Advertisement

- Israel

- /

- Household Products

- /

- TASE:SANO1

Sano Bruno's (TASE:SANO1) Net Margin Falls to 11.2%, Challenging Defensive Profitability Narrative

Simply Wall St

Reviewed by Simply Wall St

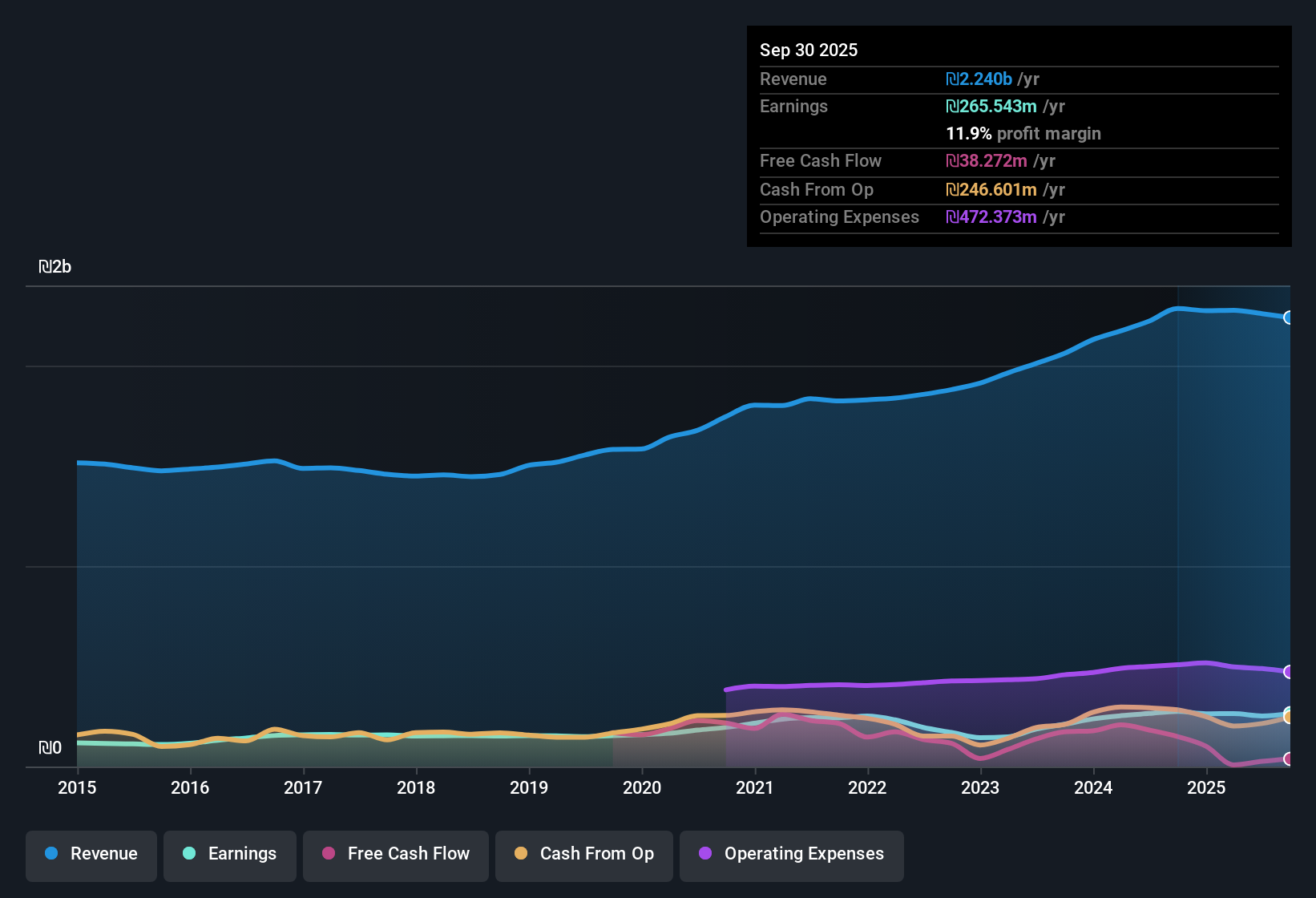

Sano Bruno's Enterprises (TASE:SANO1) just reported Q3 2025 financials with revenue of ₪536.5 million and basic EPS of ₪5.01. Over the last year, the company has seen revenue fluctuate between ₪531.6 million and ₪605.2 million per quarter, while EPS has ranged from ₪5.01 to ₪6.24. Margins came under a bit of pressure compared to last year, raising questions for investors on how profitability trends are shaping up.

See our full analysis for Sano Bruno's Enterprises.Now that the headline numbers are in, it is time to see how these results match up to the main market narratives. Some storylines might get challenged, while others could be reinforced.

Curious how numbers become stories that shape markets? Explore Community Narratives

Net Margins Dip to 11.2%

- Trailing twelve month net profit margin slid to 11.2%, down from 11.9% last year, signaling modest pressure on profitability even as revenues remained steady above ₪2.2 billion.

- Investors monitoring sector stability will note that despite this margin squeeze and negative yearly earnings growth, the company maintained high quality earnings. Bears caution that if this profitability dip continues, it could erode the income consistency that defensive names depend on.

- Consensus narrative points out that while the company’s margin and recent earnings growth faltered, its stable product demand and lack of new risks provide a base for resilience going forward.

- Trailing earnings growth over the last five years averaged +4.2% annually, but the most recent year contracted.

Peer Comparison: P/E Sits Below Sector

- Sano Bruno's Enterprises trades at a trailing P/E of 17.9x, lower than the household products industry average of 18.2x and well under the peer average of 24.7x.

- In reviewing comparative valuation, general market opinion suggests this relative discount supports a case for attractively priced shares. However, with the company’s current share price of ₪401.5 sitting markedly above the DCF fair value of ₪133.18, cautious investors may see the valuation gap as justification for restraint.

- The material gap between market and DCF values shows why price alone does not guarantee a bargain, especially with fundamentals facing pressure.

- Even as the lower P/E suggests value, the negative earnings trend and margin slip provide important context.

Revenue Holds Steady Despite Volatility

- Over the last four quarters, total revenue has remained consistently above ₪2.2 billion, with quarterly figures fluctuating but never dropping below ₪531.6 million. This underscores the company's core demand stability.

- The prevailing market view highlights that Sano Bruno's Enterprises’ diversified product portfolio continues to foster reliable sales despite broader headwinds. Opinions diverge on whether continued cost pressures could soon challenge this revenue resilience.

- Industry context: The non-food FMCG sector typically benefits from inelastic demand, but ongoing input cost pressure is being closely monitored by investors.

- Consensus narrative notes the company’s defensive positioning may appeal during volatile periods, even as growth remains modest.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Sano Bruno's Enterprises's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Despite stable revenues, Sano Bruno's Enterprises faces narrowing margins and a valuation premium to fair value. This situation is increasing concerns for cautious investors.

If you want to avoid overpaying for pressured fundamentals, check out these 920 undervalued stocks based on cash flows and discover companies trading at more attractive prices with robust value metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TASE:SANO1

Sano Bruno's Enterprises

Engages in the development, production, marketing, distribution, and sale of non-food household and commercial consumer products in Israel and internationally.

Flawless balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative