Stock Analysis

- Hong Kong

- /

- Specialty Stores

- /

- SEHK:3669

Returns On Capital - An Important Metric For China Yongda Automobiles Services Holdings (HKG:3669)

Finding a business that has the potential to grow substantially is not easy, but it is possible if we look at a few key financial metrics. Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. So when we looked at China Yongda Automobiles Services Holdings (HKG:3669) and its trend of ROCE, we really liked what we saw.

Return On Capital Employed (ROCE): What is it?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on China Yongda Automobiles Services Holdings is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.14 = CN¥2.4b ÷ (CN¥36b - CN¥18b) (Based on the trailing twelve months to June 2020).

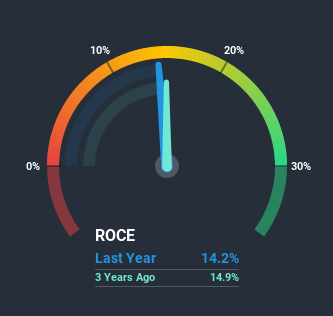

Thus, China Yongda Automobiles Services Holdings has an ROCE of 14%. In absolute terms, that's a satisfactory return, but compared to the Specialty Retail industry average of 11% it's much better.

See our latest analysis for China Yongda Automobiles Services Holdings

Above you can see how the current ROCE for China Yongda Automobiles Services Holdings compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering China Yongda Automobiles Services Holdings here for free.

What The Trend Of ROCE Can Tell Us

We like the trends that we're seeing from China Yongda Automobiles Services Holdings. Over the last five years, returns on capital employed have risen substantially to 14%. The amount of capital employed has increased too, by 142%. So we're very much inspired by what we're seeing at China Yongda Automobiles Services Holdings thanks to its ability to profitably reinvest capital.

On a side note, China Yongda Automobiles Services Holdings' current liabilities are still rather high at 52% of total assets. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.The Bottom Line

In summary, it's great to see that China Yongda Automobiles Services Holdings can compound returns by consistently reinvesting capital at increasing rates of return, because these are some of the key ingredients of those highly sought after multi-baggers. And with the stock having performed exceptionally well over the last five years, these patterns are being accounted for by investors. With that being said, we still think the promising fundamentals mean the company deserves some further due diligence.

On a final note, we've found 2 warning signs for China Yongda Automobiles Services Holdings that we think you should be aware of.

While China Yongda Automobiles Services Holdings isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

If you decide to trade China Yongda Automobiles Services Holdings, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're helping make it simple.

Find out whether China Yongda Automobiles Services Holdings is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:3669

China Yongda Automobiles Services Holdings

An investment holding company, operates as a passenger vehicle retailer and service provider for luxury and ultra-luxury brands in the People’s Republic of China.

Undervalued with excellent balance sheet and pays a dividend.