Advertisement

- Israel

- /

- Real Estate

- /

- TASE:BCNV-M

Brack Capital Properties (TLV:BCNV-M) shareholders are up 19% this past week, but still in the red over the last year

It is a pleasure to report that the Brack Capital Properties N.V (TLV:BCNV-M) is up 32% in the last quarter. But that doesn't change the fact that the returns over the last year have been less than pleasing. After all, the share price is down 31% in the last year, significantly under-performing the market.

The recent uptick of 19% could be a positive sign of things to come, so let's take a look at historical fundamentals.

See our latest analysis for Brack Capital Properties

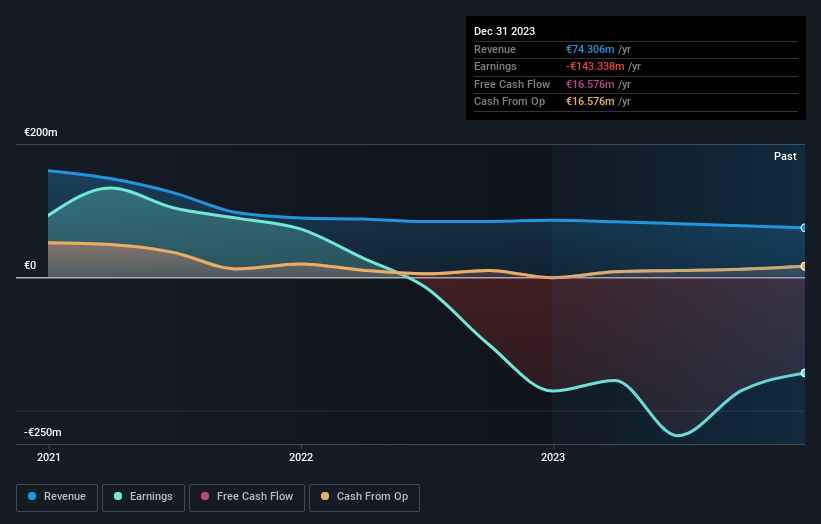

Because Brack Capital Properties made a loss in the last twelve months, we think the market is probably more focussed on revenue and revenue growth, at least for now. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

In just one year Brack Capital Properties saw its revenue fall by 13%. That looks pretty grim, at a glance. Shareholders have seen the share price drop 31% in that time. What would you expect when revenue is falling, and it doesn't make a profit? We think most holders must believe revenue growth will improve, or else costs will decline.

The graphic below depicts how earnings and revenue have changed over time (unveil the exact values by clicking on the image).

Take a more thorough look at Brack Capital Properties' financial health with this free report on its balance sheet.

A Different Perspective

While the broader market gained around 9.1% in the last year, Brack Capital Properties shareholders lost 31%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 5% over the last half decade. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Even so, be aware that Brack Capital Properties is showing 3 warning signs in our investment analysis , you should know about...

If you would prefer to check out another company -- one with potentially superior financials -- then do not miss this free list of companies that have proven they can grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Israeli exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Brack Capital Properties might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TASE:BCNV-M

Brack Capital Properties

A real estate company, owns and develops residential and commercial properties in Germany.

Low and slightly overvalued.

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|69.8% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|15.0% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|36.1% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$202.60|21.1% undervalued

AN

Based on Analyst Price Targets