Advertisement

Is China e-Wallet Payment Group (HKG:802) Using Debt In A Risky Way?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that China e-Wallet Payment Group Limited (HKG:802) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

Our analysis indicates that 802 is potentially overvalued!

What Is China e-Wallet Payment Group's Net Debt?

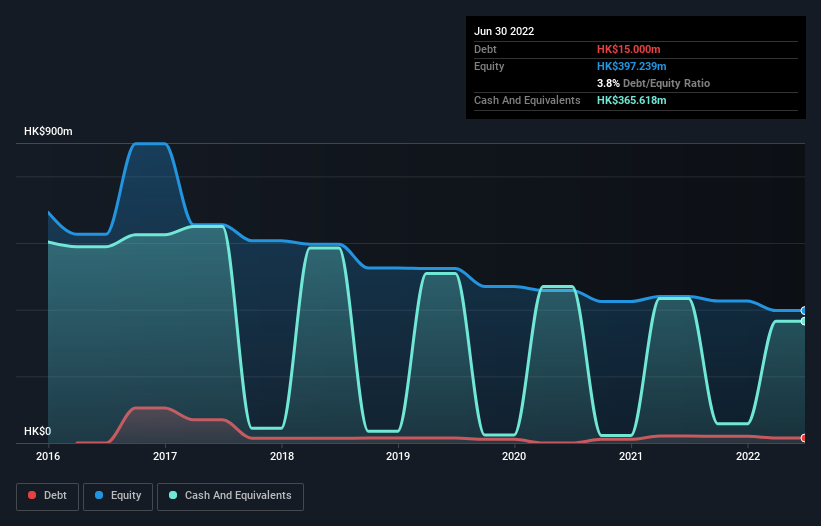

As you can see below, China e-Wallet Payment Group had HK$15.0m of debt at June 2022, down from HK$21.0m a year prior. But on the other hand it also has HK$365.6m in cash, leading to a HK$350.6m net cash position.

A Look At China e-Wallet Payment Group's Liabilities

We can see from the most recent balance sheet that China e-Wallet Payment Group had liabilities of HK$21.9m falling due within a year, and liabilities of HK$17.3m due beyond that. On the other hand, it had cash of HK$365.6m and HK$47.9m worth of receivables due within a year. So it can boast HK$374.4m more liquid assets than total liabilities.

This luscious liquidity implies that China e-Wallet Payment Group's balance sheet is sturdy like a giant sequoia tree. On this view, lenders should feel as safe as the beloved of a black-belt karate master. Succinctly put, China e-Wallet Payment Group boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since China e-Wallet Payment Group will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Over 12 months, China e-Wallet Payment Group made a loss at the EBIT level, and saw its revenue drop to HK$89m, which is a fall of 13%. We would much prefer see growth.

So How Risky Is China e-Wallet Payment Group?

Statistically speaking companies that lose money are riskier than those that make money. And we do note that China e-Wallet Payment Group had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of HK$74m and booked a HK$50m accounting loss. While this does make the company a bit risky, it's important to remember it has net cash of HK$350.6m. That means it could keep spending at its current rate for more than two years. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. To that end, you should be aware of the 2 warning signs we've spotted with China e-Wallet Payment Group .

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:802

China e-Wallet Payment Group

An investment holding company, primarily engages in the internet and mobile’s application, and related accessories business in Hong Kong and the People’s Republic of China.

Excellent balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor