Advertisement

There are a few key trends to look for if we want to identify the next multi-bagger. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. In light of that, when we looked at GET Holdings (HKG:8100) and its ROCE trend, we weren't exactly thrilled.

What Is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on GET Holdings is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

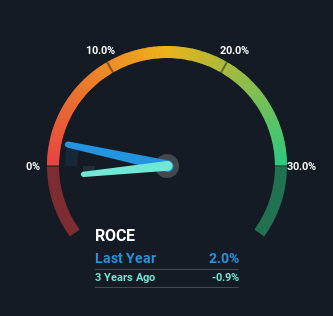

0.02 = HK$5.3m ÷ (HK$299m - HK$38m) (Based on the trailing twelve months to September 2023).

Therefore, GET Holdings has an ROCE of 2.0%. Ultimately, that's a low return and it under-performs the Software industry average of 6.7%.

Check out our latest analysis for GET Holdings

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating GET Holdings' past further, check out this free graph of past earnings, revenue and cash flow.

What Can We Tell From GET Holdings' ROCE Trend?

We're a bit concerned with the trends, because the business is applying 45% less capital than it was five years ago and returns on that capital have stayed flat. To us that doesn't look like a multi-bagger because the company appears to be selling assets and it's returns aren't increasing. Not only that, but the low returns on this capital mentioned earlier would leave most investors unimpressed.

The Key Takeaway

It's a shame to see that GET Holdings is effectively shrinking in terms of its capital base. And investors appear hesitant that the trends will pick up because the stock has fallen 62% in the last five years. Therefore based on the analysis done in this article, we don't think GET Holdings has the makings of a multi-bagger.

If you'd like to know about the risks facing GET Holdings, we've discovered 1 warning sign that you should be aware of.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:8100

Famous Tech International Holdings

An investment holding company, engages in the research, development, and distribution of personal computer performance software, anti-virus software, mobile phone applications, and toolbar advertisements.

Flawless balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor