- Thailand

- /

- Real Estate

- /

- SET:PSH

Uncovering 3 Stocks Considered Undervalued Based On Current Estimates

Reviewed by Simply Wall St

As global markets navigate a mixed start to the new year, with U.S. stocks experiencing both gains and declines and notable economic indicators like the Chicago PMI showing contraction, investors are keenly observing opportunities for value amidst volatility. In such an environment, identifying undervalued stocks can be particularly appealing as these equities may offer potential for growth when broader market conditions stabilize or improve.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Avant Group (TSE:3836) | ¥1878.00 | ¥3755.66 | 50% |

| NBTM New Materials Group (SHSE:600114) | CN¥15.55 | CN¥31.07 | 49.9% |

| Gaming Realms (AIM:GMR) | £0.36 | £0.72 | 49.9% |

| Sudarshan Chemical Industries (BSE:506655) | ₹1120.30 | ₹2232.36 | 49.8% |

| Kinaxis (TSX:KXS) | CA$170.99 | CA$340.11 | 49.7% |

| ReadyTech Holdings (ASX:RDY) | A$3.15 | A$6.30 | 50% |

| Vogo (ENXTPA:ALVGO) | €2.94 | €5.87 | 49.9% |

| Exosens (ENXTPA:EXENS) | €22.505 | €44.77 | 49.7% |

| iFLYTEKLTD (SZSE:002230) | CN¥45.41 | CN¥90.65 | 49.9% |

| Salmones Camanchaca (SNSE:SALMOCAM) | CLP2434.90 | CLP4848.26 | 49.8% |

Let's dive into some prime choices out of the screener.

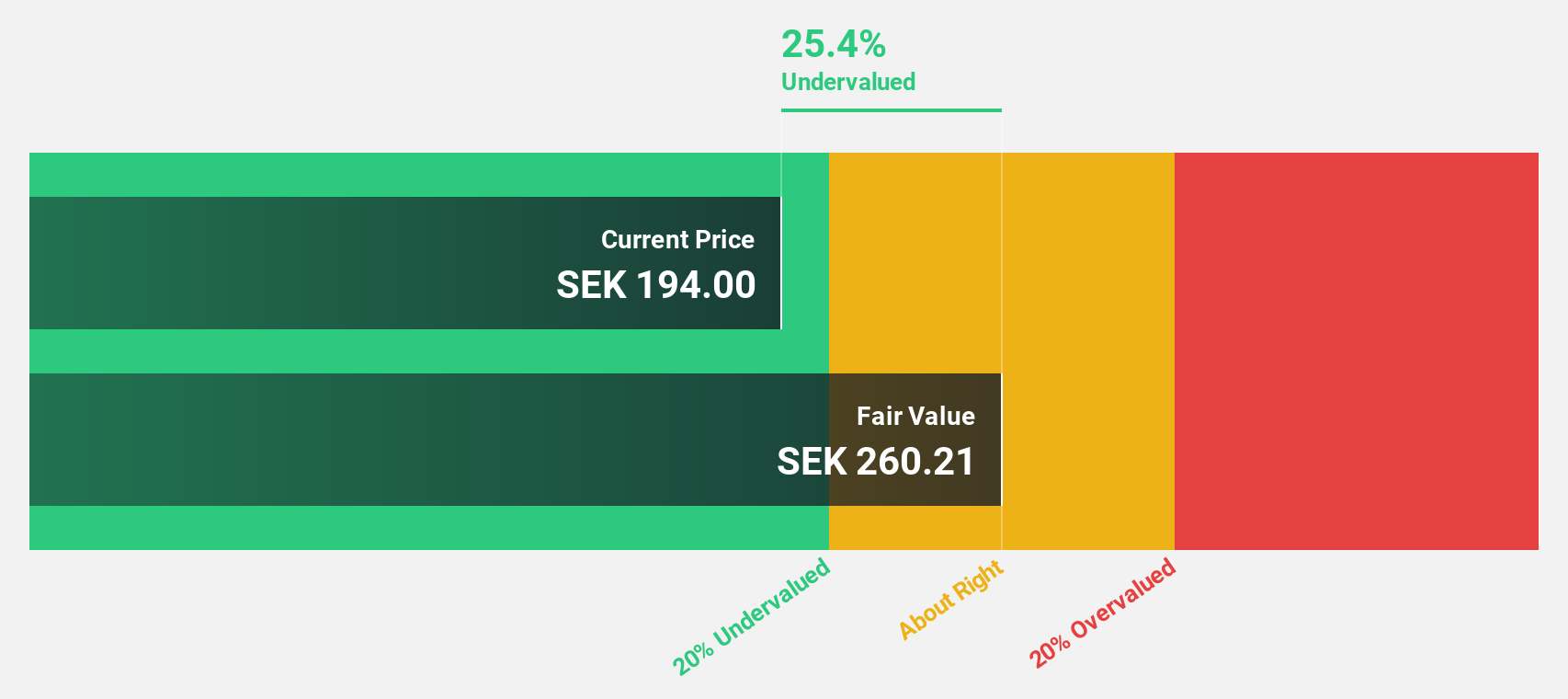

CellaVision (OM:CEVI)

Overview: CellaVision AB (publ) develops and sells instruments, software, and reagents for blood and body fluids analysis in Sweden and internationally, with a market cap of SEK4.93 billion.

Operations: The company's revenue is primarily derived from automated microscopy systems and reagents in the field of hematology, totaling SEK737.16 million.

Estimated Discount To Fair Value: 39.3%

CellaVision AB is trading at SEK 206.5, significantly below its estimated fair value of SEK 340.38, indicating substantial undervaluation based on cash flows. The company reported strong earnings growth of 33.9% over the past year and forecasts suggest continued robust earnings growth at 22.5% annually, outpacing the Swedish market's average growth rate. Recent financial results show increased revenues and net income for Q3 and nine months ending September 2024, reinforcing its positive cash flow outlook.

- Insights from our recent growth report point to a promising forecast for CellaVision's business outlook.

- Take a closer look at CellaVision's balance sheet health here in our report.

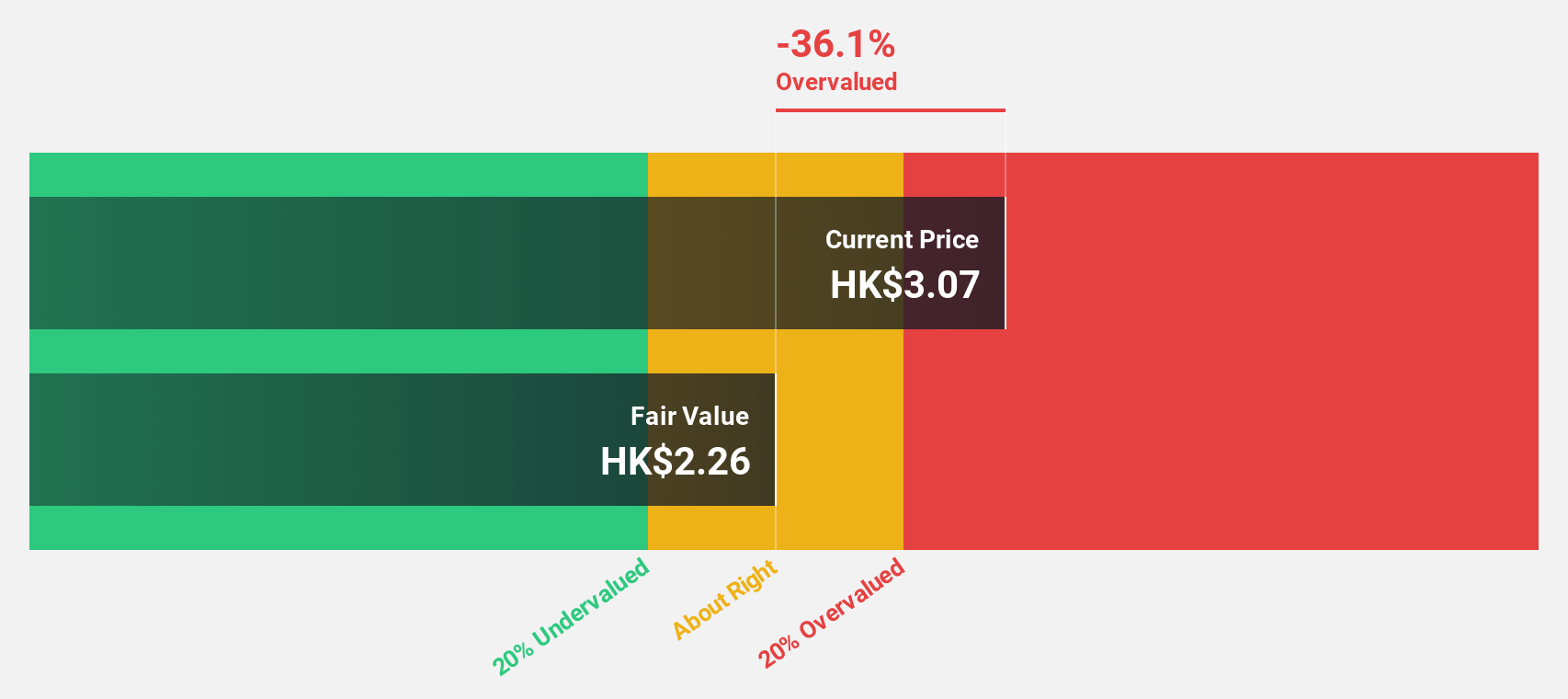

Digital China Holdings (SEHK:861)

Overview: Digital China Holdings Limited is an investment holding company that offers big data products and solutions to government and enterprise customers mainly in Mainland China, with a market capitalization of approximately HK$5.20 billion.

Operations: The company's revenue is derived from three main segments: Big Data Products and Solutions (CN¥3.39 billion), Software and Operating Services (CN¥5.31 billion), and Traditional and Localization Services (CN¥10.03 billion).

Estimated Discount To Fair Value: 46.2%

Digital China Holdings is trading at HK$3.11, significantly below its estimated fair value of HK$5.78, highlighting potential undervaluation based on cash flows. The company is projected to achieve profitability within three years, with revenue growth forecasted at 8.8% annually—outpacing the Hong Kong market's average rate of 7.5%. Despite a low future return on equity of 7.6%, Digital China presents good relative value compared to peers and industry standards.

- Our growth report here indicates Digital China Holdings may be poised for an improving outlook.

- Click here and access our complete balance sheet health report to understand the dynamics of Digital China Holdings.

