Advertisement

- Hong Kong

- /

- Semiconductors

- /

- SEHK:1665

How Does Pentamaster International's (HKG:1665) P/E Compare To Its Industry, After Its Big Share Price Gain?

Pentamaster International (HKG:1665) shares have continued recent momentum with a 30% gain in the last month alone. And the full year gain of 35% isn't too shabby, either!

All else being equal, a sharp share price increase should make a stock less attractive to potential investors. In the long term, share prices tend to follow earnings per share, but in the short term prices bounce around in response to short term factors (which are not always obvious). So some would prefer to hold off buying when there is a lot of optimism towards a stock. One way to gauge market expectations of a stock is to look at its Price to Earnings Ratio (PE Ratio). A high P/E implies that investors have high expectations of what a company can achieve compared to a company with a low P/E ratio.

See our latest analysis for Pentamaster International

Does Pentamaster International Have A Relatively High Or Low P/E For Its Industry?

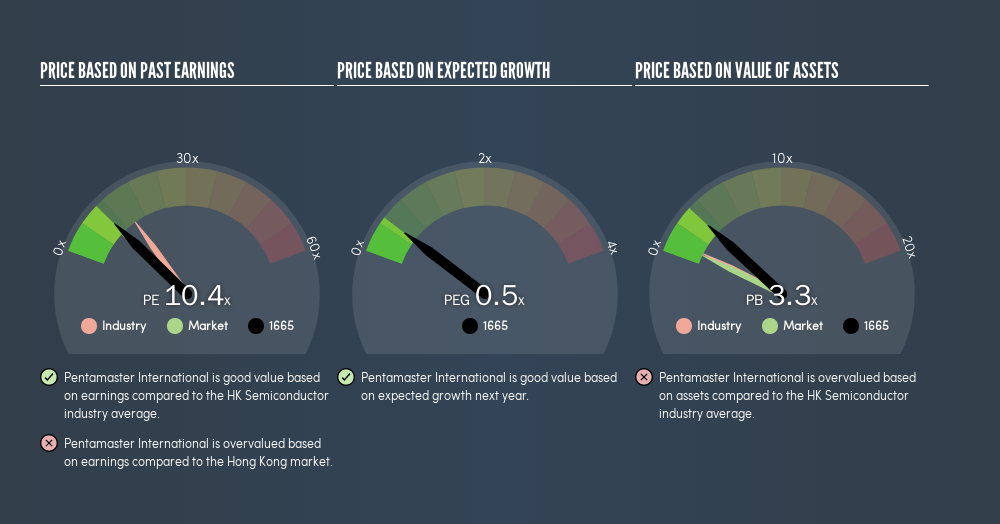

We can tell from its P/E ratio of 10.35 that sentiment around Pentamaster International isn't particularly high. If you look at the image below, you can see Pentamaster International has a lower P/E than the average (14.7) in the semiconductor industry classification.

This suggests that market participants think Pentamaster International will underperform other companies in its industry.

How Growth Rates Impact P/E Ratios

Probably the most important factor in determining what P/E a company trades on is the earnings growth. If earnings are growing quickly, then the 'E' in the equation will increase faster than it would otherwise. Therefore, even if you pay a high multiple of earnings now, that multiple will become lower in the future. And as that P/E ratio drops, the company will look cheap, unless its share price increases.

In the last year, Pentamaster International grew EPS like Taylor Swift grew her fan base back in 2010; the 63% gain was both fast and well deserved.

Don't Forget: The P/E Does Not Account For Debt or Bank Deposits

The 'Price' in P/E reflects the market capitalization of the company. That means it doesn't take debt or cash into account. In theory, a company can lower its future P/E ratio by using cash or debt to invest in growth.

Such expenditure might be good or bad, in the long term, but the point here is that the balance sheet is not reflected by this ratio.

How Does Pentamaster International's Debt Impact Its P/E Ratio?

With net cash of RM286m, Pentamaster International has a very strong balance sheet, which may be important for its business. Having said that, at 24% of its market capitalization the cash hoard would contribute towards a higher P/E ratio.

The Verdict On Pentamaster International's P/E Ratio

Pentamaster International has a P/E of 10.4. That's around the same as the average in the HK market, which is 9.7. The excess cash it carries is the gravy on top its fast EPS growth. So based on this analysis we'd expect Pentamaster International to have a higher P/E ratio. Because analysts are even expecting further profit growth, we would venture this stock is worth a closer look.. What we know for sure is that investors have become much more excited about Pentamaster International recently, since they have pushed its P/E ratio from 7.9 to 10.4 over the last month. If you like to buy stocks that have recently impressed the market, then this one might be a candidate; but if you prefer to invest when there is 'blood in the streets', then you may feel the opportunity has passed.

When the market is wrong about a stock, it gives savvy investors an opportunity. If the reality for a company is better than it expects, you can make money by buying and holding for the long term. So this free visualization of the analyst consensus on future earnings could help you make the right decision about whether to buy, sell, or hold.

But note: Pentamaster International may not be the best stock to buy. So take a peek at this free list of interesting companies with strong recent earnings growth (and a P/E ratio below 20).

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About SEHK:1665

Pentamaster International

An investment holding company, provides automation manufacturing and technology solutions in Malaysia and internationally.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor