Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:1966

Some Analysts Just Cut Their China SCE Group Holdings Limited (HKG:1966) Estimates

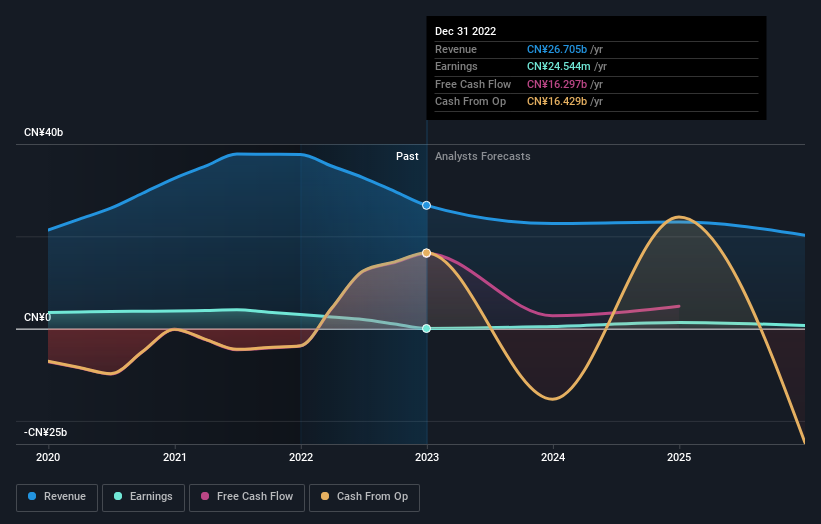

The latest analyst coverage could presage a bad day for China SCE Group Holdings Limited (HKG:1966), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. There was a fairly draconian cut to their revenue estimates, perhaps an implicit admission that previous forecasts were much too optimistic.

Following the latest downgrade, the four analysts covering China SCE Group Holdings provided consensus estimates of CN¥23b revenue in 2023, which would reflect a definite 15% decline on its sales over the past 12 months. Prior to the latest estimates, the analysts were forecasting revenues of CN¥28b in 2023. It looks like forecasts have become a fair bit less optimistic on China SCE Group Holdings, given the measurable cut to revenue estimates.

See our latest analysis for China SCE Group Holdings

Notably, the analysts have cut their price target 18% to CN¥0.65, suggesting concerns around China SCE Group Holdings' valuation. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on China SCE Group Holdings, with the most bullish analyst valuing it at CN¥1.00 and the most bearish at CN¥0.28 per share. As you can see the range of estimates is wide, with the lowest valuation coming in at less than half the most bullish estimate, suggesting there are some strongly diverging views on how think this business will perform. As a result it might not be possible to derive much meaning from the consensus price target, which is after all just an average of this wide range of estimates.

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would highlight that sales are expected to reverse, with a forecast 15% annualised revenue decline to the end of 2023. That is a notable change from historical growth of 17% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 8.9% annually for the foreseeable future. It's pretty clear that China SCE Group Holdings' revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to take away is that analysts cut their revenue estimates for this year. They also expect company revenue to perform worse than the wider market. The consensus price target fell measurably, with analysts seemingly not reassured by recent business developments, leading to a lower estimate of China SCE Group Holdings' future valuation. Often, one downgrade can set off a daisy-chain of cuts, especially if an industry is in decline. So we wouldn't be surprised if the market became a lot more cautious on China SCE Group Holdings after today.

After a downgrade like this, it's pretty clear that previous forecasts were too optimistic. What's more, we've spotted several possible issues with China SCE Group Holdings' business, like its declining profit margins. Learn more, and discover the 2 other warning signs we've identified, for free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1966

China SCE Group Holdings

An investment holding company, engages in the development, investment, and management of properties in the People’s Republic of China.

Low risk and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor