- Hong Kong

- /

- Electronic Equipment and Components

- /

- SEHK:8051

Why We’re Not Impressed By CircuTech International Holdings Limited’s (HKG:8051) 1.6% ROCE

Today we are going to look at CircuTech International Holdings Limited (HKG:8051) to see whether it might be an attractive investment prospect. To be precise, we'll consider its Return On Capital Employed (ROCE), as that will inform our view of the quality of the business.

First up, we'll look at what ROCE is and how we calculate it. Then we'll compare its ROCE to similar companies. Then we'll determine how its current liabilities are affecting its ROCE.

Return On Capital Employed (ROCE): What is it?

ROCE measures the amount of pre-tax profits a company can generate from the capital employed in its business. In general, businesses with a higher ROCE are usually better quality. In brief, it is a useful tool, but it is not without drawbacks. Renowned investment researcher Michael Mauboussin has suggested that a high ROCE can indicate that 'one dollar invested in the company generates value of more than one dollar'.

So, How Do We Calculate ROCE?

The formula for calculating the return on capital employed is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

Or for CircuTech International Holdings:

0.016 = HK$2.2m ÷ (HK$151m - HK$17m) (Based on the trailing twelve months to December 2019.)

Therefore, CircuTech International Holdings has an ROCE of 1.6%.

See our latest analysis for CircuTech International Holdings

Does CircuTech International Holdings Have A Good ROCE?

When making comparisons between similar businesses, investors may find ROCE useful. Using our data, CircuTech International Holdings's ROCE appears to be significantly below the 9.7% average in the Electronic industry. This performance could be negative if sustained, as it suggests the business may underperform its industry. Putting aside CircuTech International Holdings's performance relative to its industry, its ROCE in absolute terms is poor - considering the risk of owning stocks compared to government bonds. There are potentially more appealing investments elsewhere.

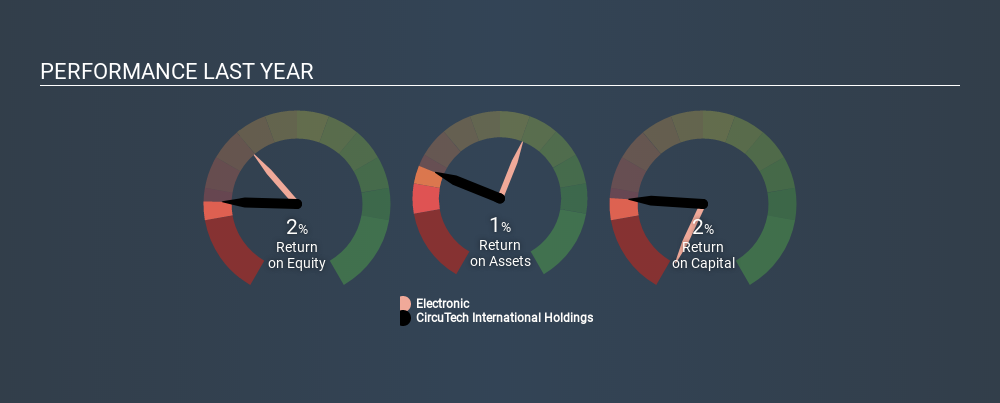

CircuTech International Holdings has an ROCE of 1.6%, but it didn't have an ROCE 3 years ago, since it was unprofitable. That implies the business has been improving. You can see in the image below how CircuTech International Holdings's ROCE compares to its industry. Click to see more on past growth.

When considering ROCE, bear in mind that it reflects the past and does not necessarily predict the future. ROCE can be deceptive for cyclical businesses, as returns can look incredible in boom times, and terribly low in downturns. ROCE is only a point-in-time measure. You can check if CircuTech International Holdings has cyclical profits by looking at this free graph of past earnings, revenue and cash flow.

What Are Current Liabilities, And How Do They Affect CircuTech International Holdings's ROCE?

Current liabilities include invoices, such as supplier payments, short-term debt, or a tax bill, that need to be paid within 12 months. Due to the way ROCE is calculated, a high level of current liabilities makes a company look as though it has less capital employed, and thus can (sometimes unfairly) boost the ROCE. To counteract this, we check if a company has high current liabilities, relative to its total assets.

CircuTech International Holdings has total assets of HK$151m and current liabilities of HK$17m. As a result, its current liabilities are equal to approximately 11% of its total assets. With a very reasonable level of current liabilities, so the impact on ROCE is fairly minimal.

The Bottom Line On CircuTech International Holdings's ROCE

CircuTech International Holdings has a poor ROCE, and there may be better investment prospects out there. Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with modest (or no) debt, trading on a P/E below 20.

For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About SEHK:8051

CircuTech International Holdings

An investment holding company, engages in sale and distribution of IT products, and provision of repair and other support services for IT products in Hong Kong, Japan, the United States, Australia, and internationally.

Flawless balance sheet with questionable track record.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion