- Hong Kong

- /

- Capital Markets

- /

- SEHK:1468

We Take A Look At Whether Kingkey Financial International (Holdings) Limited's (HKG:1468) CEO May Be Underpaid

The solid performance at Kingkey Financial International (Holdings) Limited (HKG:1468) has been impressive and shareholders will probably be pleased to know that CEO Yin Ning Kwok has delivered. This would be kept in mind at the upcoming AGM on 08 February 2022 which will be a chance for them to hear the board review the financial results, discuss future company strategy and vote on resolutions such as executive remuneration and other matters. We think the CEO has done a pretty decent job and probably deserves a well-earned pay rise.

See our latest analysis for Kingkey Financial International (Holdings)

Comparing Kingkey Financial International (Holdings) Limited's CEO Compensation With the industry

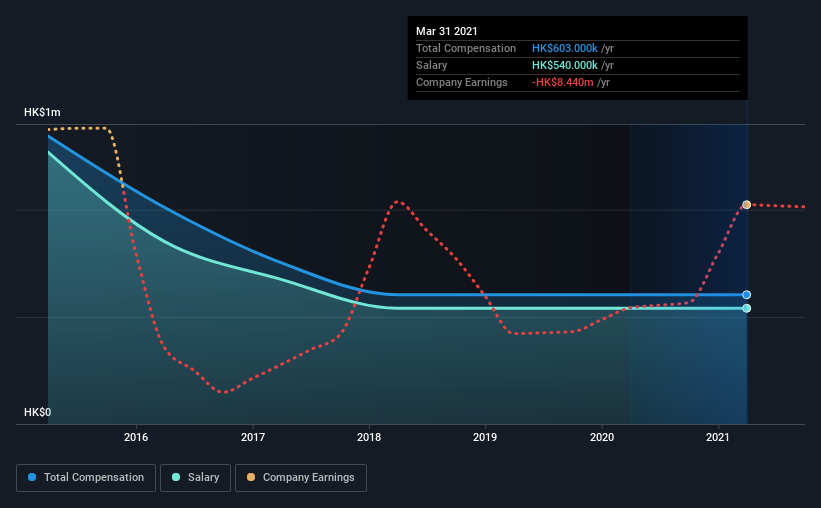

At the time of writing, our data shows that Kingkey Financial International (Holdings) Limited has a market capitalization of HK$4.2b, and reported total annual CEO compensation of HK$603k for the year to March 2021. There was no change in the compensation compared to last year. We note that the salary portion, which stands at HK$540.0k constitutes the majority of total compensation received by the CEO.

On comparing similar companies from the same industry with market caps ranging from HK$1.6b to HK$6.2b, we found that the median CEO total compensation was HK$5.0m. This suggests that Yin Ning Kwok is paid below the industry median. What's more, Yin Ning Kwok holds HK$9.8m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | HK$540k | HK$540k | 90% |

| Other | HK$63k | HK$63k | 10% |

| Total Compensation | HK$603k | HK$603k | 100% |

Speaking on an industry level, nearly 92% of total compensation represents salary, while the remainder of 8% is other remuneration. Although there is a difference in how total compensation is set, Kingkey Financial International (Holdings) more or less reflects the market in terms of setting the salary. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Kingkey Financial International (Holdings) Limited's Growth

Kingkey Financial International (Holdings) Limited has seen its earnings per share (EPS) increase by 40% a year over the past three years. In the last year, its revenue is down 7.0%.

Shareholders would be glad to know that the company has improved itself over the last few years. It's always a tough situation when revenues are not growing, but ultimately profits are more important. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Kingkey Financial International (Holdings) Limited Been A Good Investment?

We think that the total shareholder return of 170%, over three years, would leave most Kingkey Financial International (Holdings) Limited shareholders smiling. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

In Summary...

Given the improved performance, shareholders may be more forgiving of CEO compensation in the upcoming AGM. In saying that, some shareholders may feel that the more important issues to be addressed may be how the management plans to steer the company towards sustainable profitability in the future.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. We identified 3 warning signs for Kingkey Financial International (Holdings) (1 can't be ignored!) that you should be aware of before investing here.

Important note: Kingkey Financial International (Holdings) is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Kingkey Financial International (Holdings) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1468

Kingkey Financial International (Holdings)

An investment holding company, provides insurance brokerage services in the People’s Republic of China, Hong Kong, and Denmark.

Excellent balance sheet moderate.

Market Insights

Community Narratives