Advertisement

- Hong Kong

- /

- Specialty Stores

- /

- SEHK:1929

Chow Tai Fook (SEHK:1929) Net Margin Rises to 6.6%, Challenging Cautious Profitability Narratives

Simply Wall St

Reviewed by Simply Wall St

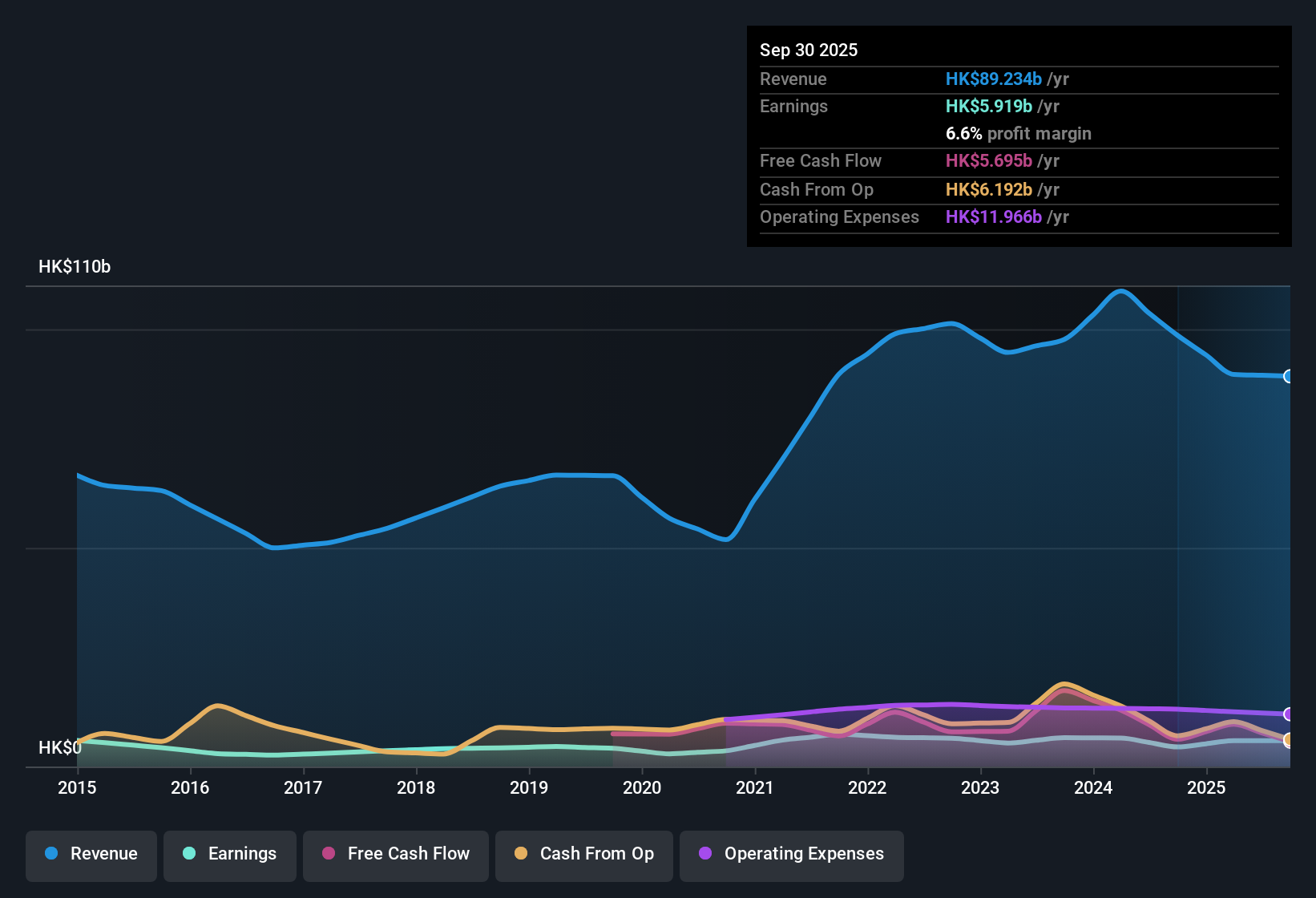

Chow Tai Fook Jewellery Group (SEHK:1929) just released its H1 2026 results, posting revenue of HK$39.0 billion and basic EPS of HK$0.26, with net income at HK$2.5 billion. Looking back, the company has seen revenue move from HK$39.4 billion in H1 2025 to HK$50.2 billion in H2 2025 before the latest tally. EPS shifted from HK$0.25 to HK$0.34 and then HK$0.26. Margins held up as investors focus on how recent profit improvements fit into the wider story.

See our full analysis for Chow Tai Fook Jewellery Group.Next, we break down how this set of numbers measures up against prevailing Simply Wall St narratives and where they might surprise.

See what the community is saying about Chow Tai Fook Jewellery Group

Net Margin Climbs to 6.6%

- Chow Tai Fook’s trailing twelve month net profit margin increased to 6.6%, up from last year's 4.5%, which may indicate stronger cost controls or a shift to higher-margin products.

- Consensus narrative highlights that this margin expansion strongly supports the investment case for improved profitability.

- Trailing twelve month earnings rose 32.2% year on year, in contrast to the five-year average annual decline of 0.4%.

- Analysts forecast profit margins to further expand to 10.1% within three years, expressing optimism for sustained bottom line growth even as revenue trends moderate.

Strength in margins could provide a sturdier base for earnings, challenging caution in the consensus view. Explore the full context in the consensus narrative link.

📊 Read the full Chow Tai Fook Jewellery Group Consensus Narrative. - The shares are trading at HK$14.31, representing a 30.1% discount compared to the DCF fair value of HK$20.48, which suggests possible price appreciation based on discounted cash flow analysis.

- Consensus narrative balances this with a note that, despite the significant discount to intrinsic value, Chow Tai Fook’s price-to-earnings ratio of 23.8x remains notably higher than industry and peer averages.

- This premium multiple indicates that the market is willing to pay for the company’s growth prospects, but it also limits upside if near-term growth does not meet expectations.

- Analyst price targets are closely grouped, with a consensus at HK$17.63, only 23% above current levels, which may temper enthusiasm about the perceived discount.

- Forward-looking revenue forecasts anticipate 4.7% annual growth for Chow Tai Fook, which is slower than the Hong Kong market’s 8.5% projection over the same period.

- Consensus narrative notes that, despite improvements in margins and earnings, slower revenue growth could affect the company’s ability to capture market share.

- Diversification efforts in international markets and e-commerce may eventually increase momentum, but current performance shows the business is still catching up to sector peers.

- Store count reductions and subdued sales in key regions, such as a 26% to 42% drop in retail sales value in Hong Kong and Macau, highlight the headwinds currently limiting growth.

DCF Valuation Shows 30% Discount

Revenue Growth Trails Local Market

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Chow Tai Fook Jewellery Group on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Notice something others might have missed? It only takes a few minutes to share your perspective and shape the story to fit your insights. Do it your way

A great starting point for your Chow Tai Fook Jewellery Group research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

See What Else Is Out There

Chow Tai Fook’s slower revenue growth and recent store reductions suggest it could struggle to keep pace with faster-growing sector peers in Hong Kong.

If you’re looking to prioritize consistent expansion, companies highlighted in our stable growth stocks screener (2073 results) may offer more reliable growth prospects for your watchlist.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1929

Chow Tai Fook Jewellery Group

An investment holding company, manufactures and sells jewelry products in Mainland China, Hong Kong, Macau, and internationally.

Solid track record with reasonable growth potential and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

75 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative