Advertisement

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that China Merchants Land Limited (HKG:978) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for China Merchants Land

How Much Debt Does China Merchants Land Carry?

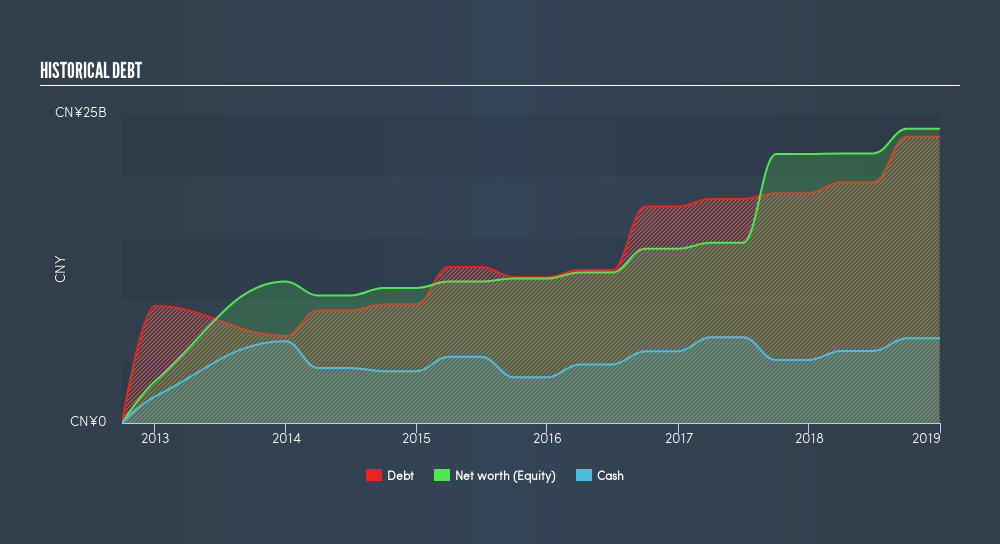

The image below, which you can click on for greater detail, shows that at December 2018 China Merchants Land had debt of CN¥23.2b, up from CN¥18.6b in one year. However, because it has a cash reserve of CN¥6.87b, its net debt is less, at about CN¥16.3b.

A Look At China Merchants Land's Liabilities

We can see from the most recent balance sheet that China Merchants Land had liabilities of CN¥34.4b falling due within a year, and liabilities of CN¥13.0b due beyond that. Offsetting these obligations, it had cash of CN¥6.87b as well as receivables valued at CN¥7.74b due within 12 months. So it has liabilities totalling CN¥32.9b more than its cash and near-term receivables, combined.

This deficit casts a shadow over the CN¥4.96b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, China Merchants Land would probably need a major re-capitalization if its creditors were to demand repayment. Since China Merchants Land does have net debt, we think it is worthwhile for shareholders to keep an eye on the balance sheet, over time.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

China Merchants Land's net debt is 4.60 times its EBITDA, which is a significant but still reasonable amount of leverage. However, its interest coverage of 13.4 is very high, suggesting that the interest expense may well rise in the future, even if there hasn't yet been a major cost attached to that debt. Shareholders should be aware that China Merchants Land's EBIT was down 34% last year. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since China Merchants Land will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. In the last three years, China Merchants Land created free cash flow amounting to 19% of its EBIT, an uninspiring performance. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

To be frank both China Merchants Land's EBIT growth rate and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. But on the bright side, its interest cover is a good sign, and makes us more optimistic. After considering the datapoints discussed, we think China Merchants Land has too much debt. While some investors love that sort of risky play, it's certainly not our cup of tea. Another positive for shareholders is that it pays dividends. So if you like receiving those dividend payments, check China Merchants Land's dividend history, without delay!

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About SEHK:978

China Merchants Land

An investment holding company, engages in the development, management, lease, investment, and sale of properties.

Good value with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.6% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor