Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:1528

Red Star Macalline Group (HKG:1528) Use Of Debt Could Be Considered Risky

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Red Star Macalline Group Corporation Ltd. (HKG:1528) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Red Star Macalline Group

How Much Debt Does Red Star Macalline Group Carry?

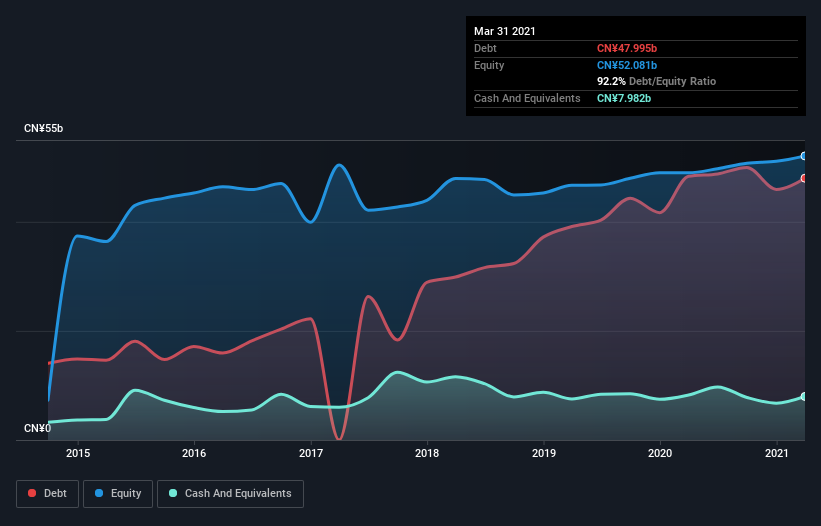

The chart below, which you can click on for greater detail, shows that Red Star Macalline Group had CN¥47.1b in debt in March 2021; about the same as the year before. However, because it has a cash reserve of CN¥7.98b, its net debt is less, at about CN¥39.1b.

How Healthy Is Red Star Macalline Group's Balance Sheet?

We can see from the most recent balance sheet that Red Star Macalline Group had liabilities of CN¥33.1b falling due within a year, and liabilities of CN¥49.8b due beyond that. Offsetting these obligations, it had cash of CN¥7.98b as well as receivables valued at CN¥5.11b due within 12 months. So its liabilities total CN¥69.9b more than the combination of its cash and short-term receivables.

When you consider that this deficiency exceeds the company's CN¥47.3b market capitalization, you might well be inclined to review the balance sheet intently. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Weak interest cover of 2.4 times and a disturbingly high net debt to EBITDA ratio of 7.8 hit our confidence in Red Star Macalline Group like a one-two punch to the gut. The debt burden here is substantial. Another concern for investors might be that Red Star Macalline Group's EBIT fell 10% in the last year. If that's the way things keep going handling the debt load will be like delivering hot coffees on a pogo stick. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Red Star Macalline Group can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Considering the last three years, Red Star Macalline Group actually recorded a cash outflow, overall. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Our View

To be frank both Red Star Macalline Group's conversion of EBIT to free cash flow and its track record of managing its debt, based on its EBITDA, make us rather uncomfortable with its debt levels. And furthermore, its interest cover also fails to instill confidence. Considering all the factors previously mentioned, we think that Red Star Macalline Group really is carrying too much debt. To us, that makes the stock rather risky, like walking through a dog park with your eyes closed. But some investors may feel differently. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 3 warning signs for Red Star Macalline Group (1 doesn't sit too well with us!) that you should be aware of before investing here.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1528

Moderate growth potential and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.8% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|22.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.8% overvalued

LI

Community Contributor