Advertisement

- Hong Kong

- /

- Communications

- /

- SEHK:1617

This Is Why Nanfang Communication Holdings Limited's (HKG:1617) CEO Can Expect A Bump Up In Their Pay Packet

Key Insights

- Nanfang Communication Holdings will host its Annual General Meeting on 25th of June

- Salary of CN¥666.0k is part of CEO Ming Shi's total remuneration

- Total compensation is 40% below industry average

- Nanfang Communication Holdings' total shareholder return over the past three years was 22% while its EPS grew by 128% over the past three years

Shareholders will probably not be disappointed by the robust results at Nanfang Communication Holdings Limited (HKG:1617) recently and they will be keeping this in mind as they go into the AGM on 25th of June. They will probably be more interested in hearing the board discuss future initiatives to further improve the business as they vote on resolutions such as executive remuneration. In our analysis below, we discuss why we think the CEO compensation looks acceptable and the case for a raise.

View our latest analysis for Nanfang Communication Holdings

How Does Total Compensation For Ming Shi Compare With Other Companies In The Industry?

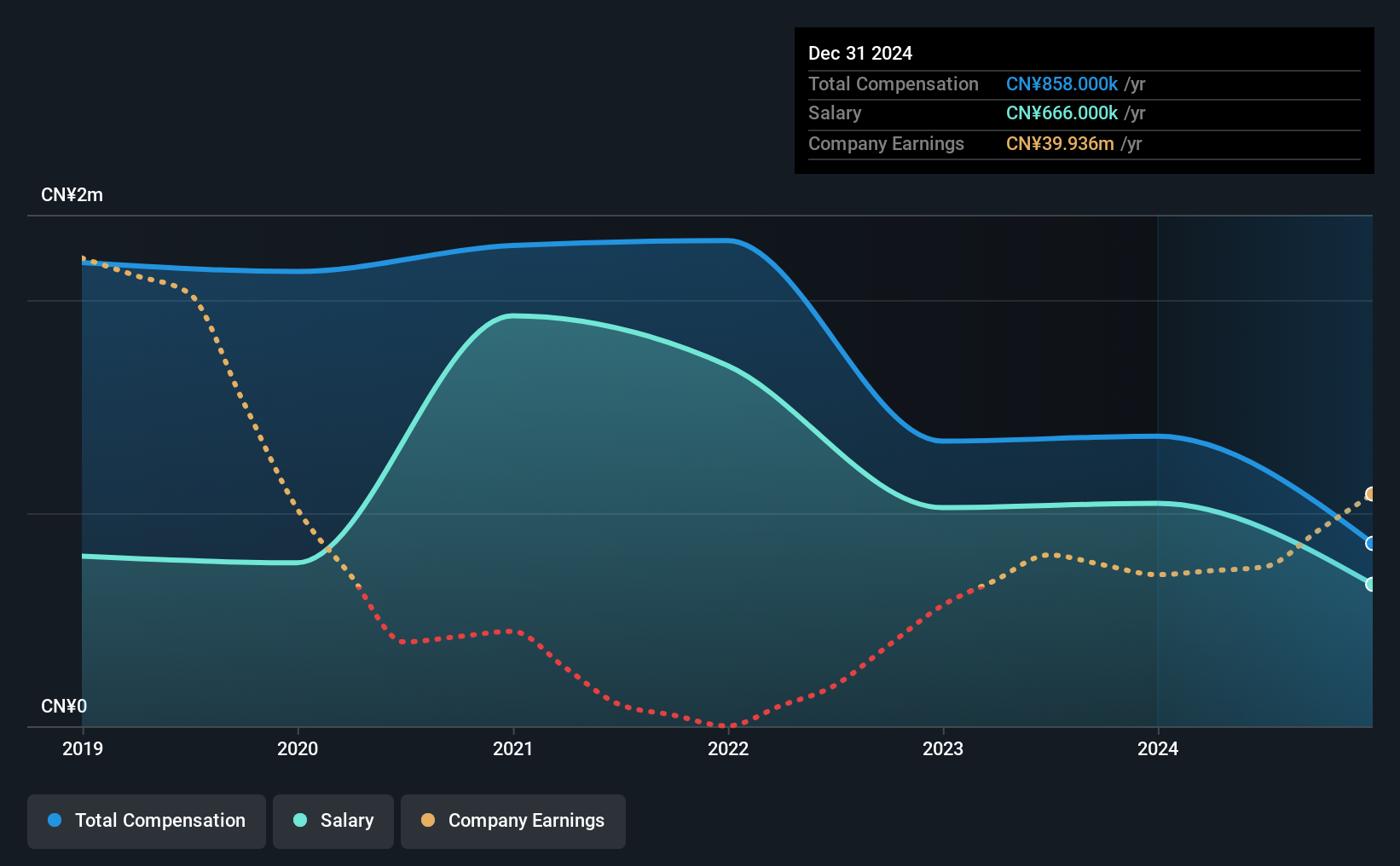

According to our data, Nanfang Communication Holdings Limited has a market capitalization of HK$195m, and paid its CEO total annual compensation worth CN¥858k over the year to December 2024. We note that's a decrease of 37% compared to last year. Notably, the salary which is CN¥666.0k, represents most of the total compensation being paid.

In comparison with other companies in the Hong Kong Communications industry with market capitalizations under HK$1.6b, the reported median total CEO compensation was CN¥1.4m. In other words, Nanfang Communication Holdings pays its CEO lower than the industry median. What's more, Ming Shi holds HK$6.7m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | CN¥666k | CN¥1.0m | 78% |

| Other | CN¥192k | CN¥315k | 22% |

| Total Compensation | CN¥858k | CN¥1.4m | 100% |

Talking in terms of the industry, salary represented approximately 66% of total compensation out of all the companies we analyzed, while other remuneration made up 34% of the pie. It's interesting to note that Nanfang Communication Holdings pays out a greater portion of remuneration through salary, compared to the industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Nanfang Communication Holdings Limited's Growth

Nanfang Communication Holdings Limited's earnings per share (EPS) grew 128% per year over the last three years. In the last year, its revenue is up 3.0%.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's good to see a bit of revenue growth, as this suggests the business is able to grow sustainably. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Nanfang Communication Holdings Limited Been A Good Investment?

Nanfang Communication Holdings Limited has served shareholders reasonably well, with a total return of 22% over three years. But they would probably prefer not to see CEO compensation far in excess of the median.

In Summary...

While the company seems to be headed in the right direction performance-wise, there's always room for improvement. If it manages to keep up the current streak, CEO remuneration could well be one of shareholders' least concerns. In fact, strategic decisions that could impact the future of the business might be a far more interesting topic for investors as it would help them set their longer-term expectations.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We've identified 1 warning sign for Nanfang Communication Holdings that investors should be aware of in a dynamic business environment.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

Valuation is complex, but we're here to simplify it.

Discover if Nanfang Communication Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1617

Nanfang Communication Holdings

An investment holding company, engages in the manufacturing and sale of optical fiber cables and optical distribution network devices in the People’s Republic of China.

Proven track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor