Some Investors May Be Worried About Birman Wood & Hardware's (TLV:BIRM) Returns On Capital

If you're looking at a mature business that's past the growth phase, what are some of the underlying trends that pop up? More often than not, we'll see a declining return on capital employed (ROCE) and a declining amount of capital employed. Ultimately this means that the company is earning less per dollar invested and on top of that, it's shrinking its base of capital employed. So after glancing at the trends within Birman Wood & Hardware (TLV:BIRM), we weren't too hopeful.

Return On Capital Employed (ROCE): What Is It?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for Birman Wood & Hardware, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

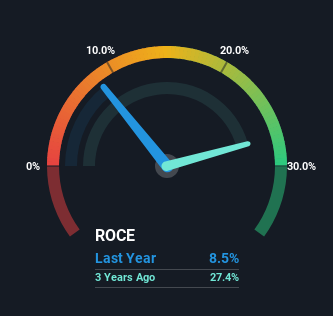

0.085 = ₪13m ÷ (₪389m - ₪241m) (Based on the trailing twelve months to June 2024).

So, Birman Wood & Hardware has an ROCE of 8.5%. Even though it's in line with the industry average of 8.8%, it's still a low return by itself.

Check out our latest analysis for Birman Wood & Hardware

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you want to delve into the historical earnings , check out these free graphs detailing revenue and cash flow performance of Birman Wood & Hardware.

So How Is Birman Wood & Hardware's ROCE Trending?

In terms of Birman Wood & Hardware's historical ROCE movements, the trend doesn't inspire confidence. To be more specific, the ROCE was 12% five years ago, but since then it has dropped noticeably. Meanwhile, capital employed in the business has stayed roughly the flat over the period. Companies that exhibit these attributes tend to not be shrinking, but they can be mature and facing pressure on their margins from competition. If these trends continue, we wouldn't expect Birman Wood & Hardware to turn into a multi-bagger.

While on the subject, we noticed that the ratio of current liabilities to total assets has risen to 62%, which has impacted the ROCE. If current liabilities hadn't increased as much as they did, the ROCE could actually be even lower. What this means is that in reality, a rather large portion of the business is being funded by the likes of the company's suppliers or short-term creditors, which can bring some risks of its own.

What We Can Learn From Birman Wood & Hardware's ROCE

All in all, the lower returns from the same amount of capital employed aren't exactly signs of a compounding machine. But investors must be expecting an improvement of sorts because over the last five yearsthe stock has delivered a respectable 72% return. In any case, the current underlying trends don't bode well for long term performance so unless they reverse, we'd start looking elsewhere.

Birman Wood & Hardware does have some risks, we noticed 5 warning signs (and 2 which don't sit too well with us) we think you should know about.

While Birman Wood & Hardware may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Valuation is complex, but we're here to simplify it.

Discover if Birman Wood & Hardware might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TASE:BIRM

Birman Wood & Hardware

Imports, produces, and markets wood panels, hardware products, kitchen electrical appliances, and laminate flooring parquets.

Moderate and good value.

Market Insights

Community Narratives