Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:237

Safety Godown (SEHK:237): Net Loss Deepens to HK$-283M, Undermining Turnaround Narratives

Simply Wall St

Reviewed by Simply Wall St

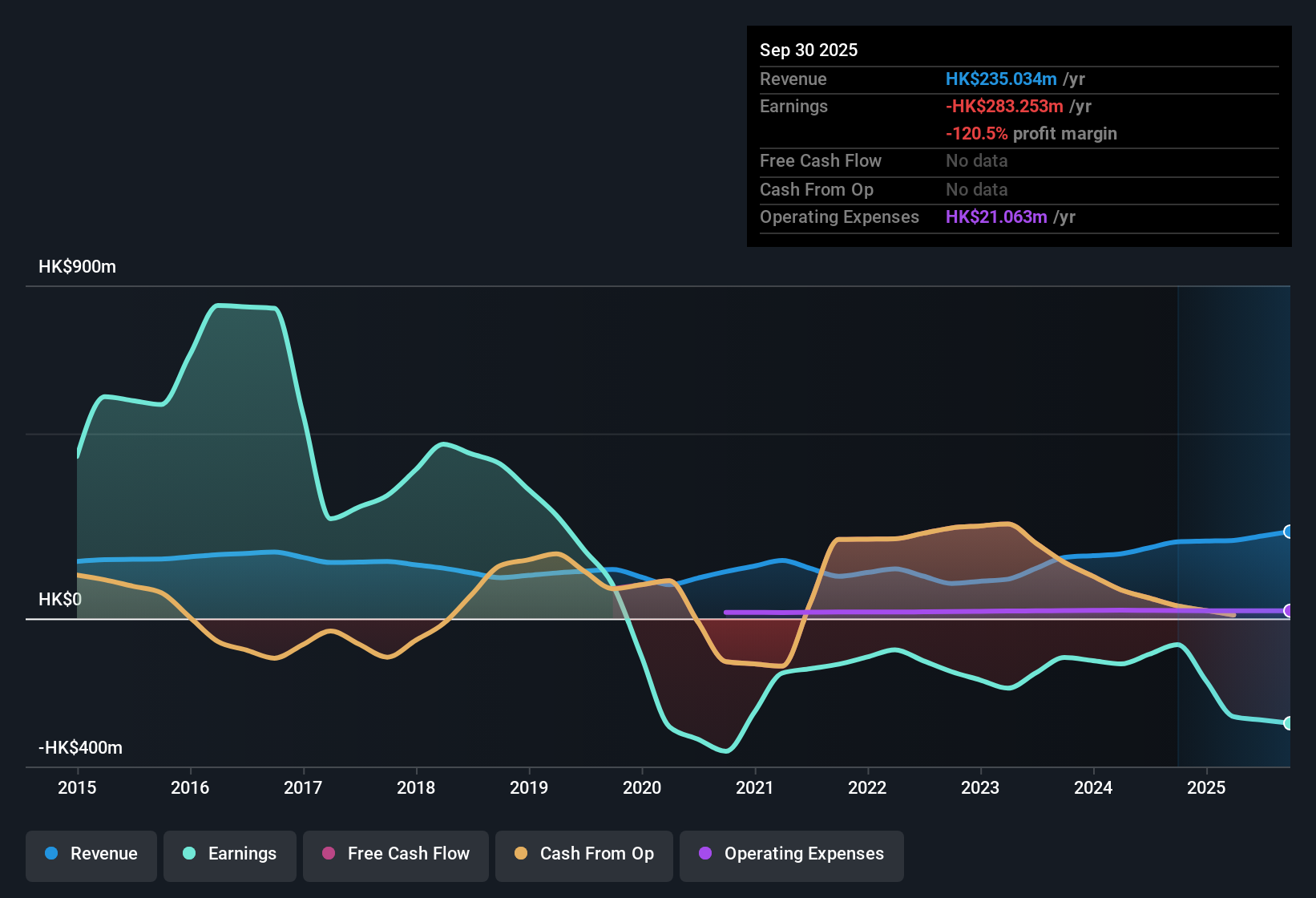

Safety Godown Company (SEHK:237) reported H1 2026 results showing total revenue of HK$235.0 million and a basic EPS of -0.67 HKD. Over the past several periods, revenue moved from HK$207.1 million in H1 2025 to HK$211.2 million in H2 2025, and now to HK$235.0 million in the trailing twelve months. EPS tracked a similar trend, shifting from -0.17 HKD to -0.66 HKD over the same periods. Margin pressures remain clear across headline metrics, putting renewed focus on profitability and future guidance from management.

See our full analysis for Safety Godown Company.Next, we compare these headline numbers to the prevailing narratives in the market to see which stories hold up and which may need rethinking.

Curious how numbers become stories that shape markets? Explore Community Narratives

Losses Deepen as Net Profit Margin Fails to Recover

- Net income excluding extra items reached a loss of HK$-283.3 million over the last twelve months, with no improvement in profit margin compared to prior periods.

- Bears emphasize that persistent net losses and a lack of earnings quality directly contradict hopes of a turnaround. The data shows net losses growing with each recent period:

- Trailing 12-month loss expanded from HK$-70.7 million (H1 2025) to HK$-283.3 million (H1 2026), showing a deepening negative trend and no visible margin recovery.

- Despite the company’s real asset base, bulls’ arguments for stability and value are undermined by unbroken profitability challenges over multiple reporting periods.

Premium Valuation Despite Sector Lag

- Safety Godown trades on a Price-to-Sales ratio of 3.6x, well above the Hong Kong real estate industry average of 0.7x and the peer average of 1.8x.

- Critics highlight that this elevated multiple exposes investors to valuation risk without reward. The HK$2.07 share price stands far above the DCF fair value of HK$0.42:

- The ongoing trading premium is not justified by performance, as neither revenue growth nor profit margin outpaces sector averages.

- Bearish arguments gain traction as valuation disconnects from fundamentals, raising red flags for new buyers reviewing the latest report.

Dividend Yield Threatened by Uncovered Payouts

- The current dividend yield is 3.86%, but recent financials confirm it is not covered by either reported earnings (net loss HK$-283.3 million) or free cash flow.

- What is surprising is how dividend sustainability questions have shifted the market focus away from income appeal. The narrative now revolves around payout risk:

- With losses mounting and coverage ratios deteriorating, the reward profile weakens for income-focused shareholders who previously relied on stable distributions.

- Consensus narrative notes the market increasingly views dividend risk as a key obstacle, significantly curbing the company’s defensive reputation.

If you want to see how other investors balance the risks and rewards, dive deeper in the consensus breakdown. 📊 Read the full Safety Godown Company Consensus Narrative.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Safety Godown Company's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Safety Godown’s persistent net losses, uncovered dividends, and hefty valuation premium highlight mounting risks for both income and value-focused investors.

Looking for attractively priced alternatives with stronger fundamentals and better downside protection? Discover potential bargains now by checking out these 922 undervalued stocks based on cash flows and target companies where market price and business strength are better aligned.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:237

Safety Godown Company

An investment holding company, engages in the operation of godowns in Hong Kong.

Flawless balance sheet with very low risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative