Advertisement

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Gabriel India Limited (NSE:GABRIEL) does use debt in its business. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Gabriel India

How Much Debt Does Gabriel India Carry?

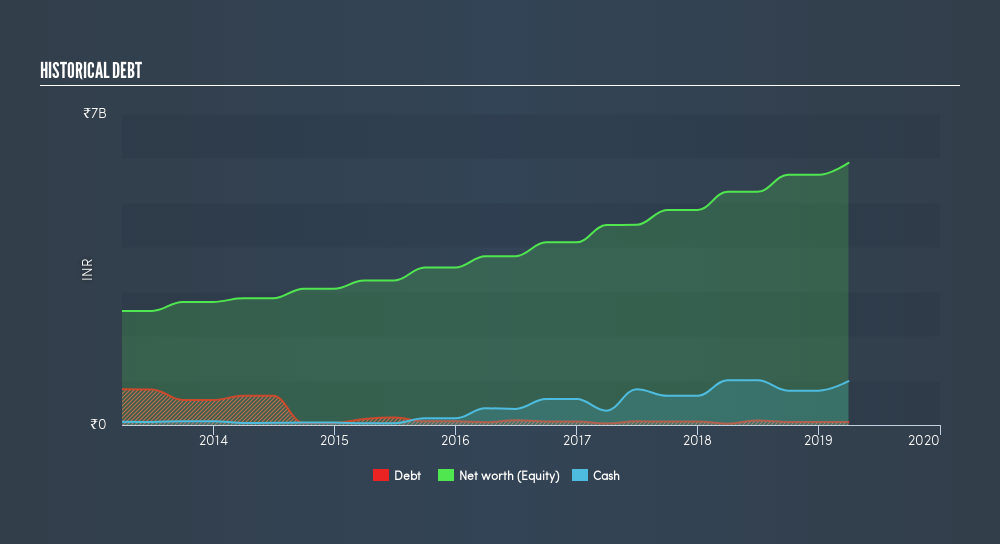

The image below, which you can click on for greater detail, shows that Gabriel India had debt of ₹69.8m at the end of March 2019, a reduction from ₹104.0m over a year. But it also has ₹986.3m in cash to offset that, meaning it has ₹916.5m net cash.

How Healthy Is Gabriel India's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Gabriel India had liabilities of ₹3.36b due within 12 months and liabilities of ₹435.3m due beyond that. Offsetting these obligations, it had cash of ₹986.3m as well as receivables valued at ₹2.85b due within 12 months. So these liquid assets roughly match the total liabilities.

This state of affairs indicates that Gabriel India's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the ₹15.2b company is struggling for cash, we still think it's worth monitoring its balance sheet. Given that Gabriel India has more cash than debt, we're pretty confident it can manage its debt safely.

The good news is that Gabriel India has increased its EBIT by 2.9% over twelve months, which should ease any concerns about debt repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Gabriel India's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Gabriel India has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. In the last three years, Gabriel India's free cash flow amounted to 48% of its EBIT, less than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that Gabriel India has net cash of ₹916m, as well as more liquid assets than liabilities. And it also grew its EBIT by 2.9% over the last year. So we are not troubled with Gabriel India's debt use. Over time, share prices tend to follow earnings per share, so if you're interested in Gabriel India, you may well want to click here to check an interactive graph of its earnings per share history.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NSEI:GABRIEL

Gabriel India

Manufactures and sells of ride control products to the automotive industry in India, the Netherlands, and internationally.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.3% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor