Advertisement

- Croatia

- /

- Marine and Shipping

- /

- ZGSE:JDPL

Jadroplov d.d. (ZGSE:JDPL) Soars 37% But It's A Story Of Risk Vs Reward

Jadroplov d.d. (ZGSE:JDPL) shares have had a really impressive month, gaining 37% after a shaky period beforehand. Notwithstanding the latest gain, the annual share price return of 7.1% isn't as impressive.

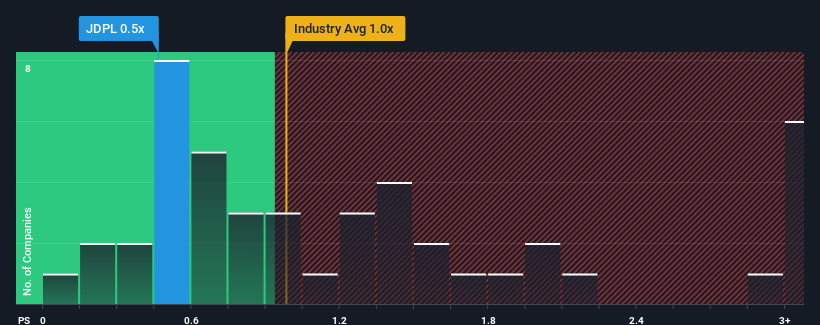

Although its price has surged higher, when close to half the companies operating in Croatia's Shipping industry have price-to-sales ratios (or "P/S") above 1x, you may still consider Jadroplov d.d as an enticing stock to check out with its 0.5x P/S ratio. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Jadroplov d.d

What Does Jadroplov d.d's Recent Performance Look Like?

For instance, Jadroplov d.d's receding revenue in recent times would have to be some food for thought. Perhaps the market believes the recent revenue performance isn't good enough to keep up the industry, causing the P/S ratio to suffer. However, if this doesn't eventuate then existing shareholders may be feeling optimistic about the future direction of the share price.

Although there are no analyst estimates available for Jadroplov d.d, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Do Revenue Forecasts Match The Low P/S Ratio?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Jadroplov d.d's to be considered reasonable.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 17%. The last three years don't look nice either as the company has shrunk revenue by 14% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

This is in contrast to the rest of the industry, which is expected to decline by 13% over the next year, even worse than the company's recent medium-term annualised revenue decline.

With this information, it's perhaps strange but not a major surprise that Jadroplov d.d is trading at a lower P/S in comparison. Even if the company's recent growth rates continue outperforming the industry, shrinking revenues are unlikely to lead to a stable P/S long-term. Even just maintaining these prices will be difficult to achieve as recent revenue trends are already weighing down the shares excessively.

What We Can Learn From Jadroplov d.d's P/S?

Jadroplov d.d's stock price has surged recently, but its but its P/S still remains modest. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

A look into numbers has shown it's somewhat unexpected that Jadroplov d.d has a lower P/S than the industry average, given its recent three-year revenue performance which was better than anticipated for an industry facing challenges. There could be some major unobserved threats to revenue preventing the P/S ratio from matching this comparatively more attractive revenue performance. Perhaps there is some hesitation about the company's ability to stay its recent course and resist the broader industry turmoil. While recent medium-term revenue trends suggest that the risk of a price decline is low, investors appear to perceive a possibility of revenue volatility in the future.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Jadroplov d.d (of which 1 is concerning!) you should know about.

If you're unsure about the strength of Jadroplov d.d's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ZGSE:JDPL

Jadroplov d.d

Engages in the international maritime transportation of goods with its own tramp ships.

Slight risk and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor