Advertisement

- Israel

- /

- Construction

- /

- TASE:BRAN

We're Not So Sure You Should Rely on Baran Group's (TLV:BRAN) Statutory Earnings

Broadly speaking, profitable businesses are less risky than unprofitable ones. That said, the current statutory profit is not always a good guide to a company's underlying profitability. This article will consider whether Baran Group's (TLV:BRAN) statutory profits are a good guide to its underlying earnings.

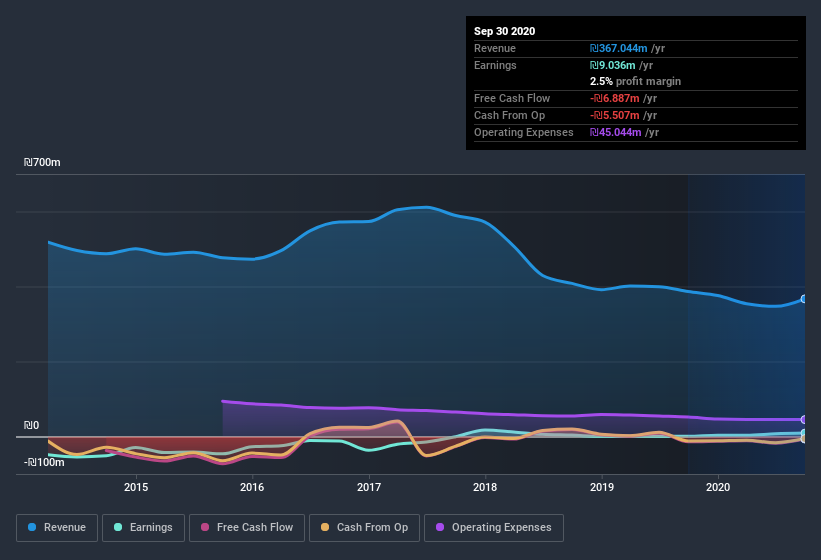

We like the fact that Baran Group made a profit of ₪9.04m on its revenue of ₪367.0m, in the last year. The chart below shows that while revenue has fallen over the last three years, the company has moved from unprofitable to profitable.

Check out our latest analysis for Baran Group

Importantly, statutory profits are not always the best tool for understanding a company's true earnings power, so it's well worth examining profits in a little more detail. In this article we will consider how Baran Group's decision to issue new shares in the company has impacted returns to shareholders. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Baran Group.

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. In fact, Baran Group increased the number of shares on issue by 98% over the last twelve months by issuing new shares. As a result, its net income is now split between a greater number of shares. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. Check out Baran Group's historical EPS growth by clicking on this link.

A Look At The Impact Of Baran Group's Dilution on Its Earnings Per Share (EPS).

Baran Group was losing money three years ago. The good news is that profit was up 2,084% in the last twelve months. But EPS was less impressive, up only 1,108% in that time. So you can see that the dilution has had a fairly significant impact on shareholders.

Changes in the share price do tend to reflect changes in earnings per share, in the long run. So it will certainly be a positive for shareholders if Baran Group can grow EPS persistently. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

Our Take On Baran Group's Profit Performance

Baran Group shareholders should keep in mind how many new shares it is issuing, because, dilution clearly has the power to severely impact shareholder returns. For this reason, we think that Baran Group's statutory profits may be a bad guide to its underlying earnings power, and might give investors an overly positive impression of the company. The silver lining is that its EPS growth over the last year has been really wonderful, even if it's not a perfect measure. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. So while earnings quality is important, it's equally important to consider the risks facing Baran Group at this point in time. For instance, we've identified 3 warning signs for Baran Group (2 shouldn't be ignored) you should be familiar with.

This note has only looked at a single factor that sheds light on the nature of Baran Group's profit. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

When trading Baran Group or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Baran Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TASE:BRAN

Baran Group

An engineering company, provides engineering solutions for projects in Israel and internationally.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor