Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:1755

The Market Doesn't Like What It Sees From S-Enjoy Service Group Co., Limited's (HKG:1755) Earnings Yet As Shares Tumble 27%

To the annoyance of some shareholders, S-Enjoy Service Group Co., Limited (HKG:1755) shares are down a considerable 27% in the last month, which continues a horrid run for the company. For any long-term shareholders, the last month ends a year to forget by locking in a 68% share price decline.

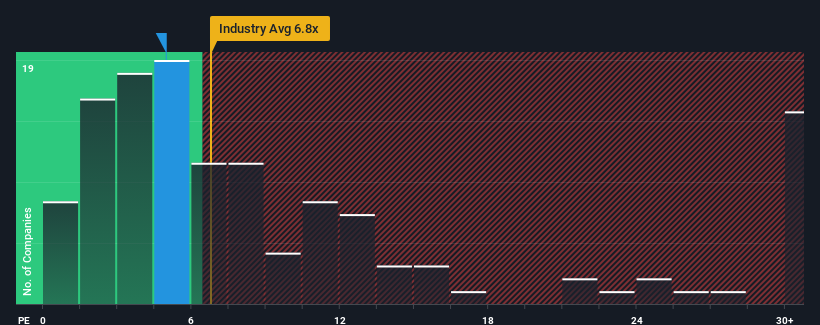

Although its price has dipped substantially, given about half the companies in Hong Kong have price-to-earnings ratios (or "P/E's") above 9x, you may still consider S-Enjoy Service Group as an attractive investment with its 5x P/E ratio. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

S-Enjoy Service Group certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. It might be that many expect the strong earnings performance to degrade substantially, possibly more than the market, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

See our latest analysis for S-Enjoy Service Group

Does Growth Match The Low P/E?

The only time you'd be truly comfortable seeing a P/E as low as S-Enjoy Service Group's is when the company's growth is on track to lag the market.

Retrospectively, the last year delivered a decent 5.8% gain to the company's bottom line. Pleasingly, EPS has also lifted 30% in aggregate from three years ago, partly thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Shifting to the future, estimates from the nine analysts covering the company suggest earnings should grow by 11% per annum over the next three years. With the market predicted to deliver 15% growth per year, the company is positioned for a weaker earnings result.

With this information, we can see why S-Enjoy Service Group is trading at a P/E lower than the market. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Bottom Line On S-Enjoy Service Group's P/E

S-Enjoy Service Group's recently weak share price has pulled its P/E below most other companies. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that S-Enjoy Service Group maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Before you take the next step, you should know about the 2 warning signs for S-Enjoy Service Group (1 can't be ignored!) that we have uncovered.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1755

S-Enjoy Service Group

An investment holding company, provides property management and related value-added services for property developers in the People’s Republic of China.

Flawless balance sheet and undervalued.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.8% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.5% undervalued

GM

Community Contributor