Advertisement

Should Shareholders Reconsider Jacobson Pharma Corporation Limited's (HKG:2633) CEO Compensation Package?

Jacobson Pharma Corporation Limited (HKG:2633) has not performed well recently and CEO Derek Sum will probably need to up their game. At the upcoming AGM on 23 September 2022, shareholders can hear from the board including their plans for turning around performance. It would also be an opportunity for shareholders to influence management through voting on company resolutions such as executive remuneration, which could impact the firm significantly. We present the case why we think CEO compensation is out of sync with company performance.

View our latest analysis for Jacobson Pharma

How Does Total Compensation For Derek Sum Compare With Other Companies In The Industry?

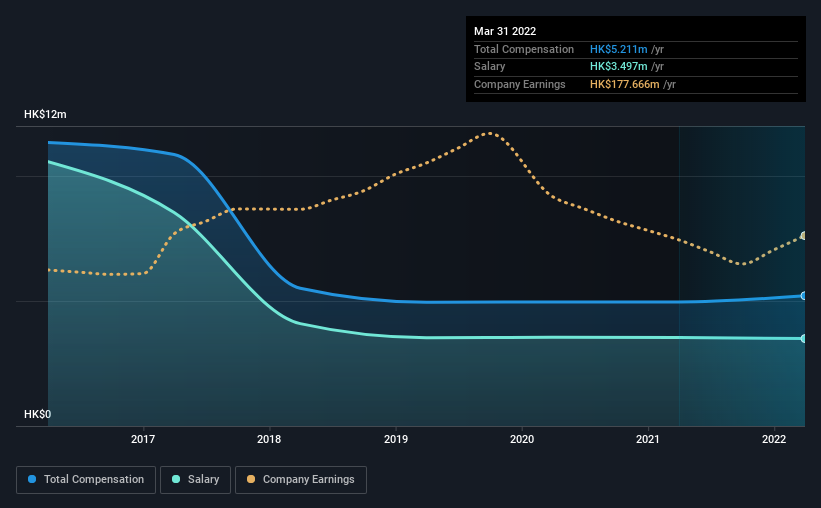

Our data indicates that Jacobson Pharma Corporation Limited has a market capitalization of HK$1.7b, and total annual CEO compensation was reported as HK$5.2m for the year to March 2022. That's a fairly small increase of 5.0% over the previous year. In particular, the salary of HK$3.50m, makes up a huge portion of the total compensation being paid to the CEO.

On examining similar-sized companies in the industry with market capitalizations between HK$785m and HK$3.1b, we discovered that the median CEO total compensation of that group was HK$1.3m. Hence, we can conclude that Derek Sum is remunerated higher than the industry median. Furthermore, Derek Sum directly owns HK$1.0b worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | HK$3.5m | HK$3.5m | 67% |

| Other | HK$1.7m | HK$1.4m | 33% |

| Total Compensation | HK$5.2m | HK$5.0m | 100% |

On an industry level, roughly 67% of total compensation represents salary and 33% is other remuneration. Jacobson Pharma is largely mirroring the industry average when it comes to the share a salary enjoys in overall compensation. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

Jacobson Pharma Corporation Limited's Growth

Jacobson Pharma Corporation Limited has reduced its earnings per share by 10.0% a year over the last three years. In the last year, its revenue is up 10%.

The decline in EPS is a bit concerning. And while it's good to see some good revenue growth recently, the growth isn't really fast enough for us to put aside my concerns around EPS. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Jacobson Pharma Corporation Limited Been A Good Investment?

Given the total shareholder loss of 12% over three years, many shareholders in Jacobson Pharma Corporation Limited are probably rather dissatisfied, to say the least. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

In Summary...

Along with the business performing poorly, shareholders have suffered with poor share price returns on their investments, suggesting that there's little to no chance of them being in favor of a CEO pay raise. At the upcoming AGM, management will get a chance to explain how they plan to get the business back on track and address the concerns from investors.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. We identified 2 warning signs for Jacobson Pharma (1 shouldn't be ignored!) that you should be aware of before investing here.

Switching gears from Jacobson Pharma, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2633

Jacobson Pharma

Through its subsidiaries, engages in the research, development, production, sale, and distribution of medicine and drugs in Hong Kong, Mainland China, Macau, Singapore, and internationally.

Flawless balance sheet, undervalued and pays a dividend.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor