- Japan

- /

- Specialty Stores

- /

- TSE:3660

Undiscovered Gems with Promising Potential In January 2025

Reviewed by Simply Wall St

As global markets continue to react to political developments and economic indicators, the S&P 500 has reached new heights amid optimism for softer tariffs and advancements in artificial intelligence. While large-cap stocks have generally outperformed their smaller-cap counterparts, there remains a fertile ground of opportunity within small-cap stocks that exhibit strong fundamentals and innovative potential.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Morris State Bancshares | 10.20% | -0.28% | 6.97% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Natural Food International Holding | NA | 2.49% | 20.35% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Kenturn Nano. Tec | 45.38% | 9.73% | 28.94% | ★★★★★☆ |

| ONEJOON | 9.85% | 24.95% | 4.85% | ★★★★★☆ |

| Giant Heavy Machinery Service | 17.81% | 21.88% | 48.77% | ★★★★★☆ |

| PAN Group | 143.29% | 15.75% | 23.10% | ★★★★☆☆ |

| Petrolimex Insurance | 32.25% | 4.46% | 7.91% | ★★★★☆☆ |

| Bhakti Multi Artha | 45.21% | 32.37% | -16.43% | ★★★★☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

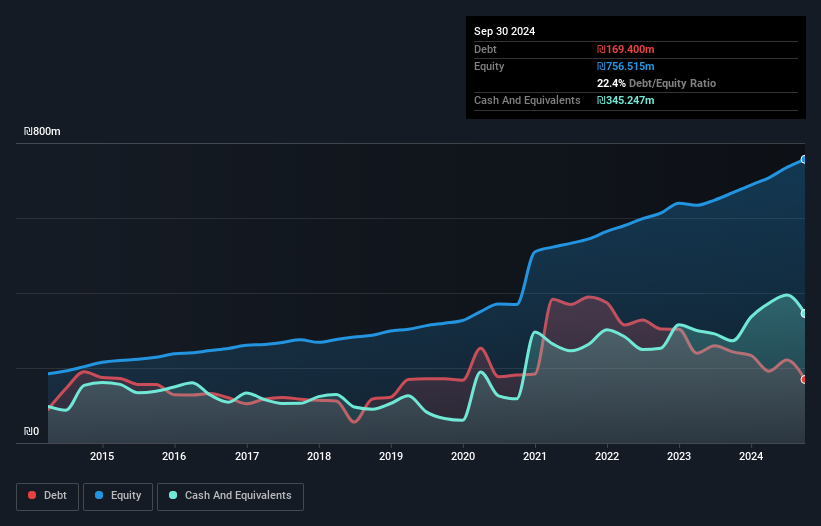

One Software Technologies (TASE:ONE)

Simply Wall St Value Rating: ★★★★★★

Overview: One Software Technologies Ltd offers software, hardware, and integration services with a market capitalization of ₪4.61 billion.

Operations: The company generates revenue primarily from three segments: Infrastructure and Computing Solutions (₪1.22 billion), Outsourcing of Business Processes and Technological Support Centers (₪317.30 million), and Technological Solutions and Services, Management Consulting, and Value-Added Services (₪2.41 billion).

In the tech landscape, One Software Technologies stands out with a robust financial profile and noteworthy growth metrics. Over the past year, earnings surged by 19%, surpassing industry averages. The company's debt to equity ratio has impressively decreased from 53% to 22% in five years, indicating prudent financial management. Trading at nearly 41% below estimated fair value suggests potential undervaluation. Moreover, its interest payments are well-covered by EBIT at a solid 18x coverage ratio. Despite recent delisting news due to inactivity on OTC Equity, its high-quality earnings and positive free cash flow remain strong points for consideration.

- Click to explore a detailed breakdown of our findings in One Software Technologies' health report.

Learn about One Software Technologies' historical performance.

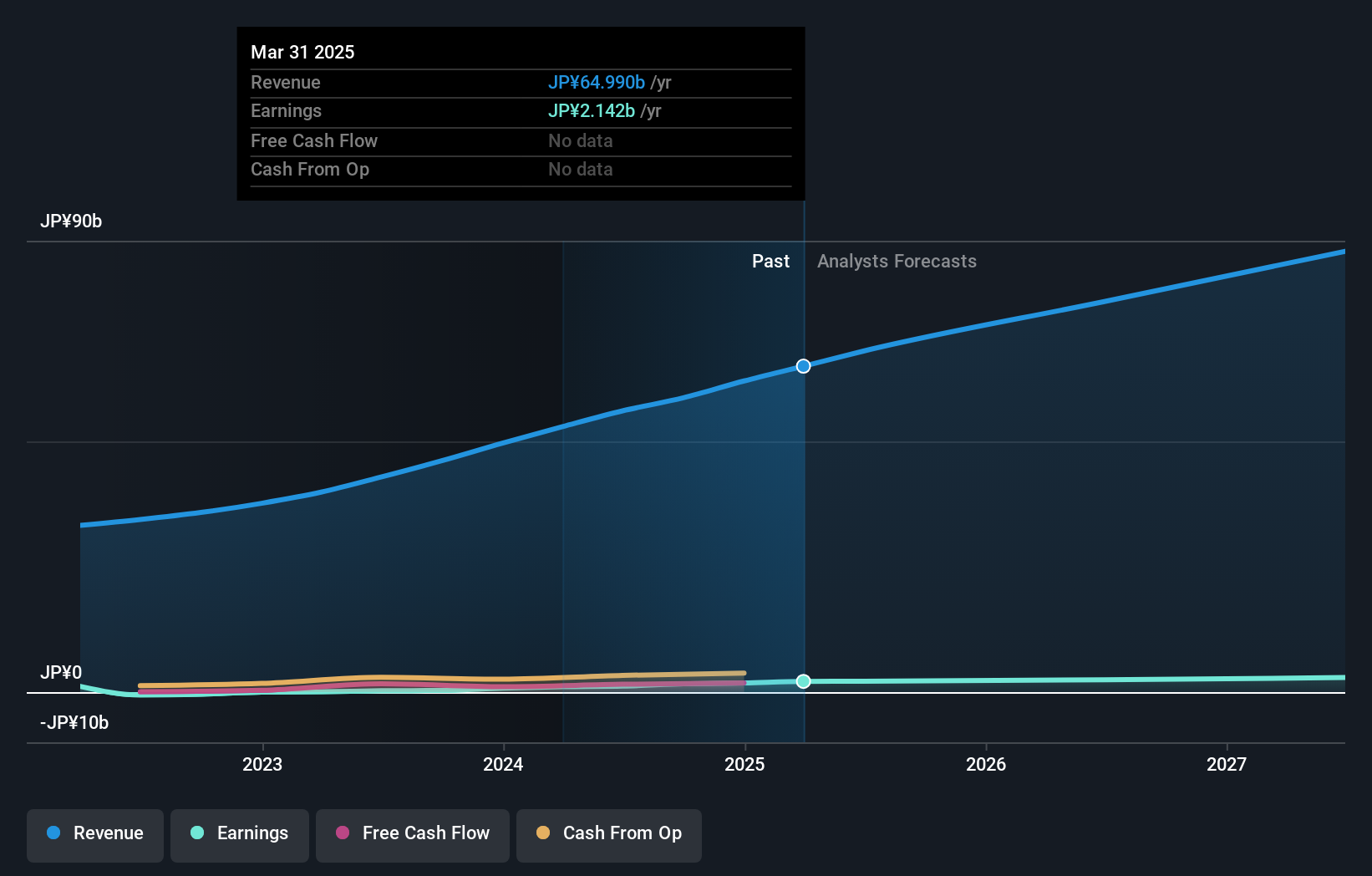

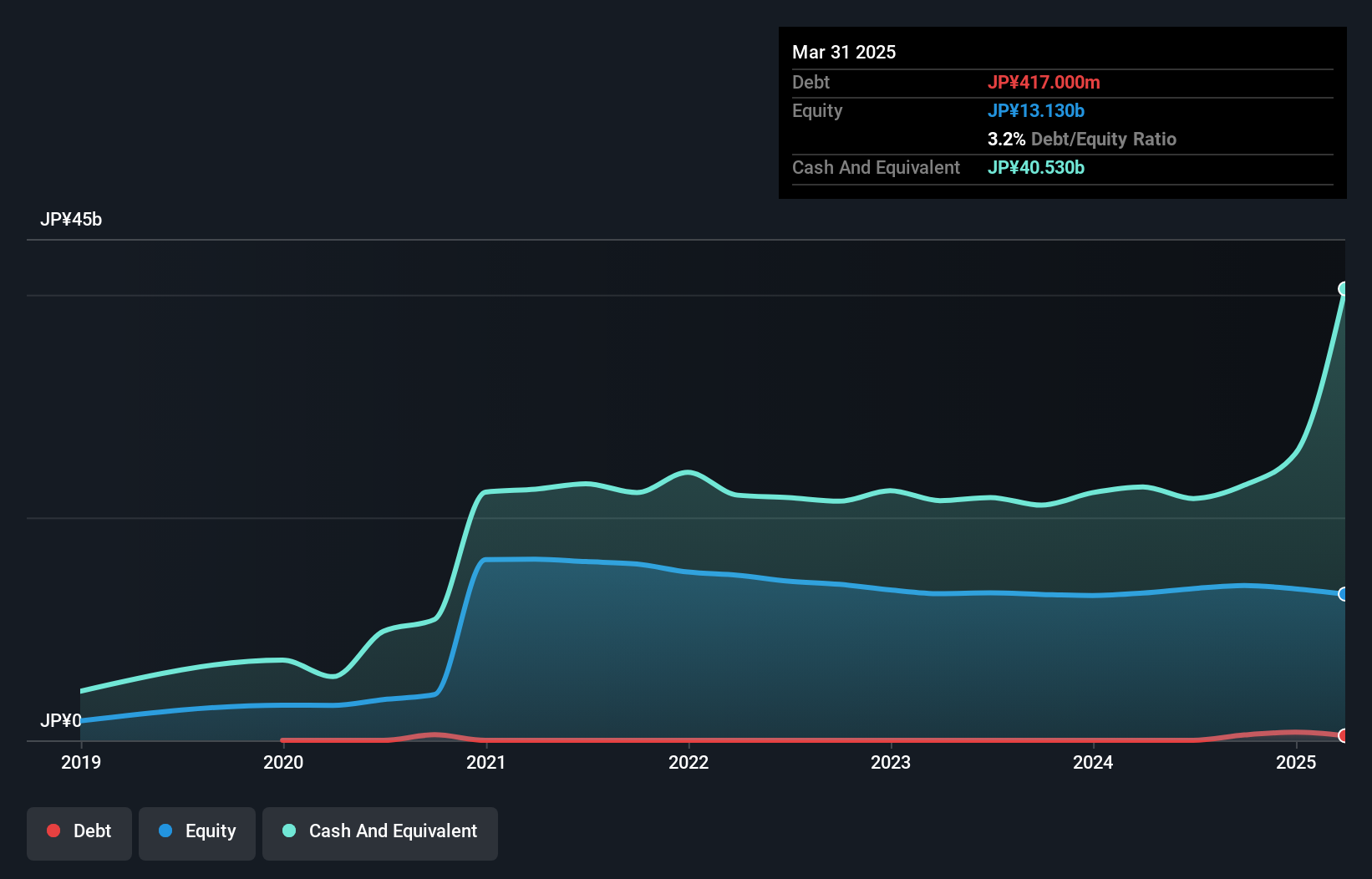

istyle (TSE:3660)

Simply Wall St Value Rating: ★★★★★★

Overview: istyle Inc. operates a beauty portal site called @cosme both in Japan and internationally, with a market cap of approximately ¥39.70 billion.

Operations: The company's primary revenue streams include Retail at ¥44.78 billion and Marketing Solution at ¥9.61 billion, with a smaller contribution from the Global segment at ¥3.84 billion. The net profit margin is a key metric to consider when evaluating its financial performance over time.

isStyle, a small player in the specialty retail sector, has shown impressive financial performance recently. The company's earnings soared by 377% last year, outpacing the industry's average growth of 5.8%. This robust growth is supported by a satisfactory net debt to equity ratio of 18.1%, indicating prudent financial management. Additionally, its interest payments are comfortably covered with EBIT at 64.8 times the interest repayments, reflecting strong operational efficiency. Despite these positives, the share price has been highly volatile over the past three months, which investors should consider when evaluating potential opportunities in this promising yet fluctuating stock environment.

- Navigate through the intricacies of istyle with our comprehensive health report here.

Review our historical performance report to gain insights into istyle's's past performance.

BASEInc (TSE:4477)

Simply Wall St Value Rating: ★★★★☆☆

Overview: BASE, Inc. is a Japanese company focused on the planning, development, and operation of web services with a market capitalization of approximately ¥39.79 billion.

Operations: BASE generates revenue primarily through its BASE Business segment, contributing ¥8.65 billion, followed by the PAY.JP Business at ¥5.25 billion, and YELL BANK Business at ¥743 million.

BASEInc., a nimble player in the tech arena, has recently turned profitable, marking a significant milestone. Its debt to equity ratio has edged up to 3.4% over five years, yet it holds more cash than total debt, indicating financial resilience. The company’s earnings are forecasted to grow at an impressive 34.83% annually, reflecting strong potential for expansion. However, BASE's share price volatility over the last three months might concern some investors. A recent board meeting discussed acquiring Estore Corporation shares from JG27 Ltd., potentially enhancing BASE's market position if successful in these strategic moves.

- Delve into the full analysis health report here for a deeper understanding of BASEInc.

Explore historical data to track BASEInc's performance over time in our Past section.

Where To Now?

- Unlock more gems! Our Undiscovered Gems With Strong Fundamentals screener has unearthed 4661 more companies for you to explore.Click here to unveil our expertly curated list of 4664 Undiscovered Gems With Strong Fundamentals.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if istyle might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:3660

istyle

Operates a beauty portal site @cosme in Japan and internationally.

Flawless balance sheet with reasonable growth potential.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion