Advertisement

New Forecasts: Here's What Analysts Think The Future Holds For Jamna Auto Industries Limited (NSE:JAMNAAUTO)

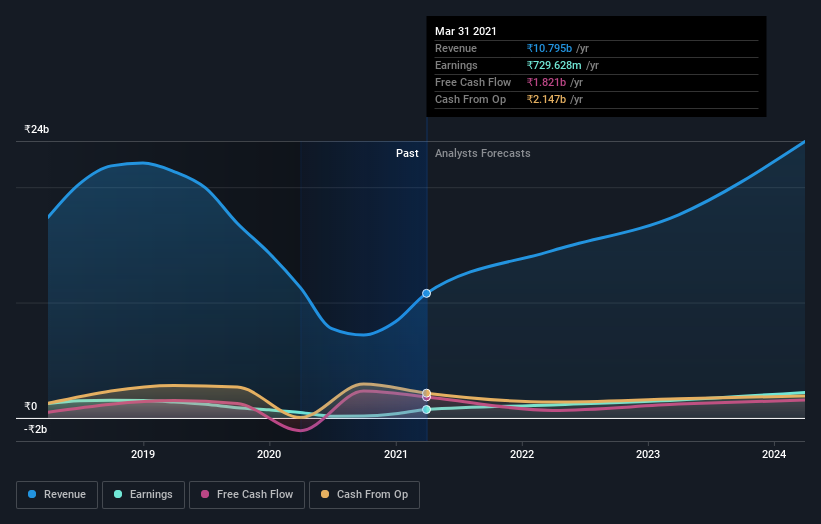

Shareholders in Jamna Auto Industries Limited (NSE:JAMNAAUTO) may be thrilled to learn that the analysts have just delivered a major upgrade to their near-term forecasts. The consensus statutory numbers for both revenue and earnings per share (EPS) increased, with their view clearly much more bullish on the company's business prospects.

Following the upgrade, the most recent consensus for Jamna Auto Industries from its four analysts is for revenues of ₹15b in 2022 which, if met, would be a huge 38% increase on its sales over the past 12 months. Statutory earnings per share are presumed to shoot up 68% to ₹3.08. Before this latest update, the analysts had been forecasting revenues of ₹13b and earnings per share (EPS) of ₹2.38 in 2022. There has definitely been an improvement in perception recently, with the analysts substantially increasing both their earnings and revenue estimates.

Check out our latest analysis for Jamna Auto Industries

It will come as no surprise to learn that the analysts have increased their price target for Jamna Auto Industries 17% to ₹88.20 on the back of these upgrades. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on Jamna Auto Industries, with the most bullish analyst valuing it at ₹108 and the most bearish at ₹55.97 per share. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Jamna Auto Industries' past performance and to peers in the same industry. One thing stands out from these estimates, which is that Jamna Auto Industries is forecast to grow faster in the future than it has in the past, with revenues expected to display 38% annualised growth until the end of 2022. If achieved, this would be a much better result than the 3.6% annual decline over the past five years. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 16% annually. So it looks like Jamna Auto Industries is expected to grow faster than its competitors, at least for a while.

The Bottom Line

The biggest takeaway for us from these new estimates is that analysts upgraded their earnings per share estimates, with improved earnings power expected for this year. Fortunately, analysts also upgraded their revenue estimates, and our data indicates sales are expected to perform better than the wider market. With a serious upgrade to expectations and a rising price target, it might be time to take another look at Jamna Auto Industries.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Jamna Auto Industries analysts - going out to 2024, and you can see them free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you’re looking to trade Jamna Auto Industries, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:JAMNAAUTO

Jamna Auto Industries

Engages in the manufacture and sale of tapered leaf, parabolic springs, and lift axles under the JAI brand in India and internationally.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|39.3% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|91.8% undervalued

DO

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.4% undervalued

AG

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|17.3% undervalued

CL

Community Contributor