- Hong Kong

- /

- Electronic Equipment and Components

- /

- SEHK:1888

Kingboard Laminates Holdings Limited's (HKG:1888) On An Uptrend But Financial Prospects Look Pretty Weak: Is The Stock Overpriced?

Kingboard Laminates Holdings (HKG:1888) has had a great run on the share market with its stock up by a significant 39% over the last three months. We, however wanted to have a closer look at its key financial indicators as the markets usually pay for long-term fundamentals, and in this case, they don't look very promising. In this article, we decided to focus on Kingboard Laminates Holdings' ROE.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Put another way, it reveals the company's success at turning shareholder investments into profits.

View our latest analysis for Kingboard Laminates Holdings

How Do You Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Kingboard Laminates Holdings is:

6.1% = HK$909m ÷ HK$15b (Based on the trailing twelve months to December 2023).

The 'return' refers to a company's earnings over the last year. One way to conceptualize this is that for each HK$1 of shareholders' capital it has, the company made HK$0.06 in profit.

What Has ROE Got To Do With Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

A Side By Side comparison of Kingboard Laminates Holdings' Earnings Growth And 6.1% ROE

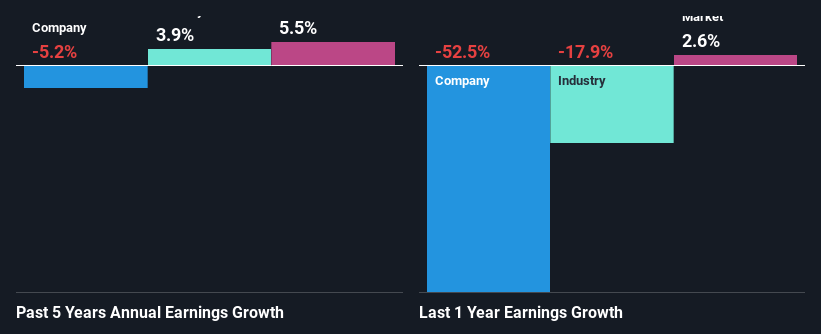

On the face of it, Kingboard Laminates Holdings' ROE is not much to talk about. However, its ROE is similar to the industry average of 5.9%, so we won't completely dismiss the company. Having said that, Kingboard Laminates Holdings' five year net income decline rate was 5.2%. Remember, the company's ROE is a bit low to begin with. Hence, this goes some way in explaining the shrinking earnings.

So, as a next step, we compared Kingboard Laminates Holdings' performance against the industry and were disappointed to discover that while the company has been shrinking its earnings, the industry has been growing its earnings at a rate of 3.9% over the last few years.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Kingboard Laminates Holdings is trading on a high P/E or a low P/E, relative to its industry.

Is Kingboard Laminates Holdings Efficiently Re-investing Its Profits?

Kingboard Laminates Holdings' declining earnings is not surprising given how the company is spending most of its profits in paying dividends, judging by its three-year median payout ratio of 69% (or a retention ratio of 31%). The business is only left with a small pool of capital to reinvest - A vicious cycle that doesn't benefit the company in the long-run.

Additionally, Kingboard Laminates Holdings has paid dividends over a period of at least ten years, which means that the company's management is determined to pay dividends even if it means little to no earnings growth. Existing analyst estimates suggest that the company's future payout ratio is expected to drop to 44% over the next three years. Accordingly, the expected drop in the payout ratio explains the expected increase in the company's ROE to 18%, over the same period.

Summary

In total, we would have a hard think before deciding on any investment action concerning Kingboard Laminates Holdings. As a result of its low ROE and lack of much reinvestment into the business, the company has seen a disappointing earnings growth rate. That being so, the latest industry analyst forecasts show that the analysts are expecting to see a huge improvement in the company's earnings growth rate. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

Valuation is complex, but we're here to simplify it.

Discover if Kingboard Laminates Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1888

Kingboard Laminates Holdings

An investment holding company, manufactures and sells laminates in the People's Republic of China, Europe, other Asian countries, and the United States.

Excellent balance sheet with reasonable growth potential.