Advertisement

Market Participants Recognise Qyuns Therapeutics Co., Ltd.'s (HKG:2509) Revenues Pushing Shares 26% Higher

The Qyuns Therapeutics Co., Ltd. (HKG:2509) share price has done very well over the last month, posting an excellent gain of 26%. Still, the 30-day jump doesn't change the fact that longer term shareholders have seen their stock decimated by the 56% share price drop in the last twelve months.

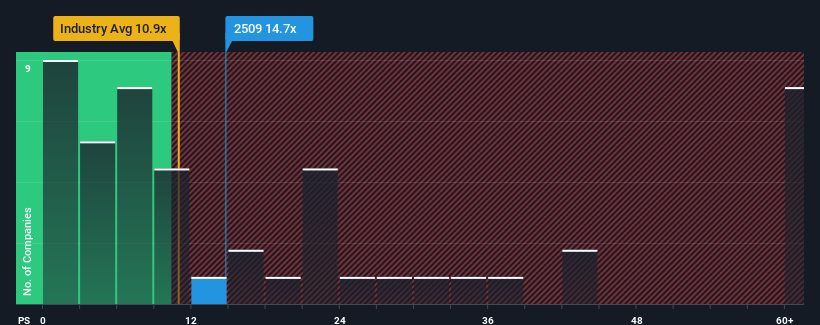

After such a large jump in price, Qyuns Therapeutics may be sending bearish signals at the moment with its price-to-sales (or "P/S") ratio of 14.7x, since almost half of all companies in the Biotechs in Hong Kong have P/S ratios under 10.9x and even P/S lower than 5x are not unusual. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

See our latest analysis for Qyuns Therapeutics

How Qyuns Therapeutics Has Been Performing

With revenue growth that's exceedingly strong of late, Qyuns Therapeutics has been doing very well. Perhaps the market is expecting future revenue performance to outperform the wider market, which has seemingly got people interested in the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Although there are no analyst estimates available for Qyuns Therapeutics, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Is There Enough Revenue Growth Forecasted For Qyuns Therapeutics?

In order to justify its P/S ratio, Qyuns Therapeutics would need to produce impressive growth in excess of the industry.

Retrospectively, the last year delivered an explosive gain to the company's top line. Spectacularly, three year revenue growth has also set the world alight, thanks to the last 12 months of incredible growth. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

This is in contrast to the rest of the industry, which is expected to grow by 27% over the next year, materially lower than the company's recent medium-term annualised growth rates.

In light of this, it's understandable that Qyuns Therapeutics' P/S sits above the majority of other companies. Presumably shareholders aren't keen to offload something they believe will continue to outmanoeuvre the wider industry.

The Bottom Line On Qyuns Therapeutics' P/S

Qyuns Therapeutics shares have taken a big step in a northerly direction, but its P/S is elevated as a result. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Qyuns Therapeutics maintains its high P/S on the strength of its recent three-year growth being higher than the wider industry forecast, as expected. In the eyes of shareholders, the probability of a continued growth trajectory is great enough to prevent the P/S from pulling back. If recent medium-term revenue trends continue, it's hard to see the share price falling strongly in the near future under these circumstances.

And what about other risks? Every company has them, and we've spotted 1 warning sign for Qyuns Therapeutics you should know about.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Qyuns Therapeutics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2509

Qyuns Therapeutics

A clinical-stage biotech company, focuses on the research and development of biologic therapies for autoimmune and allergic diseases in the People’s Republic of China.

Excellent balance sheet minimal.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor