Advertisement

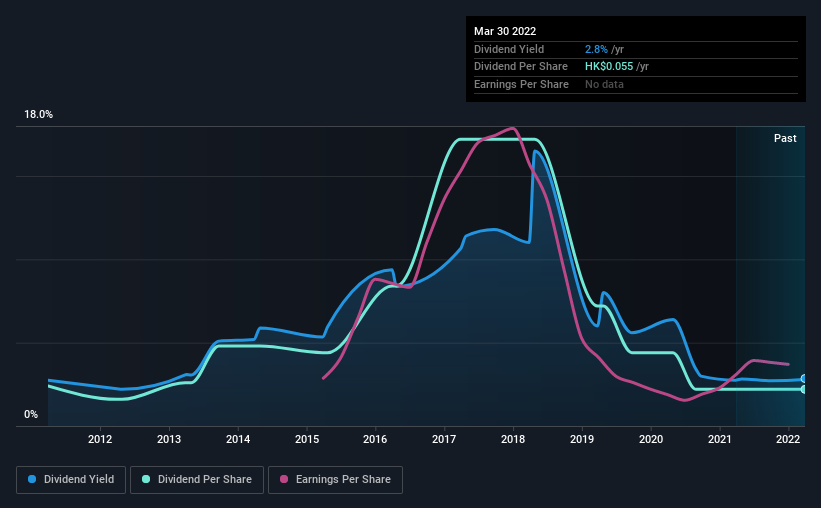

The board of Tomson Group Limited (HKG:258) has announced that it will pay a dividend on the 22nd of June, with investors receiving HK$0.055 per share. This payment means the dividend yield will be 2.8%, which is below the average for the industry.

Check out our latest analysis for Tomson Group

Tomson Group's Dividend Is Well Covered By Earnings

If it is predictable over a long period, even low dividend yields can be attractive. However, based ont he last payment, Tomson Group was earning enough to cover the dividend pretty comfortably. The business is returning a large chunk of its cash to shareholders, which means it is not being used to grow the business.

Looking forward, EPS could fall by 22.9% if the company can't turn things around from the last few years. Assuming the dividend continues along recent trends, we believe the payout ratio could be 38%, which we are pretty comfortable with and we think is feasible on an earnings basis.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. Since 2012, the dividend has gone from HK$0.06 to HK$0.055. Dividend payments have shrunk at a rate of less than 1% per annum over this time frame. Generally, we don't like to see a dividend that has been declining over time as this can degrade shareholders' returns and indicate that the company may be running into problems.

Dividend Growth Potential Is Shaky

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. Tomson Group's EPS has fallen by approximately 23% per year during the past five years. Dividend payments are likely to come under some pressure unless EPS can pull out of the nosedive it is in.

In Summary

Overall, it's nice to see a consistent dividend payment, but we think that longer term, the current level of payment might be unsustainable. While Tomson Group is earning enough to cover the dividend, we are generally unimpressed with its future prospects. We would be a touch cautious of relying on this stock primarily for the dividend income.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. For example, we've identified 2 warning signs for Tomson Group (1 is a bit unpleasant!) that you should be aware of before investing. Is Tomson Group not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Tomson Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:258

Tomson Group

An investment holding company, engages in the property development and investment, hospitality and leisure, securities trading, and media and entertainment investment and operation businesses in Hong Kong, Macau, and Mainland China.

Proven track record with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|49.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|7.0% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|20.3% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|54.2% overvalued

RO

Community Contributor