Advertisement

- Israel

- /

- Real Estate

- /

- TASE:RANI

Rani Zim Shopping Centers Ltd's (TLV:RANI) Price Is Right But Growth Is Lacking After Shares Rocket 40%

Despite an already strong run, Rani Zim Shopping Centers Ltd (TLV:RANI) shares have been powering on, with a gain of 40% in the last thirty days. Looking back a bit further, it's encouraging to see the stock is up 40% in the last year.

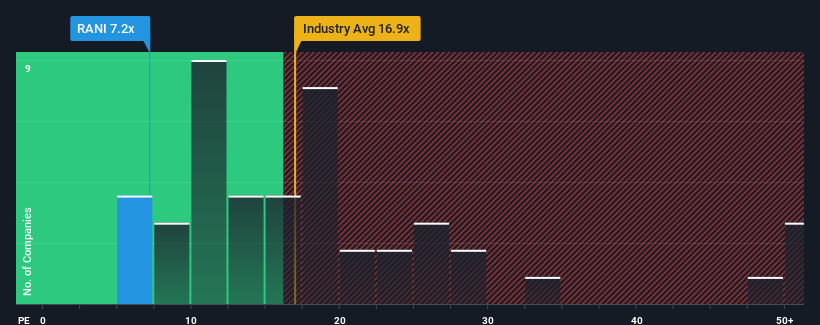

Although its price has surged higher, Rani Zim Shopping Centers' price-to-earnings (or "P/E") ratio of 7.2x might still make it look like a buy right now compared to the market in Israel, where around half of the companies have P/E ratios above 14x and even P/E's above 23x are quite common. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

Rani Zim Shopping Centers certainly has been doing a great job lately as it's been growing earnings at a really rapid pace. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If that doesn't eventuate, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

Check out our latest analysis for Rani Zim Shopping Centers

Does Growth Match The Low P/E?

In order to justify its P/E ratio, Rani Zim Shopping Centers would need to produce sluggish growth that's trailing the market.

If we review the last year of earnings growth, the company posted a terrific increase of 38%. However, the latest three year period hasn't been as great in aggregate as it didn't manage to provide any growth at all. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

This is in contrast to the rest of the market, which is expected to grow by 26% over the next year, materially higher than the company's recent medium-term annualised growth rates.

In light of this, it's understandable that Rani Zim Shopping Centers' P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on to something they believe will continue to trail the bourse.

The Final Word

Despite Rani Zim Shopping Centers' shares building up a head of steam, its P/E still lags most other companies. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Rani Zim Shopping Centers revealed its three-year earnings trends are contributing to its low P/E, given they look worse than current market expectations. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

It is also worth noting that we have found 3 warning signs for Rani Zim Shopping Centers (1 is a bit unpleasant!) that you need to take into consideration.

Of course, you might also be able to find a better stock than Rani Zim Shopping Centers. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TASE:RANI

Rani Zim Shopping Centers

Engages in the development, management, and lease or sale of commercial projects in Israel.

Proven track record with low risk.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|6.3% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.8% undervalued

GM

Community Contributor