Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:3319

A-Living Smart City Services Co., Ltd.'s (HKG:3319) Share Price Boosted 34% But Its Business Prospects Need A Lift Too

A-Living Smart City Services Co., Ltd. (HKG:3319) shareholders would be excited to see that the share price has had a great month, posting a 34% gain and recovering from prior weakness. But the last month did very little to improve the 53% share price decline over the last year.

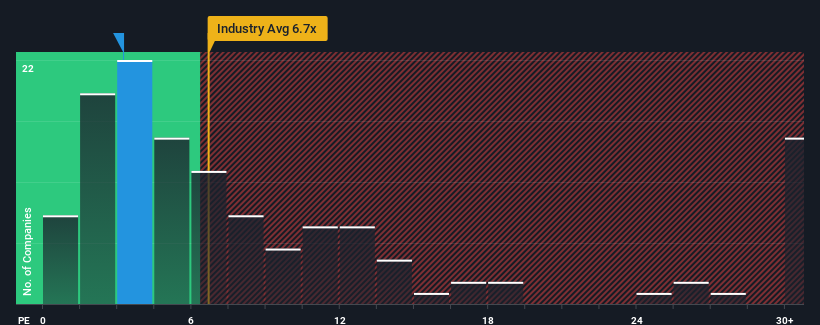

In spite of the firm bounce in price, A-Living Smart City Services may still be sending very bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 3.2x, since almost half of all companies in Hong Kong have P/E ratios greater than 9x and even P/E's higher than 19x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

Recent times haven't been advantageous for A-Living Smart City Services as its earnings have been falling quicker than most other companies. It seems that many are expecting the dismal earnings performance to persist, which has repressed the P/E. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. Or at the very least, you'd be hoping the earnings slide doesn't get any worse if your plan is to pick up some stock while it's out of favour.

Check out our latest analysis for A-Living Smart City Services

What Are Growth Metrics Telling Us About The Low P/E?

In order to justify its P/E ratio, A-Living Smart City Services would need to produce anemic growth that's substantially trailing the market.

Retrospectively, the last year delivered a frustrating 27% decrease to the company's bottom line. This has soured the latest three-year period, which nevertheless managed to deliver a decent 5.1% overall rise in EPS. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of earnings growth.

Turning to the outlook, the next three years should generate growth of 4.6% per annum as estimated by the eleven analysts watching the company. That's shaping up to be materially lower than the 16% each year growth forecast for the broader market.

With this information, we can see why A-Living Smart City Services is trading at a P/E lower than the market. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

What We Can Learn From A-Living Smart City Services' P/E?

A-Living Smart City Services' recent share price jump still sees its P/E sitting firmly flat on the ground. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of A-Living Smart City Services' analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

Before you settle on your opinion, we've discovered 1 warning sign for A-Living Smart City Services that you should be aware of.

You might be able to find a better investment than A-Living Smart City Services. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:3319

A-Living Smart City Services

Provides property management, sale, and inspection services in the People’s Republic of China.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|27.6% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.1% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|60.0% undervalued

ME

Community Contributor