Kerry Group's (ISE:KRZ) Upcoming Dividend Will Be Larger Than Last Year's

Kerry Group plc (ISE:KRZ) will increase its dividend from last year's comparable payment on the 11th of November to €0.314. Although the dividend is now higher, the yield is only 1.1%, which is below the industry average.

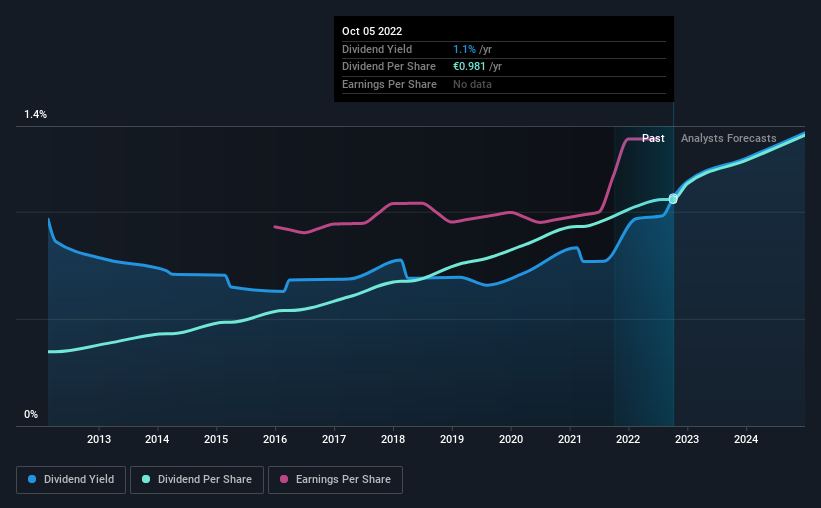

Check out our latest analysis for Kerry Group

Kerry Group's Payment Has Solid Earnings Coverage

While yield is important, another factor to consider about a company's dividend is whether the current payout levels are feasible. Before making this announcement, Kerry Group was easily earning enough to cover the dividend. This means that most of its earnings are being retained to grow the business.

Over the next year, EPS is forecast to expand by 26.5%. If the dividend continues on this path, the payout ratio could be 20% by next year, which we think can be pretty sustainable going forward.

Kerry Group Has A Solid Track Record

The company has an extended history of paying stable dividends. The dividend has gone from an annual total of €0.322 in 2012 to the most recent total annual payment of €0.981. This means that it has been growing its distributions at 12% per annum over that time. So, dividends have been growing pretty quickly, and even more impressively, they haven't experienced any notable falls during this period.

We Could See Kerry Group's Dividend Growing

Investors could be attracted to the stock based on the quality of its payment history. Kerry Group has seen EPS rising for the last five years, at 7.3% per annum. Kerry Group definitely has the potential to grow its dividend in the future with earnings on an uptrend and a low payout ratio.

We Really Like Kerry Group's Dividend

Overall, a dividend increase is always good, and we think that Kerry Group is a strong income stock thanks to its track record and growing earnings. Earnings are easily covering distributions, and the company is generating plenty of cash. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Earnings growth generally bodes well for the future value of company dividend payments. See if the 14 Kerry Group analysts we track are forecasting continued growth with our free report on analyst estimates for the company. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Kerry Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ISE:KRZ

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Community Narratives