Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:202

Shareholders May Not Be So Generous With EverChina Int'l Holdings Company Limited's (HKG:202) CEO Compensation And Here's Why

Performance at EverChina Int'l Holdings Company Limited (HKG:202) has been reasonably good and CEO Richard Lam has done a decent job of steering the company in the right direction. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 03 September 2021. However, some shareholders may still want to keep CEO compensation within reason.

Check out our latest analysis for EverChina Int'l Holdings

How Does Total Compensation For Richard Lam Compare With Other Companies In The Industry?

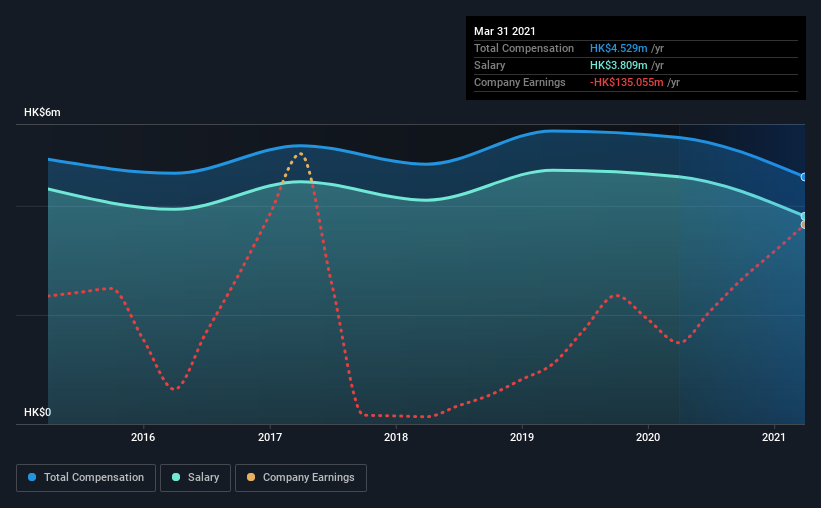

At the time of writing, our data shows that EverChina Int'l Holdings Company Limited has a market capitalization of HK$1.3b, and reported total annual CEO compensation of HK$4.5m for the year to March 2021. That's a notable decrease of 14% on last year. In particular, the salary of HK$3.81m, makes up a huge portion of the total compensation being paid to the CEO.

In comparison with other companies in the industry with market capitalizations ranging from HK$779m to HK$3.1b, the reported median CEO total compensation was HK$2.8m. This suggests that Richard Lam is paid more than the median for the industry. Furthermore, Richard Lam directly owns HK$1.4m worth of shares in the company.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | HK$3.8m | HK$4.5m | 84% |

| Other | HK$720k | HK$720k | 16% |

| Total Compensation | HK$4.5m | HK$5.3m | 100% |

Talking in terms of the industry, salary represented approximately 70% of total compensation out of all the companies we analyzed, while other remuneration made up 30% of the pie. According to our research, EverChina Int'l Holdings has allocated a higher percentage of pay to salary in comparison to the wider industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at EverChina Int'l Holdings Company Limited's Growth Numbers

EverChina Int'l Holdings Company Limited's earnings per share (EPS) grew 47% per year over the last three years. Its revenue is down 7.4% over the previous year.

This demonstrates that the company has been improving recently and is good news for the shareholders. The lack of revenue growth isn't ideal, but it is the bottom line that counts most in business. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has EverChina Int'l Holdings Company Limited Been A Good Investment?

EverChina Int'l Holdings Company Limited has generated a total shareholder return of 12% over three years, so most shareholders would be reasonably content. But they probably don't want to see the CEO paid more than is normal for companies around the same size.

To Conclude...

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. However, any decision to raise CEO pay might be met with some objections from the shareholders given that the CEO is already paid higher than the industry average.

CEO compensation is one thing, but it is also interesting to check if the CEO is buying or selling EverChina Int'l Holdings (free visualization of insider trades).

Important note: EverChina Int'l Holdings is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if EverChina Int'l Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:202

EverChina Int'l Holdings

An investment holding company, primarily engages in the property investment and hotel operations in the People’s Republic of China and Bolivia.

Excellent balance sheet with minimal risk.

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|29.0% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.6% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|60.1% undervalued

ME

Community Contributor