Advertisement

- Hong Kong

- /

- Specialty Stores

- /

- SEHK:1759

Sino Gas Holdings Group (HKG:1759) Takes On Some Risk With Its Use Of Debt

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Sino Gas Holdings Group Limited (HKG:1759) does carry debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Sino Gas Holdings Group

What Is Sino Gas Holdings Group's Net Debt?

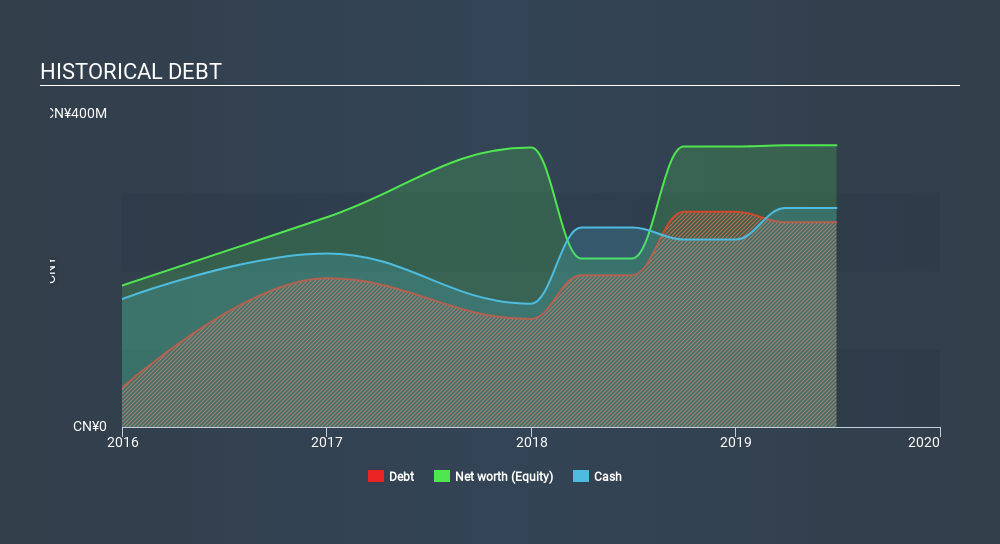

As you can see below, at the end of June 2019, Sino Gas Holdings Group had CN¥261.7m of debt, up from CN¥194.0m a year ago. Click the image for more detail. But on the other hand it also has CN¥279.8m in cash, leading to a CN¥18.1m net cash position.

A Look At Sino Gas Holdings Group's Liabilities

According to the balance sheet data, Sino Gas Holdings Group had liabilities of CN¥341.3m due within 12 months, but no longer term liabilities. Offsetting this, it had CN¥279.8m in cash and CN¥77.5m in receivables that were due within 12 months. So it actually has CN¥15.9m more liquid assets than total liabilities.

This surplus suggests that Sino Gas Holdings Group has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that Sino Gas Holdings Group has more cash than debt is arguably a good indication that it can manage its debt safely.

Importantly, Sino Gas Holdings Group's EBIT fell a jaw-dropping 58% in the last twelve months. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Sino Gas Holdings Group will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Sino Gas Holdings Group may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. In the last three years, Sino Gas Holdings Group's free cash flow amounted to 25% of its EBIT, less than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that Sino Gas Holdings Group has net cash of CN¥18.1m, as well as more liquid assets than liabilities. So while Sino Gas Holdings Group does not have a great balance sheet, it's certainly not too bad. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 6 warning signs for Sino Gas Holdings Group (3 are a bit concerning) you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About SEHK:1759

Sino Gas Holdings Group

Engages in the retail and wholesale of liquefied petroleum gas (LPG), compressed natural gas (CNG), and liquefied natural gas (LNG) in the People’s Republic of China.

Slight with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor