Advertisement

- Hong Kong

- /

- Specialty Stores

- /

- SEHK:6883

Eternal Beauty Holdings (SEHK:6883) Margins Hit 12% High, Reinforcing Profit Quality Debate

Simply Wall St

Reviewed by Simply Wall St

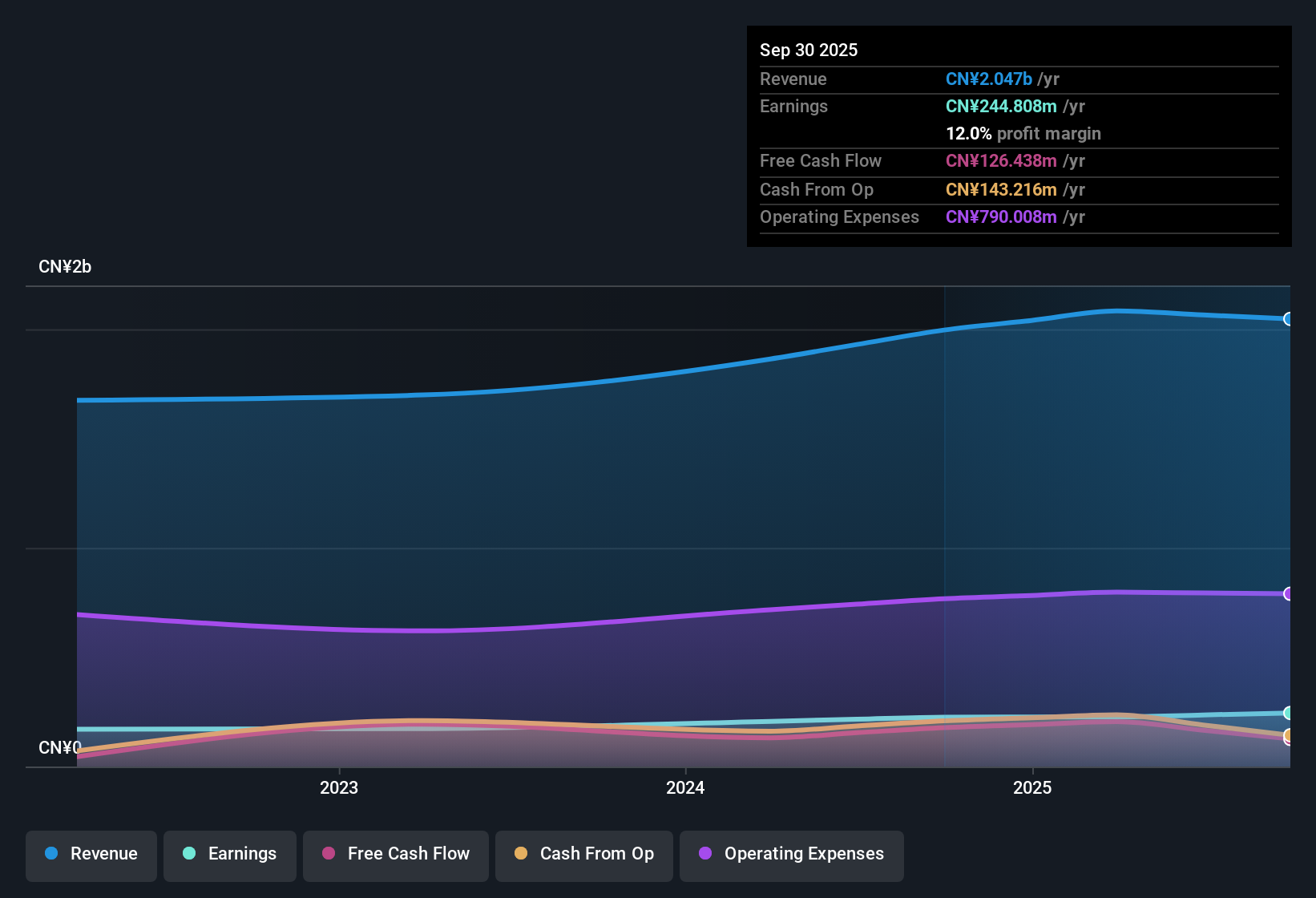

Eternal Beauty Holdings (SEHK:6883) has just posted its H1 2026 results, reporting revenue of 2.0 billion CNY and net income of 244.8 million CNY for the trailing twelve months. The company has seen revenue climb from 1.9 billion CNY in H1 2025 and 1.8 billion CNY in H1 2024, while net income moved up from 225.8 million CNY and 220.8 million CNY, respectively. Margins held firm and earnings momentum remains visible, leaving investors focused on whether underlying profitability is sustainable.

See our full analysis for Eternal Beauty Holdings.Next, we will see how these headline figures stack up against the dominant narratives and whether the results are challenging any consensus views.

Curious how numbers become stories that shape markets? Explore Community Narratives

Profit Margins Reach 12% High

- Net profit margin increased to 12% over the last twelve months, compared with 11.3% the previous year, highlighting improved underlying profitability even as revenue and net income continue trending higher.

- With this margin expansion, the general market narrative points to a stronger operating foundation, but also notes that the most recent annual earnings growth of 8.4% trails the five-year average of 10.6%. This suggests the company is performing well, yet may be experiencing a gradual moderation as it matures.

- The higher margin supports sustained profit delivery, but the slightly slower annual growth raises questions around how much more efficiency can be extracted going forward, especially if cost controls have already been maximized.

- This blend of positive fundamentals and flattening growth ties into the broader industry theme. The company shows strong performance versus peers, but not a breakaway outlier that defies sector trends.

- Sentiment remains cautiously optimistic as analysts forecast revenue growth of 15.1% annually, outpacing the Hong Kong market’s expected 8.5%, which could support continual margin strength if met or exceeded.

Shares Trade Well Below Fair Value

- The current share price at 2.19 CNY is 65.8% below the DCF fair value of 6.40, with a price-to-earnings ratio of 11x against the peer average of 24x and industry average of 11.5x.

- The prevailing opinion is that this valuation discount heavily supports the argument for value investors, given that the stock’s metrics, including low P/E, robust profit margin, and improving growth outlook, contrast with its depressed price.

- While the company is trading at a discount, the ongoing gap versus both peer valuations and intrinsic estimates could set up stronger upside if the market rerates the stock to closer to fair value.

- On the other hand, some interpret this gap as reflecting residual wariness about earnings durability, particularly given the less rapid growth in net income compared to the long-term trend and the high proportion of non-cash earnings.

Non-Cash Earnings Fuel Risk Debate

- A significant proportion of profits over the past year come from non-cash earnings, raising caution around the quality and sustainability of the reported profits despite strong margin and revenue performance.

- Many observers argue that this risk forces investors to look closer at the company’s underlying business fundamentals, not just headline profit figures, when assessing whether the current share price discount is deserved.

- This risk is especially relevant given that higher non-cash earnings can mask potential issues with underlying cash generation, which could affect liquidity or reinvestment capacity in the long run.

- Despite the clear uptrend in margins and a healthy revenue forecast, some caution that reliance on non-cash profits may pose a stumbling block to a sustained market re-rating until cash earnings strengthen.

- Find out how the mix of issue and opportunity shapes the big picture for Eternal Beauty Holdings. Read the full consensus view. 📊 Read the full Eternal Beauty Holdings Consensus Narrative.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Eternal Beauty Holdings's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Eternal Beauty Holdings’ heavy reliance on non-cash earnings, along with slowing net income growth, raises concerns about the sustainability of its profit quality.

If you want to minimize this kind of earnings risk, check out stable growth stocks screener (2074 results) to focus on companies with reliable, consistent growth driven by solid, repeatable profits.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Eternal Beauty Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:6883

Eternal Beauty Holdings

An investment holding company, engages in the retail, wholesale, and distribution of perfumes, skincare products, color cosmetics, personal care products, eyewear, and home fragrances in China, including Hong Kong and Macau.

Undervalued with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

139 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative