Advertisement

- Israel

- /

- Food and Staples Retail

- /

- TASE:HMAM

Returns On Capital At Hamama Meir Trading (1996) (TLV:HMAM) Paint A Concerning Picture

When we're researching a company, it's sometimes hard to find the warning signs, but there are some financial metrics that can help spot trouble early. Typically, we'll see the trend of both return on capital employed (ROCE) declining and this usually coincides with a decreasing amount of capital employed. This indicates to us that the business is not only shrinking the size of its net assets, but its returns are falling as well. So after glancing at the trends within Hamama Meir Trading (1996) (TLV:HMAM), we weren't too hopeful.

Understanding Return On Capital Employed (ROCE)

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for Hamama Meir Trading (1996), this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.017 = ₪1.5m ÷ (₪198m - ₪114m) (Based on the trailing twelve months to June 2020).

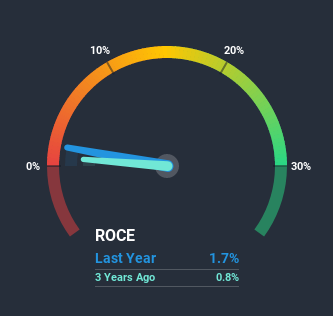

Therefore, Hamama Meir Trading (1996) has an ROCE of 1.7%. In absolute terms, that's a low return and it also under-performs the Consumer Retailing industry average of 11%.

See our latest analysis for Hamama Meir Trading (1996)

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating Hamama Meir Trading (1996)'s past further, check out this free graph of past earnings, revenue and cash flow.

What Does the ROCE Trend For Hamama Meir Trading (1996) Tell Us?

We are a bit anxious about the trends of ROCE at Hamama Meir Trading (1996). Unfortunately, returns have declined substantially over the last five years to the 1.7% we see today. What's equally concerning is that the amount of capital deployed in the business has shrunk by 49% over that same period. The fact that both are shrinking is an indication that the business is going through some tough times. If these underlying trends continue, we wouldn't be too optimistic going forward.

On a side note, Hamama Meir Trading (1996)'s current liabilities are still rather high at 58% of total assets. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. While it's not necessarily a bad thing, it can be beneficial if this ratio is lower.

The Bottom Line On Hamama Meir Trading (1996)'s ROCE

In summary, it's unfortunate that Hamama Meir Trading (1996) is shrinking its capital base and also generating lower returns. Investors must expect better things on the horizon though because the stock has risen 7.1% in the last five years. Regardless, we don't like the trends as they are and if they persist, we think you might find better investments elsewhere.

On a separate note, we've found 2 warning signs for Hamama Meir Trading (1996) you'll probably want to know about.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

If you’re looking to trade Hamama Meir Trading (1996), open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Hamama Meir Trading (1996) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TASE:HMAM

Hamama Meir Trading (1996)

Engages in the import and distribution of raw materials for the food industry in Israel.

Excellent balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|45.0% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|47.8% undervalued

TO

Community Contributor