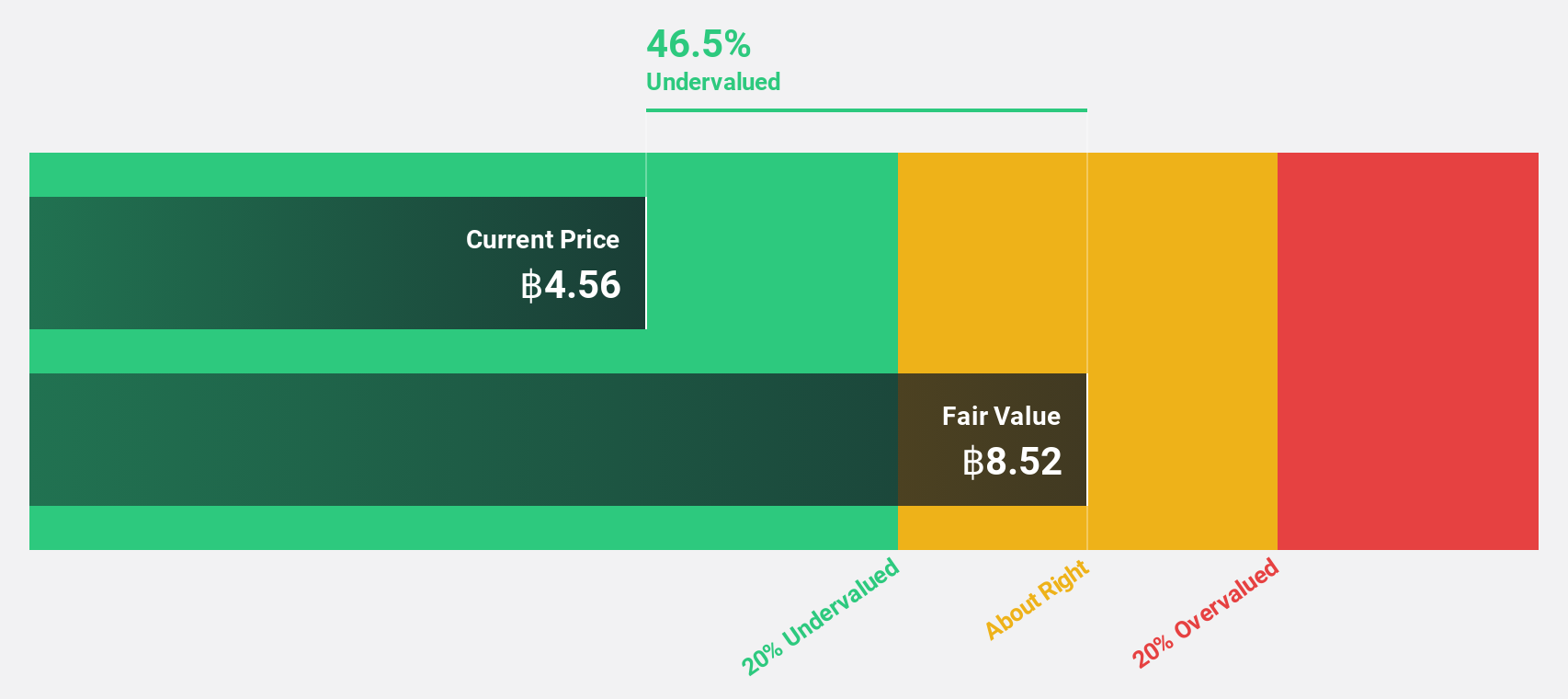

Pruksa Holding (SET:PSH)

Overview: Pruksa Holding Public Company Limited, with a market cap of THB15.76 billion, operates through its subsidiaries to develop and sell residential real estate properties in Thailand.

Operations: The company's revenue segments include SBU Hospital with THB2.32 billion, SBU Townhouse with THB6.32 billion, SBU Condominium with THB5.74 billion, and SBU Single House with THB6.43 billion.

Estimated Discount To Fair Value: 11.4%

Pruksa Holding, trading at THB7.2, is slightly undervalued compared to its fair value of THB8.13 based on cash flows. Earnings are expected to grow significantly at 28.4% annually, surpassing the Thai market's average growth rate of 16.6%. However, profit margins have declined from 11.3% last year to 4.3%, and the dividend yield of 11.11% is not well covered by earnings, indicating potential risks despite promising revenue growth forecasts of 8.9%.

- According our earnings growth report, there's an indication that Pruksa Holding might be ready to expand.

- Dive into the specifics of Pruksa Holding here with our thorough financial health report.

Next Steps

- Discover the full array of 885 Undervalued Stocks Based On Cash Flows right here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SET:PSH

Pruksa Holding

Through its subsidiaries, develops and sells residential real estate properties in Thailand.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Clarivate Stock: When Data Becomes the Backbone of Innovation and Law

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

MicroVision will explode future revenue by 380.37% with a vision towards success

Trending Discussion