- Israel

- /

- Construction

- /

- TASE:BRND

Risks Still Elevated At These Prices As Brand Group (M.G) Ltd (TLV:BRND) Shares Dive 27%

Brand Group (M.G) Ltd (TLV:BRND) shares have had a horrible month, losing 27% after a relatively good period beforehand. The recent drop has obliterated the annual return, with the share price now down 5.5% over that longer period.

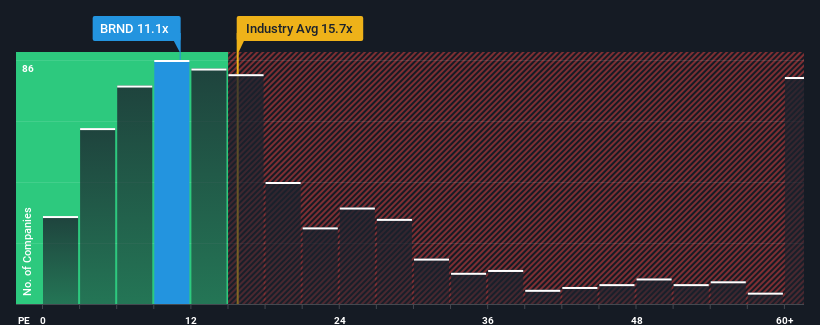

Even after such a large drop in price, you could still be forgiven for feeling indifferent about Brand Group (M.G)'s P/E ratio of 11.1x, since the median price-to-earnings (or "P/E") ratio in Israel is also close to 12x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

As an illustration, earnings have deteriorated at Brand Group (M.G) over the last year, which is not ideal at all. One possibility is that the P/E is moderate because investors think the company might still do enough to be in line with the broader market in the near future. If not, then existing shareholders may be a little nervous about the viability of the share price.

Check out our latest analysis for Brand Group (M.G)

Does Growth Match The P/E?

In order to justify its P/E ratio, Brand Group (M.G) would need to produce growth that's similar to the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 41%. The last three years don't look nice either as the company has shrunk EPS by 38% in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

In contrast to the company, the rest of the market is expected to grow by 13% over the next year, which really puts the company's recent medium-term earnings decline into perspective.

With this information, we find it concerning that Brand Group (M.G) is trading at a fairly similar P/E to the market. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. Only the boldest would assume these prices are sustainable as a continuation of recent earnings trends is likely to weigh on the share price eventually.

The Final Word

Following Brand Group (M.G)'s share price tumble, its P/E is now hanging on to the median market P/E. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Brand Group (M.G) currently trades on a higher than expected P/E since its recent earnings have been in decline over the medium-term. When we see earnings heading backwards and underperforming the market forecasts, we suspect the share price is at risk of declining, sending the moderate P/E lower. If recent medium-term earnings trends continue, it will place shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

There are also other vital risk factors to consider and we've discovered 4 warning signs for Brand Group (M.G) (2 shouldn't be ignored!) that you should be aware of before investing here.

If these risks are making you reconsider your opinion on Brand Group (M.G), explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Brand Group (M.G) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TASE:BRND

Brand Group (M.G)

Engages in metal construction and infrastructure, energy facilities, petrochemical facilities, and other industrial facilities in Israel.

Low with questionable track record.

Market Insights

Community Narratives