- Hong Kong

- /

- Gas Utilities

- /

- SEHK:2688

We Think ENN Energy Holdings (HKG:2688) Can Stay On Top Of Its Debt

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, ENN Energy Holdings Limited (HKG:2688) does carry debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for ENN Energy Holdings

How Much Debt Does ENN Energy Holdings Carry?

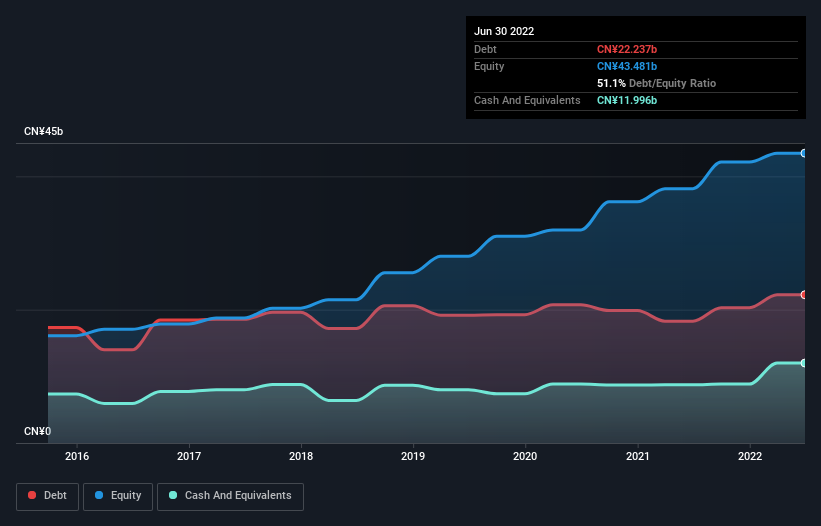

As you can see below, at the end of June 2022, ENN Energy Holdings had CN¥22.2b of debt, up from CN¥18.3b a year ago. Click the image for more detail. However, it does have CN¥12.0b in cash offsetting this, leading to net debt of about CN¥10.2b.

How Healthy Is ENN Energy Holdings' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that ENN Energy Holdings had liabilities of CN¥39.1b due within 12 months and liabilities of CN¥20.9b due beyond that. Offsetting these obligations, it had cash of CN¥12.0b as well as receivables valued at CN¥13.8b due within 12 months. So it has liabilities totalling CN¥34.2b more than its cash and near-term receivables, combined.

ENN Energy Holdings has a very large market capitalization of CN¥114.1b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

ENN Energy Holdings's net debt is only 0.94 times its EBITDA. And its EBIT covers its interest expense a whopping 46.4 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. But the other side of the story is that ENN Energy Holdings saw its EBIT decline by 4.9% over the last year. That sort of decline, if sustained, will obviously make debt harder to handle. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine ENN Energy Holdings's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. During the last three years, ENN Energy Holdings produced sturdy free cash flow equating to 52% of its EBIT, about what we'd expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

On our analysis ENN Energy Holdings's interest cover should signal that it won't have too much trouble with its debt. But the other factors we noted above weren't so encouraging. For instance it seems like it has to struggle a bit to grow its EBIT. It's also worth noting that ENN Energy Holdings is in the Gas Utilities industry, which is often considered to be quite defensive. When we consider all the elements mentioned above, it seems to us that ENN Energy Holdings is managing its debt quite well. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. We'd be motivated to research the stock further if we found out that ENN Energy Holdings insiders have bought shares recently. If you would too, then you're in luck, since today we're sharing our list of reported insider transactions for free.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if ENN Energy Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2688

ENN Energy Holdings

An investment holding company, engages in the investment, construction, operation, and management of gas pipeline infrastructure in the People’s Republic of China.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Community Narratives