Advertisement

- Hungary

- /

- Real Estate

- /

- BUSE:BIF

Is Budapesti Ingatlan Hasznosítási és Fejlesztési Nyrt (BUSE:BIF) A Risky Investment?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Budapesti Ingatlan Hasznosítási és Fejlesztési Nyrt. (BUSE:BIF) makes use of debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Budapesti Ingatlan Hasznosítási és Fejlesztési Nyrt

What Is Budapesti Ingatlan Hasznosítási és Fejlesztési Nyrt's Debt?

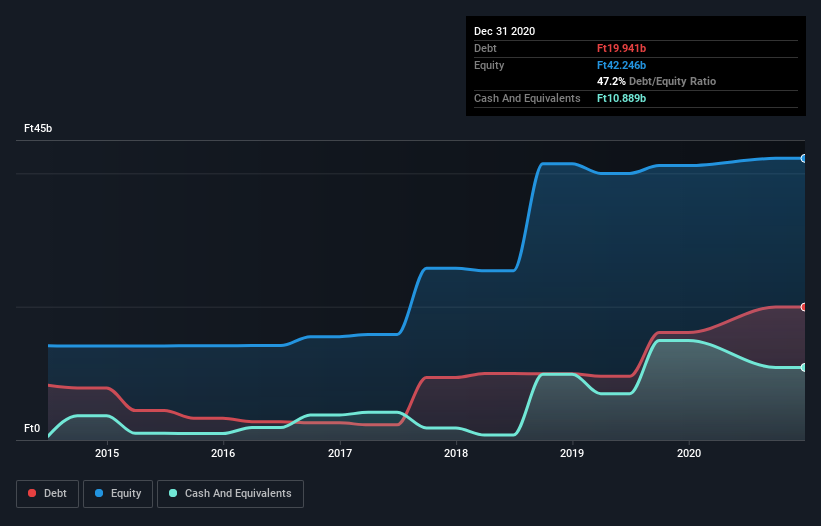

You can click the graphic below for the historical numbers, but it shows that as of December 2020 Budapesti Ingatlan Hasznosítási és Fejlesztési Nyrt had Ft19.9b of debt, an increase on Ft16.1b, over one year. On the flip side, it has Ft10.9b in cash leading to net debt of about Ft9.05b.

How Healthy Is Budapesti Ingatlan Hasznosítási és Fejlesztési Nyrt's Balance Sheet?

According to the last reported balance sheet, Budapesti Ingatlan Hasznosítási és Fejlesztési Nyrt had liabilities of Ft4.40b due within 12 months, and liabilities of Ft19.1b due beyond 12 months. Offsetting these obligations, it had cash of Ft10.9b as well as receivables valued at Ft911.1m due within 12 months. So its liabilities total Ft11.7b more than the combination of its cash and short-term receivables.

Of course, Budapesti Ingatlan Hasznosítási és Fejlesztési Nyrt has a market capitalization of Ft62.9b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Budapesti Ingatlan Hasznosítási és Fejlesztési Nyrt's net debt to EBITDA ratio of about 1.8 suggests only moderate use of debt. And its commanding EBIT of 22.0 times its interest expense, implies the debt load is as light as a peacock feather. Pleasingly, Budapesti Ingatlan Hasznosítási és Fejlesztési Nyrt is growing its EBIT faster than former Australian PM Bob Hawke downs a yard glass, boasting a 105% gain in the last twelve months. When analysing debt levels, the balance sheet is the obvious place to start. But it is Budapesti Ingatlan Hasznosítási és Fejlesztési Nyrt's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. During the last three years, Budapesti Ingatlan Hasznosítási és Fejlesztési Nyrt burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

Based on what we've seen Budapesti Ingatlan Hasznosítási és Fejlesztési Nyrt is not finding it easy, given its conversion of EBIT to free cash flow, but the other factors we considered give us cause to be optimistic. There's no doubt that its ability to to cover its interest expense with its EBIT is pretty flash. When we consider all the elements mentioned above, it seems to us that Budapesti Ingatlan Hasznosítási és Fejlesztési Nyrt is managing its debt quite well. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example Budapesti Ingatlan Hasznosítási és Fejlesztési Nyrt has 3 warning signs (and 2 which make us uncomfortable) we think you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

When trading Budapesti Ingatlan Hasznosítási és Fejlesztési Nyrt or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Budapesti Ingatlan Hasznosítási és Fejlesztési Nyrt might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About BUSE:BIF

Budapesti Ingatlan Hasznosítási és Fejlesztési Nyrt

Budapesti Ingatlan Hasznosítási és Fejlesztési Nyrt.

Excellent balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|8.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.6% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor