Advertisement

- China

- /

- Metals and Mining

- /

- SZSE:002988

Insider-Led Growth Stocks To Watch In December 2024

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate the complexities of interest rate adjustments and political uncertainties, investors are closely watching how these factors impact major indices. Despite recent declines in U.S. stocks and broader market volatility driven by cautious Fed commentary, opportunities for growth remain, particularly in companies with strong insider ownership that can leverage their leadership's vested interests to drive long-term success. In such an environment, stocks led by insiders who have a significant stake may offer a compelling proposition due to their alignment with shareholder interests and potential resilience amidst fluctuating economic conditions.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Arctech Solar Holding (SHSE:688408) | 37.9% | 25.6% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.9% | 39.9% |

| People & Technology (KOSDAQ:A137400) | 16.4% | 37.3% |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 41.3% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 26.3% |

| Laopu Gold (SEHK:6181) | 36.4% | 34.2% |

| Plenti Group (ASX:PLT) | 12.8% | 120.1% |

| Brightstar Resources (ASX:BTR) | 16.2% | 84.5% |

| Findi (ASX:FND) | 34.8% | 112.9% |

Let's uncover some gems from our specialized screener.

Pharma Mar (BME:PHM)

Simply Wall St Growth Rating: ★★★★★★

Overview: Pharma Mar, S.A. is a biopharmaceutical company focused on the research, development, production, and commercialization of bio-active principles for oncology across various international markets with a market cap of €1.40 billion.

Operations: The company's revenue primarily comes from its oncology segment, generating €154.75 million.

Insider Ownership: 11.8%

Pharma Mar demonstrates potential as a growth company with high insider ownership, despite recent volatility. Its earnings are forecast to grow significantly at 56.19% annually, outpacing the Spanish market. The company's revenue is also expected to rise by 25.4% per year. Recent positive trial results for Zepzelca® could bolster future growth prospects, although profit margins have declined from 8.3% to 0.4%. Trading at a substantial discount to its estimated fair value enhances its appeal for investors seeking undervalued opportunities with growth potential.

- Get an in-depth perspective on Pharma Mar's performance by reading our analyst estimates report here.

- Our valuation report unveils the possibility Pharma Mar's shares may be trading at a premium.

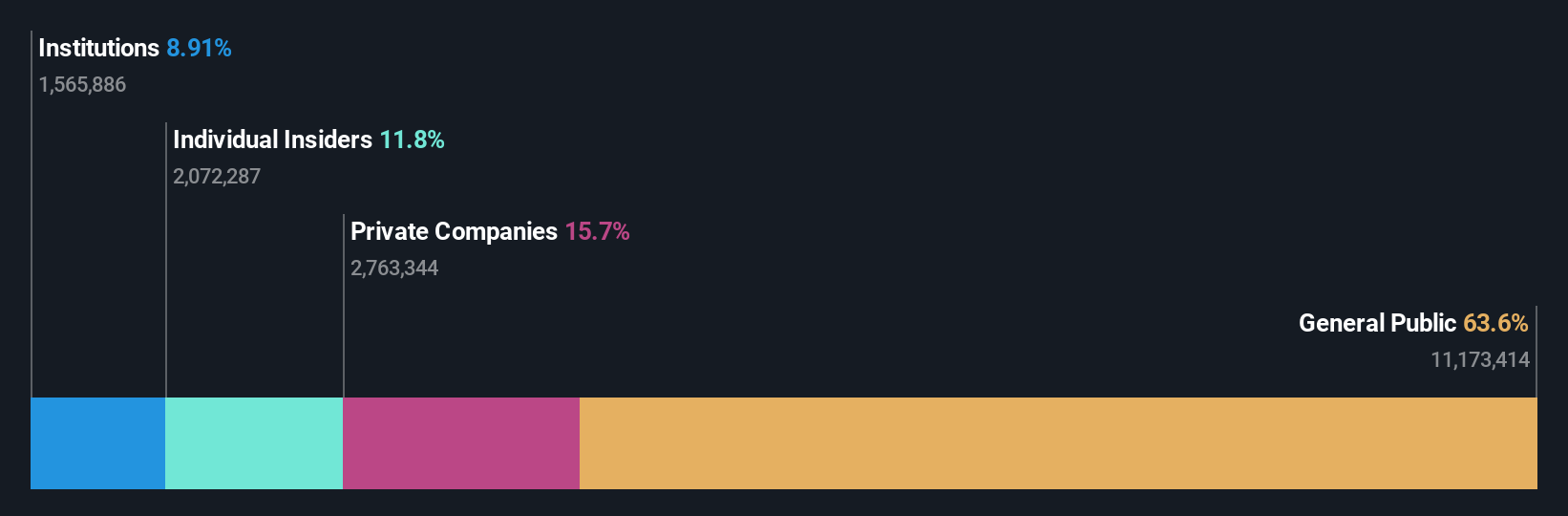

Beijing Fourth Paradigm Technology (SEHK:6682)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Beijing Fourth Paradigm Technology Co., Ltd. is an investment holding company offering platform-centric artificial intelligence solutions in China, with a market cap of HK$23.97 billion.

Operations: The company's revenue segments include CN¥3 billion from the Sage AI Platform, CN¥448.10 million from Sagegpt Aigs Services, and CN¥1.15 billion from Shift Intelligent Solutions.

Insider Ownership: 22.8%

Beijing Fourth Paradigm Technology shows promise with its earnings forecasted to grow 113.12% annually, significantly outpacing the Hong Kong market's average growth. Despite a highly volatile share price recently, the company is expected to become profitable within three years. However, revenue growth at 19.3% per year is slower than some high-growth benchmarks but still surpasses the broader market's rate of 7.8%. No substantial insider trading activity has been reported in recent months.

- Click here and access our complete growth analysis report to understand the dynamics of Beijing Fourth Paradigm Technology.

- The valuation report we've compiled suggests that Beijing Fourth Paradigm Technology's current price could be inflated.

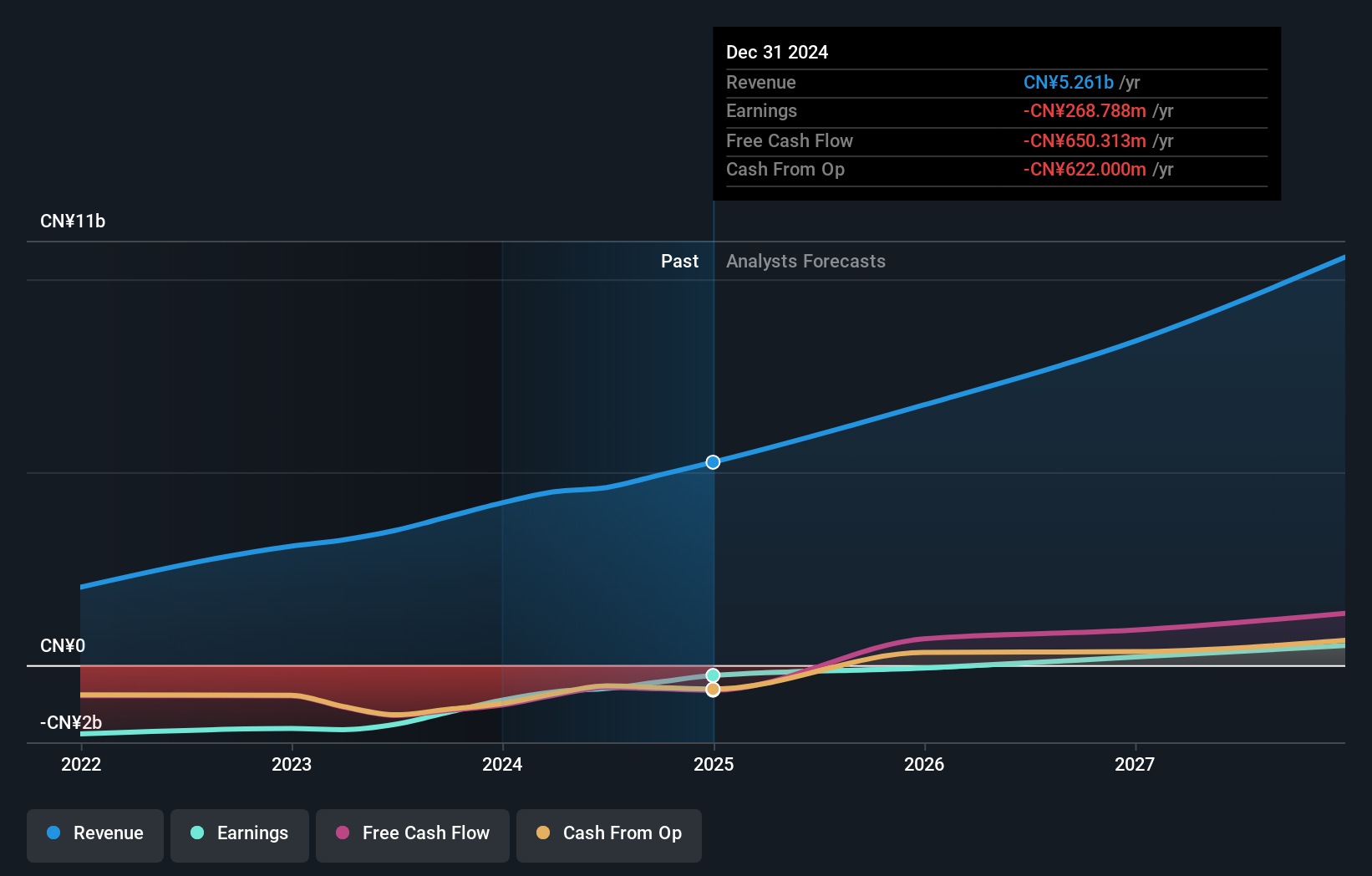

Guangdong Haomei New MaterialsLtd (SZSE:002988)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Guangdong Haomei New Materials Co., Ltd. engages in the research, development, manufacture, and sale of aluminum profiles in China with a market cap of CN¥5.18 billion.

Operations: The company generates revenue primarily from the research, development, manufacture, and sale of aluminum profiles in China.

Insider Ownership: 23.2%

Guangdong Haomei New Materials Ltd. demonstrates robust growth potential, with earnings forecasted to increase by 27.3% annually, surpassing the Chinese market's average. Recent earnings reports show a rise in net income to CNY 171.81 million for the first nine months of 2024, up from CNY 124.26 million last year. The company completed a share buyback worth CNY 45 million, enhancing shareholder value despite past dilution concerns and limited insider trading activity recently.

- Take a closer look at Guangdong Haomei New MaterialsLtd's potential here in our earnings growth report.

- In light of our recent valuation report, it seems possible that Guangdong Haomei New MaterialsLtd is trading behind its estimated value.

Make It Happen

- Explore the 1512 names from our Fast Growing Companies With High Insider Ownership screener here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002988

Guangdong Haomei New MaterialsLtd

Researches, develops, manufactures and sells aluminum profiles in China.

Mediocre balance sheet with limited growth.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% undervalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|45.0% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|20.4% undervalued

TI

Community Contributor