Advertisement

- Hong Kong

- /

- Infrastructure

- /

- SEHK:6119

We Discuss Why Tian Yuan Group Holdings Limited's (HKG:6119) CEO Will Find It Hard To Get A Pay Rise From Shareholders This Year

Key Insights

- Tian Yuan Group Holdings will host its Annual General Meeting on 3rd of June

- Total pay for CEO Jinming Yang includes CN¥744.0k salary

- The overall pay is comparable to the industry average

- Over the past three years, Tian Yuan Group Holdings' EPS grew by 18% and over the past three years, the total shareholder return was 3.5%

Under the guidance of CEO Jinming Yang, Tian Yuan Group Holdings Limited (HKG:6119) has performed reasonably well recently. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 3rd of June. Here is our take on why we think the CEO compensation looks appropriate.

Check out our latest analysis for Tian Yuan Group Holdings

How Does Total Compensation For Jinming Yang Compare With Other Companies In The Industry?

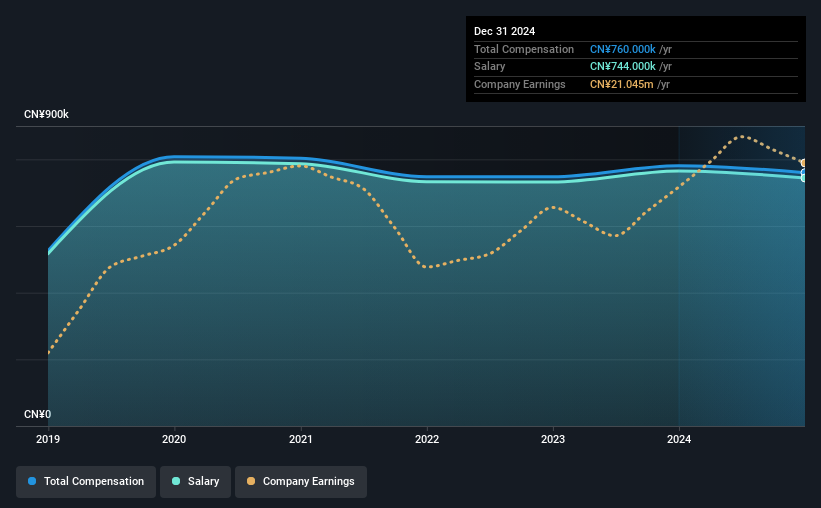

Our data indicates that Tian Yuan Group Holdings Limited has a market capitalization of HK$198m, and total annual CEO compensation was reported as CN¥760k for the year to December 2024. That's mostly flat as compared to the prior year's compensation. Notably, the salary which is CN¥744.0k, represents most of the total compensation being paid.

In comparison with other companies in the Hong Kong Infrastructure industry with market capitalizations under HK$1.6b, the reported median total CEO compensation was CN¥881k. This suggests that Tian Yuan Group Holdings remunerates its CEO largely in line with the industry average. What's more, Jinming Yang holds HK$140m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | CN¥744k | CN¥765k | 98% |

| Other | CN¥16k | CN¥16k | 2% |

| Total Compensation | CN¥760k | CN¥781k | 100% |

Speaking on an industry level, nearly 60% of total compensation represents salary, while the remainder of 40% is other remuneration. Tian Yuan Group Holdings pays a high salary, concentrating more on this aspect of compensation in comparison to non-salary pay. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Tian Yuan Group Holdings Limited's Growth

Tian Yuan Group Holdings Limited has seen its earnings per share (EPS) increase by 18% a year over the past three years. Its revenue is down 1.9% over the previous year.

Shareholders would be glad to know that the company has improved itself over the last few years. While it would be good to see revenue growth, profits matter more in the end. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Tian Yuan Group Holdings Limited Been A Good Investment?

With a total shareholder return of 3.5% over three years, Tian Yuan Group Holdings Limited has done okay by shareholders, but there's always room for improvement. As a result, investors in the company might be reluctant about agreeing to increase CEO pay in the future, before seeing an improvement on their returns.

To Conclude...

Tian Yuan Group Holdings pays its CEO a majority of compensation through a salary. Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. However, we still think that any proposed increase in CEO compensation will be examined closely to make sure the compensation is appropriate and linked to performance.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. That's why we did our research, and identified 2 warning signs for Tian Yuan Group Holdings (of which 1 makes us a bit uncomfortable!) that you should know about in order to have a holistic understanding of the stock.

Switching gears from Tian Yuan Group Holdings, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Valuation is complex, but we're here to simplify it.

Discover if Tian Yuan Group Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:6119

Tian Yuan Group Holdings

An investment holding company, provides bulk and general cargo uploading and unloading, and related ancillary port services in the People’s Republic of China.

Flawless balance sheet with low risk.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4729.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6410.8% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.8% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.71.9% undervalued

1341 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative