Advertisement

These 4 Measures Indicate That CK Life Sciences Int'l. (Holdings) (HKG:775) Is Using Debt Extensively

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that CK Life Sciences Int'l., (Holdings) Inc. (HKG:775) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for CK Life Sciences Int'l. (Holdings)

What Is CK Life Sciences Int'l. (Holdings)'s Debt?

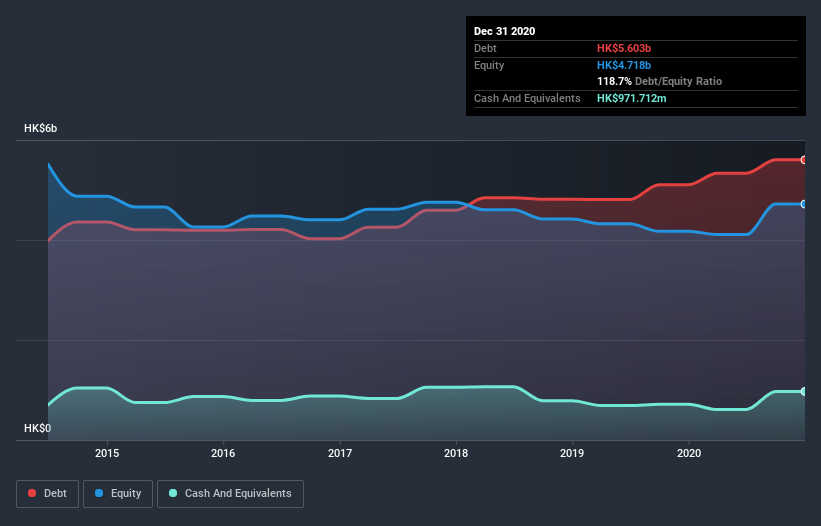

The image below, which you can click on for greater detail, shows that at December 2020 CK Life Sciences Int'l. (Holdings) had debt of HK$5.60b, up from HK$5.11b in one year. However, because it has a cash reserve of HK$971.7m, its net debt is less, at about HK$4.63b.

How Strong Is CK Life Sciences Int'l. (Holdings)'s Balance Sheet?

According to the last reported balance sheet, CK Life Sciences Int'l. (Holdings) had liabilities of HK$915.6m due within 12 months, and liabilities of HK$6.34b due beyond 12 months. Offsetting these obligations, it had cash of HK$971.7m as well as receivables valued at HK$949.9m due within 12 months. So it has liabilities totalling HK$5.34b more than its cash and near-term receivables, combined.

This is a mountain of leverage relative to its market capitalization of HK$7.78b. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Weak interest cover of 0.67 times and a disturbingly high net debt to EBITDA ratio of 21.2 hit our confidence in CK Life Sciences Int'l. (Holdings) like a one-two punch to the gut. This means we'd consider it to have a heavy debt load. Even worse, CK Life Sciences Int'l. (Holdings) saw its EBIT tank 70% over the last 12 months. If earnings continue to follow that trajectory, paying off that debt load will be harder than convincing us to run a marathon in the rain. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since CK Life Sciences Int'l. (Holdings) will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Over the last three years, CK Life Sciences Int'l. (Holdings) reported free cash flow worth 17% of its EBIT, which is really quite low. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

To be frank both CK Life Sciences Int'l. (Holdings)'s interest cover and its track record of (not) growing its EBIT make us rather uncomfortable with its debt levels. And furthermore, its conversion of EBIT to free cash flow also fails to instill confidence. After considering the datapoints discussed, we think CK Life Sciences Int'l. (Holdings) has too much debt. That sort of riskiness is ok for some, but it certainly doesn't float our boat. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. To that end, you should learn about the 4 warning signs we've spotted with CK Life Sciences Int'l. (Holdings) (including 2 which don't sit too well with us) .

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you decide to trade CK Life Sciences Int'l. (Holdings), use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:775

CK Life Sciences Int'l. (Holdings)

An investment holding company, researches, develops, manufactures, commercializes, and sells health and agriculture-related products in the Asia Pacific and North America.

Slightly overvalued with very low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor