Advertisement

- Hong Kong

- /

- Infrastructure

- /

- SEHK:871

Revenues Working Against China Dredging Environment Protection Holdings Limited's (HKG:871) Share Price Following 29% Dive

Unfortunately for some shareholders, the China Dredging Environment Protection Holdings Limited (HKG:871) share price has dived 29% in the last thirty days, prolonging recent pain. Longer-term, the stock has been solid despite a difficult 30 days, gaining 21% in the last year.

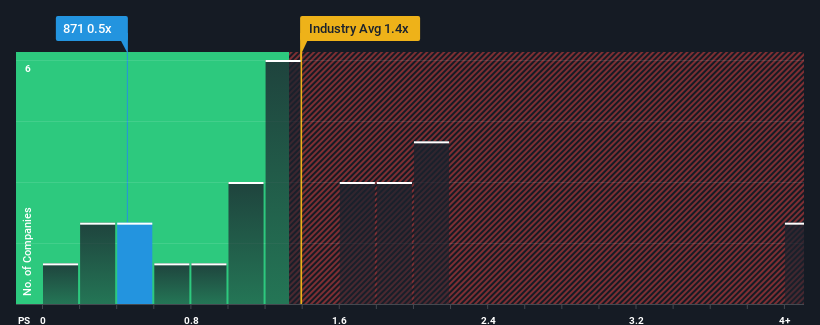

Following the heavy fall in price, when close to half the companies operating in Hong Kong's Infrastructure industry have price-to-sales ratios (or "P/S") above 1.4x, you may consider China Dredging Environment Protection Holdings as an enticing stock to check out with its 0.5x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

View our latest analysis for China Dredging Environment Protection Holdings

What Does China Dredging Environment Protection Holdings' Recent Performance Look Like?

For instance, China Dredging Environment Protection Holdings' receding revenue in recent times would have to be some food for thought. It might be that many expect the disappointing revenue performance to continue or accelerate, which has repressed the P/S. Those who are bullish on China Dredging Environment Protection Holdings will be hoping that this isn't the case so that they can pick up the stock at a lower valuation.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on China Dredging Environment Protection Holdings' earnings, revenue and cash flow.Is There Any Revenue Growth Forecasted For China Dredging Environment Protection Holdings?

In order to justify its P/S ratio, China Dredging Environment Protection Holdings would need to produce sluggish growth that's trailing the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 13%. This means it has also seen a slide in revenue over the longer-term as revenue is down 16% in total over the last three years. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

In contrast to the company, the rest of the industry is expected to grow by 1.7% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

In light of this, it's understandable that China Dredging Environment Protection Holdings' P/S would sit below the majority of other companies. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. Even just maintaining these prices could be difficult to achieve as recent revenue trends are already weighing down the shares.

What Does China Dredging Environment Protection Holdings' P/S Mean For Investors?

China Dredging Environment Protection Holdings' recently weak share price has pulled its P/S back below other Infrastructure companies. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of China Dredging Environment Protection Holdings revealed its shrinking revenue over the medium-term is contributing to its low P/S, given the industry is set to grow. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises either. Given the current circumstances, it seems unlikely that the share price will experience any significant movement in either direction in the near future if recent medium-term revenue trends persist.

It is also worth noting that we have found 2 warning signs for China Dredging Environment Protection Holdings (1 shouldn't be ignored!) that you need to take into consideration.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:871

China Dredging Environment Protection Holdings

An investment holding company, engages in dredging business in Mainland China and internationally.

Good value with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor