- Hong Kong

- /

- Electronic Equipment and Components

- /

- SEHK:2166

Are Smart-Core Holdings' (HKG:2166) Statutory Earnings A Good Reflection Of Its Earnings Potential?

It might be old fashioned, but we really like to invest in companies that make a profit, each and every year. That said, the current statutory profit is not always a good guide to a company's underlying profitability. This article will consider whether Smart-Core Holdings' (HKG:2166) statutory profits are a good guide to its underlying earnings.

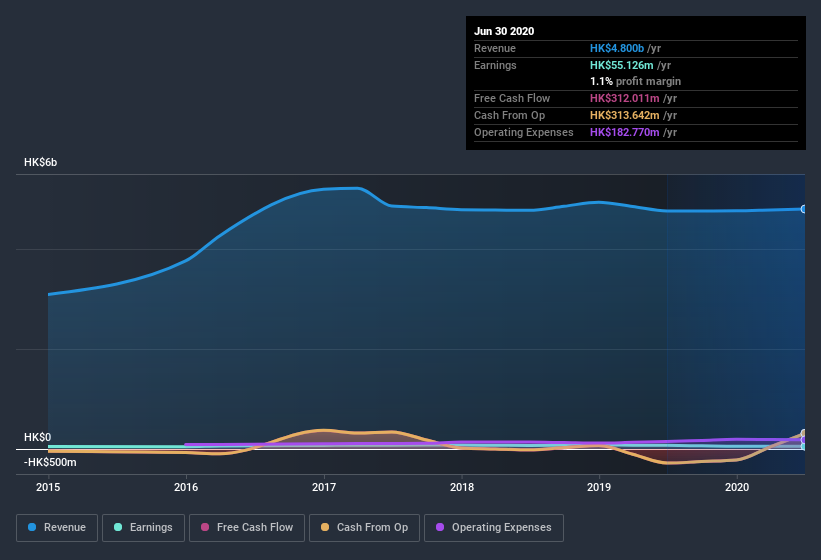

We like the fact that Smart-Core Holdings made a profit of HK$55.1m on its revenue of HK$4.80b, in the last year. In the last few years its profit has fallen, although its revenue was steady, as you can see in the chart below.

View our latest analysis for Smart-Core Holdings

Of course, when it comes to statutory profit, the devil is often in the detail, and we can get a better sense for a company by diving deeper into the financial statements. As a result, today we're going to take a closer look at Smart-Core Holdings' cashflow, and unusual items, with a view to understanding what these might tell us about its statutory profit. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Smart-Core Holdings.

Zooming In On Smart-Core Holdings' Earnings

In high finance, the key ratio used to measure how well a company converts reported profits into free cash flow (FCF) is the accrual ratio (from cashflow). The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

Over the twelve months to June 2020, Smart-Core Holdings recorded an accrual ratio of -0.31. Therefore, its statutory earnings were very significantly less than its free cashflow. To wit, it produced free cash flow of HK$312m during the period, dwarfing its reported profit of HK$55.1m. Given that Smart-Core Holdings had negative free cash flow in the prior corresponding period, the trailing twelve month resul of HK$312m would seem to be a step in the right direction. However, that's not all there is to consider. The accrual ratio is reflecting the impact of unusual items on statutory profit, at least in part.

The Impact Of Unusual Items On Profit

Surprisingly, given Smart-Core Holdings' accrual ratio implied strong cash conversion, its paper profit was actually boosted by HK$6.8m in unusual items. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. We ran the numbers on most publicly listed companies worldwide, and it's very common for unusual items to be once-off in nature. And that's as you'd expect, given these boosts are described as 'unusual'. If Smart-Core Holdings doesn't see that contribution repeat, then all else being equal we'd expect its profit to drop over the current year.

Our Take On Smart-Core Holdings' Profit Performance

Smart-Core Holdings' profits got a boost from unusual items, which indicates they might not be sustained and yet its accrual ratio still indicated solid cash conversion, which is promising. Considering all the aforementioned, we'd venture that Smart-Core Holdings' profit result is a pretty good guide to its true profitability, albeit a bit on the conservative side. If you'd like to know more about Smart-Core Holdings as a business, it's important to be aware of any risks it's facing. Be aware that Smart-Core Holdings is showing 4 warning signs in our investment analysis and 1 of those makes us a bit uncomfortable...

Our examination of Smart-Core Holdings has focussed on certain factors that can make its earnings look better than they are. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

When trading Smart-Core Holdings or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:2166

Smart-Core Holdings

An investment holding company, distributes integrated circuits and other electronic components in the Hong Kong, People’s Republic of China, Singapore, Japan, and internationally.

Slight risk and fair value.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion