Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Tree Holdings Limited (HKG:8395) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Tree Holdings

How Much Debt Does Tree Holdings Carry?

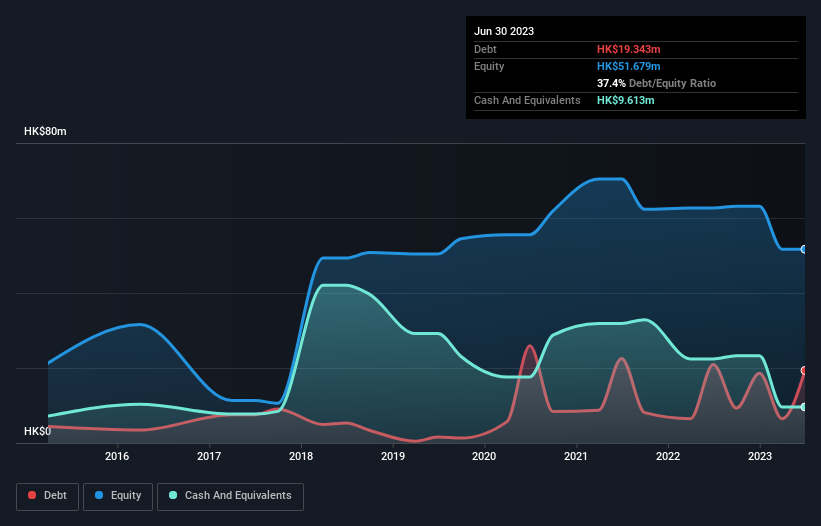

You can click the graphic below for the historical numbers, but it shows that Tree Holdings had HK$19.3m of debt in March 2023, down from HK$20.9m, one year before. On the flip side, it has HK$9.61m in cash leading to net debt of about HK$9.73m.

A Look At Tree Holdings' Liabilities

The latest balance sheet data shows that Tree Holdings had liabilities of HK$43.4m due within a year, and liabilities of HK$4.68m falling due after that. Offsetting this, it had HK$9.61m in cash and HK$42.6m in receivables that were due within 12 months. So it actually has HK$4.15m more liquid assets than total liabilities.

Having regard to Tree Holdings' size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the HK$1.30b company is struggling for cash, we still think it's worth monitoring its balance sheet. Carrying virtually no net debt, Tree Holdings has a very light debt load indeed. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Tree Holdings will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Tree Holdings had a loss before interest and tax, and actually shrunk its revenue by 13%, to HK$76m. That's not what we would hope to see.

Caveat Emptor

While Tree Holdings's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Indeed, it lost HK$3.4m at the EBIT level. Looking on the brighter side, the business has adequate liquid assets, which give it time to grow and develop before its debt becomes a near-term issue. But we'd want to see some positive free cashflow before spending much time on trying to understand the stock. So it seems too risky for our taste. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should be aware of the 1 warning sign we've spotted with Tree Holdings .

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if ZXZN Qi-House Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:8395

ZXZN Qi-House Holdings

Engages in the sale, distribution, and rental of furniture and home accessories in the People’s Republic of China.

Excellent balance sheet and slightly overvalued.

Market Insights

Community Narratives