Advertisement

Here's Why Shareholders Should Examine Wong's International Holdings Limited's (HKG:99) CEO Compensation Package More Closely

Key Insights

- Wong's International Holdings to hold its Annual General Meeting on 28th of May

- Total pay for CEO Ben Wong includes HK$4.60m salary

- Total compensation is 201% above industry average

- Wong's International Holdings' three-year loss to shareholders was 35% while its EPS was down 112% over the past three years

Wong's International Holdings Limited (HKG:99) has not performed well recently and CEO Ben Wong will probably need to up their game. Shareholders can take the chance to hold the board and management accountable for the unsatisfactory performance at the next AGM on 28th of May. This will be also be a chance where they can challenge the board on company direction and vote on resolutions such as executive remuneration. The data we present below explains why we think CEO compensation is not consistent with recent performance.

Check out our latest analysis for Wong's International Holdings

Comparing Wong's International Holdings Limited's CEO Compensation With The Industry

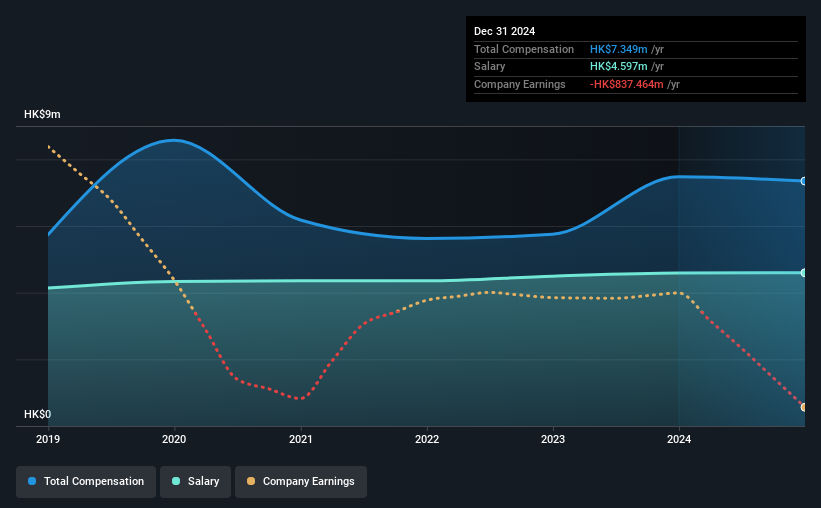

At the time of writing, our data shows that Wong's International Holdings Limited has a market capitalization of HK$555m, and reported total annual CEO compensation of HK$7.3m for the year to December 2024. That's mostly flat as compared to the prior year's compensation. We note that the salary portion, which stands at HK$4.60m constitutes the majority of total compensation received by the CEO.

In comparison with other companies in the Hong Kong Electronic industry with market capitalizations under HK$1.6b, the reported median total CEO compensation was HK$2.4m. This suggests that Ben Wong is paid more than the median for the industry. Moreover, Ben Wong also holds HK$203m worth of Wong's International Holdings stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | HK$4.6m | HK$4.6m | 63% |

| Other | HK$2.8m | HK$2.9m | 37% |

| Total Compensation | HK$7.3m | HK$7.5m | 100% |

Speaking on an industry level, nearly 79% of total compensation represents salary, while the remainder of 21% is other remuneration. Wong's International Holdings pays a modest slice of remuneration through salary, as compared to the broader industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Wong's International Holdings Limited's Growth

Over the last three years, Wong's International Holdings Limited has shrunk its earnings per share by 112% per year. In the last year, its revenue is down 16%.

The decline in EPS is a bit concerning. And the fact that revenue is down year on year arguably paints an ugly picture. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Wong's International Holdings Limited Been A Good Investment?

Few Wong's International Holdings Limited shareholders would feel satisfied with the return of -35% over three years. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

To Conclude...

Not only have shareholders not seen a favorable return on their investment, but the business hasn't performed well either. Few shareholders would be willing to award the CEO with a pay raise. At the upcoming AGM, the board will get the chance to explain the steps it plans to take to improve business performance.

CEO compensation can have a massive impact on performance, but it's just one element. That's why we did some digging and identified 2 warning signs for Wong's International Holdings that investors should think about before committing capital to this stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Wong's International Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:99

Wong's International Holdings

Through its subsidiaries, engages in the development, manufacture, marketing, and distribution of electronic products in Hong Kong, the rest of Asia, North America, and Europe.

Good value with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|7.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.8% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.4% undervalued

GM

Community Contributor