Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:816

Downgrade: Here's How Analysts See Jinmao Property Services Co., Limited (HKG:816) Performing In The Near Term

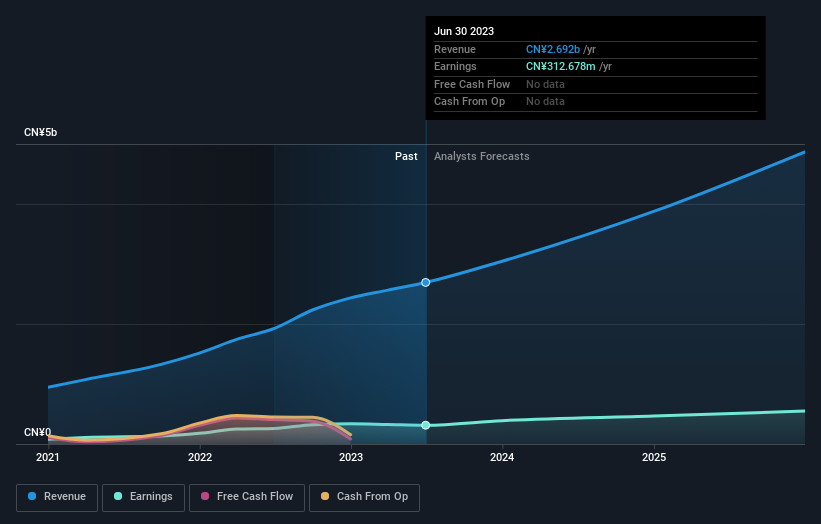

The analysts covering Jinmao Property Services Co., Limited (HKG:816) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for this year. Revenue and earnings per share (EPS) forecasts were both revised downwards, with analysts seeing grey clouds on the horizon.

Following the downgrade, the most recent consensus for Jinmao Property Services from its three analysts is for revenues of CN¥3.0b in 2023 which, if met, would be a solid 13% increase on its sales over the past 12 months. Statutory earnings per share are presumed to expand 17% to CN¥0.41. Prior to this update, the analysts had been forecasting revenues of CN¥3.5b and earnings per share (EPS) of CN¥0.49 in 2023. It looks like analyst sentiment has declined substantially, with a substantial drop in revenue estimates and a considerable drop in earnings per share numbers as well.

View our latest analysis for Jinmao Property Services

The consensus price target fell 53% to CN¥2.51, with the weaker earnings outlook clearly leading analyst valuation estimates. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values Jinmao Property Services at CN¥2.97 per share, while the most bearish prices it at CN¥2.04. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. It's pretty clear that there is an expectation that Jinmao Property Services' revenue growth will slow down substantially, with revenues to the end of 2023 expected to display 13% growth on an annualised basis. This is compared to a historical growth rate of 40% over the past year. Compare this to the 276 other companies in this industry with analyst coverage, which are forecast to grow their revenue at 11% per year. So it's pretty clear that, while Jinmao Property Services' revenue growth is expected to slow, it's expected to grow roughly in line with the industry.

The Bottom Line

The biggest issue in the new estimates is that analysts have reduced their earnings per share estimates, suggesting business headwinds lay ahead for Jinmao Property Services. Lamentably, they also downgraded their sales forecasts, but the business is still expected to grow at roughly the same rate as the market itself. After such a stark change in sentiment from analysts, we'd understand if readers now felt a bit wary of Jinmao Property Services.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Jinmao Property Services analysts - going out to 2025, and you can see them free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:816

Jinmao Property Services

An investment holding company, provides property management services in the People’s Republic of China.

Flawless balance sheet, undervalued and pays a dividend.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor