Advertisement

- India

- /

- Auto Components

- /

- NSEI:JTEKTINDIA

The JTEKT India Limited (NSE:JTEKTINDIA) Analyst Just Boosted Their Forecasts By A Meaningful Amount

Celebrations may be in order for JTEKT India Limited (NSE:JTEKTINDIA) shareholders, with the covering analyst delivering a significant upgrade to their statutory estimates for the company. The consensus statutory numbers for both revenue and earnings per share (EPS) increased, with their view clearly much more bullish on the company's business prospects. JTEKT India has also found favour with investors, with the stock up a worthy 22% to ₹128 over the past week. Could this upgrade be enough to drive the stock even higher?

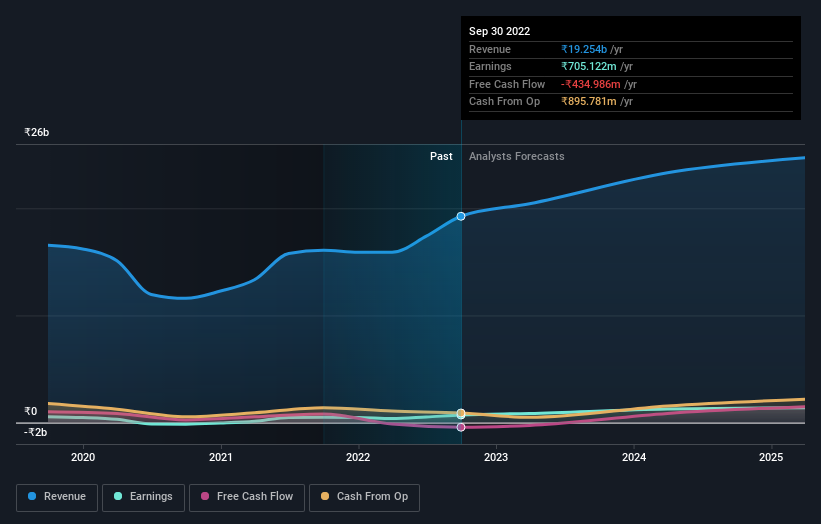

Following the upgrade, the current consensus from JTEKT India's solitary analyst is for revenues of ₹20b in 2023 which - if met - would reflect a modest 6.1% increase on its sales over the past 12 months. Statutory earnings per share are presumed to shoot up 21% to ₹3.50. Before this latest update, the analyst had been forecasting revenues of ₹18b and earnings per share (EPS) of ₹2.70 in 2023. So we can see there's been a pretty clear increase in analyst sentiment in recent times, with both revenues and earnings per share receiving a decent lift in the latest estimates.

See our latest analysis for JTEKT India

It will come as no surprise to learn that the analyst has increased their price target for JTEKT India 31% to ₹142 on the back of these upgrades.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. It's clear from the latest estimates that JTEKT India's rate of growth is expected to accelerate meaningfully, with the forecast 13% annualised revenue growth to the end of 2023 noticeably faster than its historical growth of 7.2% p.a. over the past three years. Compare this with other companies in the same industry, which are forecast to grow their revenue 12% annually. Factoring in the forecast acceleration in revenue, it's pretty clear that JTEKT India is expected to grow at about the same rate as the wider industry.

The Bottom Line

The biggest takeaway for us from these new estimates is that the analyst upgraded their earnings per share estimates, with improved earnings power expected for this year. They also upgraded their revenue forecasts, although the latest estimates suggest that JTEKT India will grow in line with the overall market. Given that the consensus looks almost universally bullish, with a substantial increase to forecasts and a higher price target, JTEKT India could be worth investigating further.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. At least one analyst has provided forecasts out to 2025, which can be seen for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:JTEKTINDIA

JTEKT India

Engages in the manufacture and sale of steering systems and auto components for the passenger car and utility vehicle manufacturers in the automobile sector in India.

Excellent balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor