Advertisement

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Tree Holdings Limited (HKG:8395) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Tree Holdings

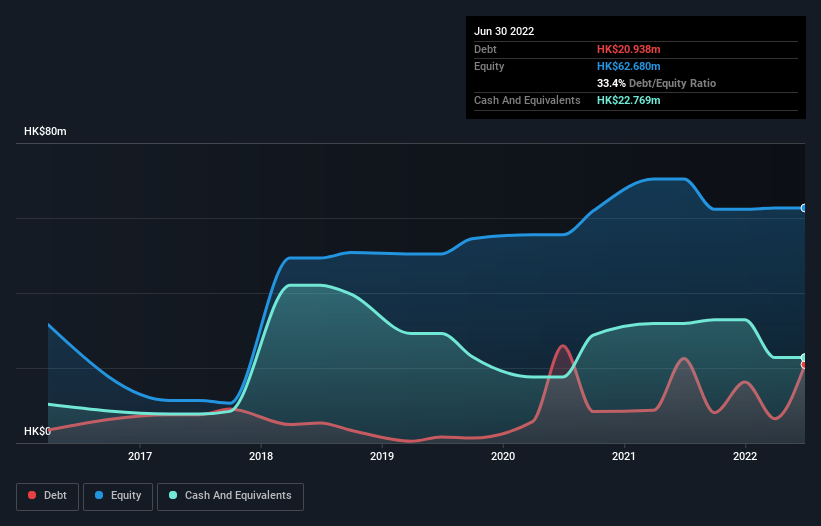

What Is Tree Holdings's Net Debt?

The image below, which you can click on for greater detail, shows that Tree Holdings had debt of HK$20.9m at the end of March 2022, a reduction from HK$22.6m over a year. However, its balance sheet shows it holds HK$22.8m in cash, so it actually has HK$1.83m net cash.

How Strong Is Tree Holdings' Balance Sheet?

We can see from the most recent balance sheet that Tree Holdings had liabilities of HK$46.7m falling due within a year, and liabilities of HK$5.54m due beyond that. Offsetting these obligations, it had cash of HK$22.8m as well as receivables valued at HK$33.7m due within 12 months. So it can boast HK$4.19m more liquid assets than total liabilities.

This state of affairs indicates that Tree Holdings' balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it's very unlikely that the HK$1.19b company is short on cash, but still worth keeping an eye on the balance sheet. Succinctly put, Tree Holdings boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Tree Holdings will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Tree Holdings had a loss before interest and tax, and actually shrunk its revenue by 31%, to HK$88m. That makes us nervous, to say the least.

So How Risky Is Tree Holdings?

Although Tree Holdings had an earnings before interest and tax (EBIT) loss over the last twelve months, it made a statutory profit of HK$419k. So when you consider it has net cash, along with the statutory profit, the stock probably isn't as risky as it might seem, at least in the short term. With mediocre revenue growth in the last year, we're don't find the investment opportunity particularly compelling. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. We've identified 3 warning signs with Tree Holdings , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if ZXZN Qi-House Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:8395

ZXZN Qi-House Holdings

Engages in the sale, distribution, and rental of furniture and home accessories in the People’s Republic of China.

Excellent balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor