Advertisement

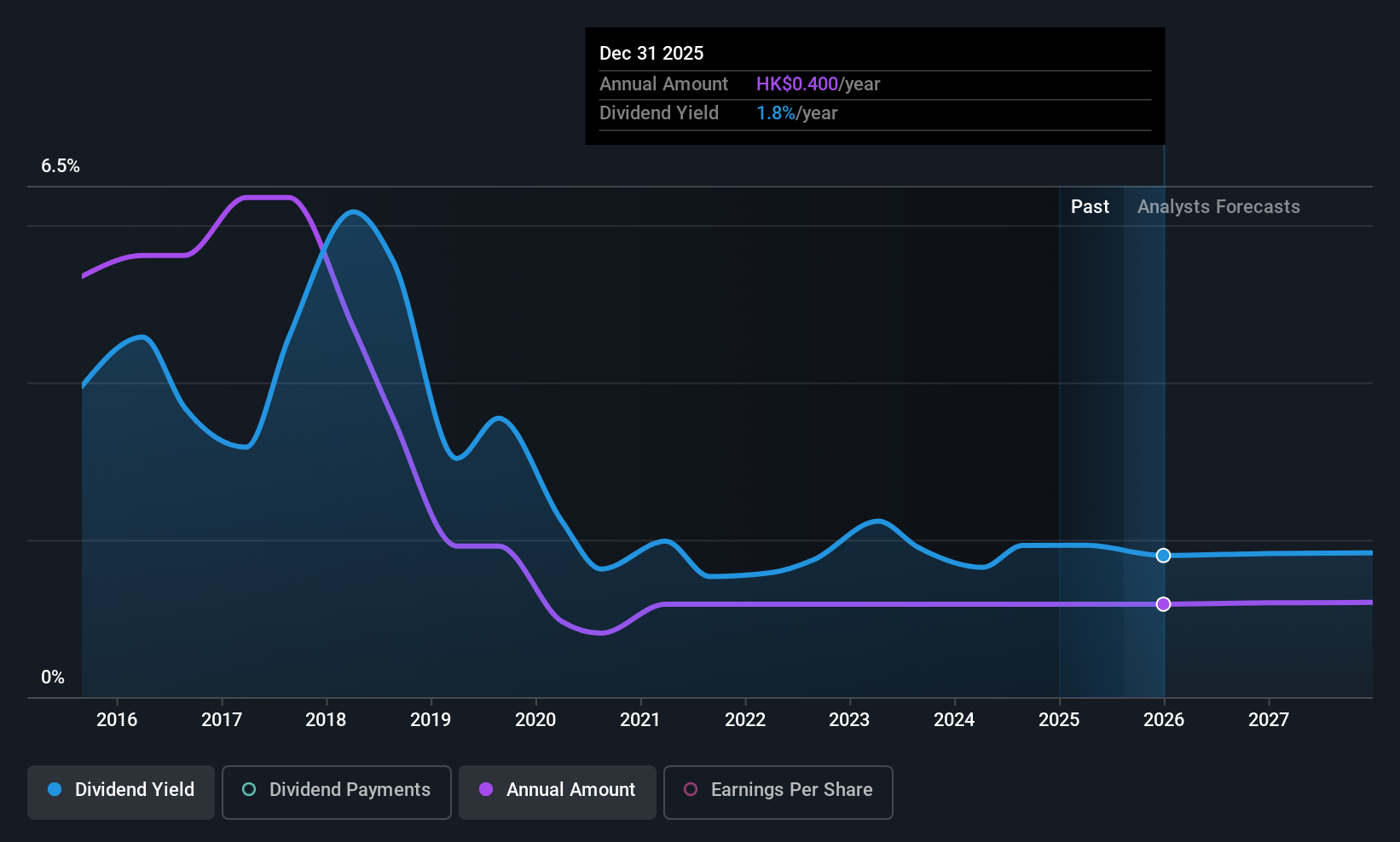

The board of The Wharf (Holdings) Limited (HKG:4) has announced that it will pay a dividend on the 16th of September, with investors receiving HK$0.20 per share. Including this payment, the dividend yield on the stock will be 1.8%, which is a modest boost for shareholders' returns.

Wharf (Holdings)'s Projections Indicate Future Payments May Be Unsustainable

Estimates Indicate Wharf (Holdings)'s Could Struggle to Maintain Dividend Payments In The Future

Wharf (Holdings)'s Future Dividends May Potentially Be At Risk

If it is predictable over a long period, even low dividend yields can be attractive. Even though Wharf (Holdings) isn't generating a profit, it is generating healthy free cash flows that easily cover the dividend. We generally think that cash flow is more important than accounting measures of profit, so we are fairly comfortable with the dividend at this level.

Over the next year, EPS is forecast to grow rapidly. Assuming the dividend continues along recent trends, we could see the payout ratio reach 893%, which is on the unsustainable side.

View our latest analysis for Wharf (Holdings)

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. Since 2015, the dividend has gone from HK$1.81 total annually to HK$0.40. This works out to a decline of approximately 78% over that time. Declining dividends isn't generally what we look for as they can indicate that the company is running into some challenges.

The Dividend Has Limited Growth Potential

Given that the track record hasn't been stellar, we really want to see earnings per share growing over time. Wharf (Holdings)'s earnings per share has shrunk at 51% a year over the past five years. Such rapid declines definitely have the potential to constrain dividend payments if the trend continues into the future. Over the next year, however, earnings are actually predicted to rise, but we would still be cautious until a track record of earnings growth can be built.

The Dividend Could Prove To Be Unreliable

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about Wharf (Holdings)'s payments, as there could be some issues with sustaining them into the future. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. We don't think Wharf (Holdings) is a great stock to add to your portfolio if income is your focus.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. However, there are other things to consider for investors when analysing stock performance. Without at least some growth in earnings per share over time, the dividend will eventually come under pressure either from competition or inflation. See if the 6 analysts are forecasting a turnaround in our free collection of analyst estimates here. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Wharf (Holdings) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:4

Wharf (Holdings)

Founded in 1886, The Wharf (Holdings) Limited (“Wharf”, Stock Code: 4) was the 17th company registered in Hong Kong and is currently the 7th with the longest history.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|7.3% undervalued

AN

Based on Analyst Price Targets