Advertisement

- Israel

- /

- Specialty Stores

- /

- TASE:CRSM

Carasso Motors (TASE:CRSM) Net Profit Margin Climbs to 4.6%, Reinforcing Efficiency Narrative

Simply Wall St

Reviewed by Simply Wall St

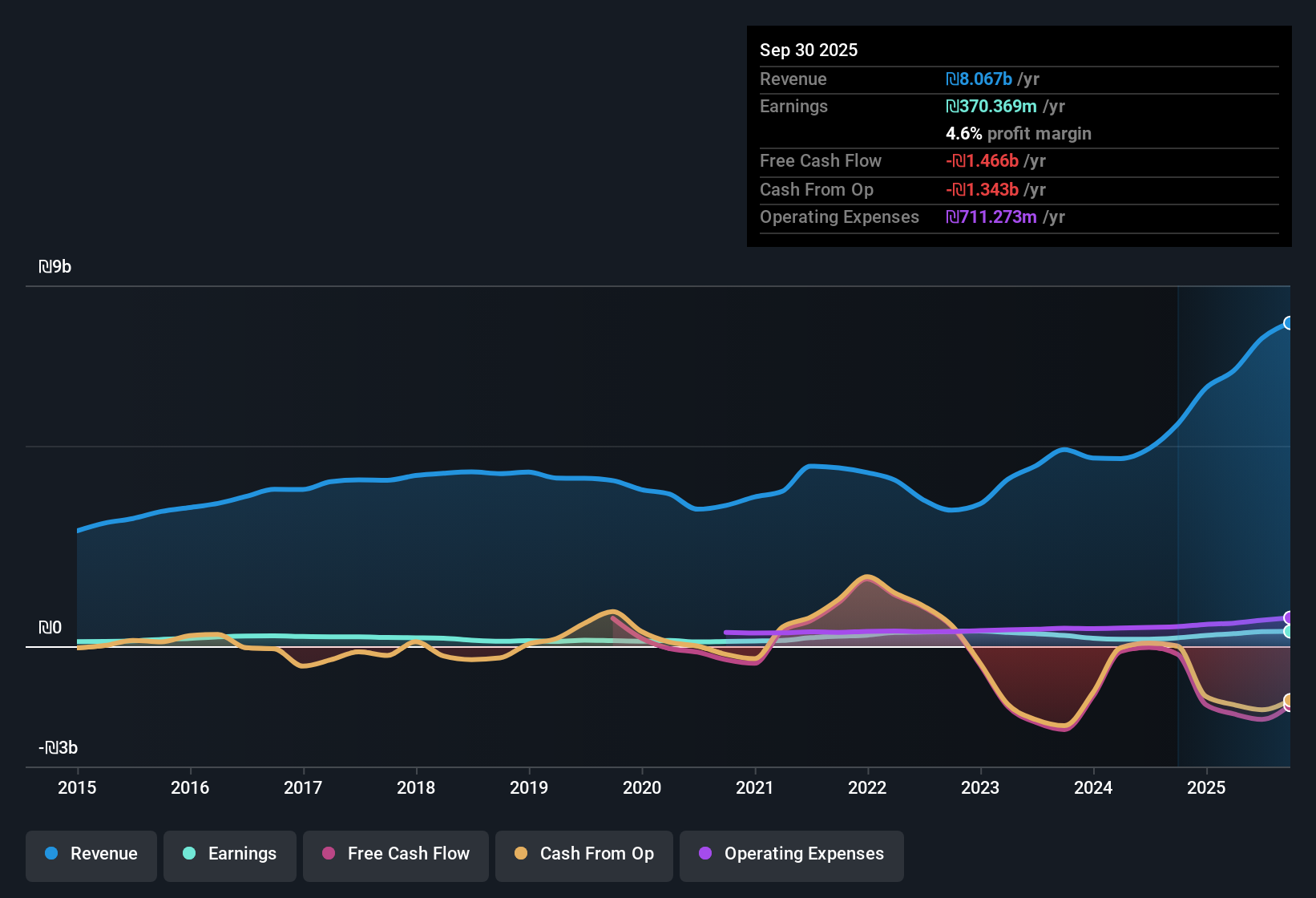

Carasso Motors (TASE:CRSM) just posted its third quarter 2025 results, landing revenue of ₪2.1 billion and basic EPS of ₪0.85. Over recent quarters, the company has seen revenue climb from ₪1.4 billion in Q2 2024 to ₪2.2 billion last quarter. Basic EPS has ranged from ₪0.68 to ₪1.26. Investors tracking the latest numbers will be watching profitability after a period where margins have steadily expanded.

See our full analysis for Carasso Motors.Let's see how this round of earnings lines up with the prevailing narratives. Some views could be confirmed, while others might need a rethink.

Curious how numbers become stories that shape markets? Explore Community Narratives

Net Profit Margin Reaches 4.6%

- Carasso Motors improved its net profit margin to 4.6% for the trailing twelve months, up from 3.8% in the comparable year-ago period.

- Analysts looking at operational efficiency point to this margin expansion as evidence of better cost management and resilience. Trailing twelve month net income climbed to ₪370.4 million alongside the margin improvement.

- This aligns with the view that diverse business lines, including services and leasing, are driving steadier, higher-quality profits.

- At the same time, the margin growth supports the argument that management is adapting well to industry change, such as electrification and recurring revenue streams.

Share Price Trades Above DCF Value

- Carasso Motors’ share price is now at ₪36.00, which is above its calculated DCF fair value of ₪22.69.

- For value-focused investors, it is notable that the price-to-earnings ratio (9.2x) remains lower than peer and industry averages. This challenges the perception that shares are overheated solely based on price.

- The wide gap between share price and DCF fair value leads to active valuation debates. Bulls may highlight sector leadership, while others question whether premium pricing is justified.

- Market watchers often cite the relatively low P/E as an anchor for bullish perspectives, even if the headline price appears stretched against intrinsic value models.

Dividend Yield Flags Sustainability Concern

- Despite a 5.27% dividend yield, Carasso Motors’ payouts are not well covered by free cash flow according to the latest reporting period.

- While the track record of profit growth appears strong, the sustainability of dividends is under scrutiny, especially as interest obligations are not fully covered by earnings.

- This highlights a tension between an attractive headline yield and the quality of underlying cash generation.

- Investors need to weigh the appeal of current distributions against the risk that payouts could be scaled back if cash flow does not improve in future quarters.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Carasso Motors's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Carasso Motors’ headline dividend yield is appealing. However, its weak free cash flow coverage and interest shortfall raise major sustainability concerns.

If you’re seeking more reliable income, check out these 1927 dividend stocks with yields > 3% for companies offering strong yields that are actually underpinned by robust, sustainable cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TASE:CRSM

Carasso Motors

Engages in the import, distribution, and sale of automobiles in Israel.

Proven track record second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

JO

JohnJ on Worldline ·

No miracle in sight

Fair Value:€7.0178.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

79 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

90 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

928 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative