Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Wuhan YZY Biopharma Co., Ltd. (HKG:2496) makes use of debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

What Is Wuhan YZY Biopharma's Net Debt?

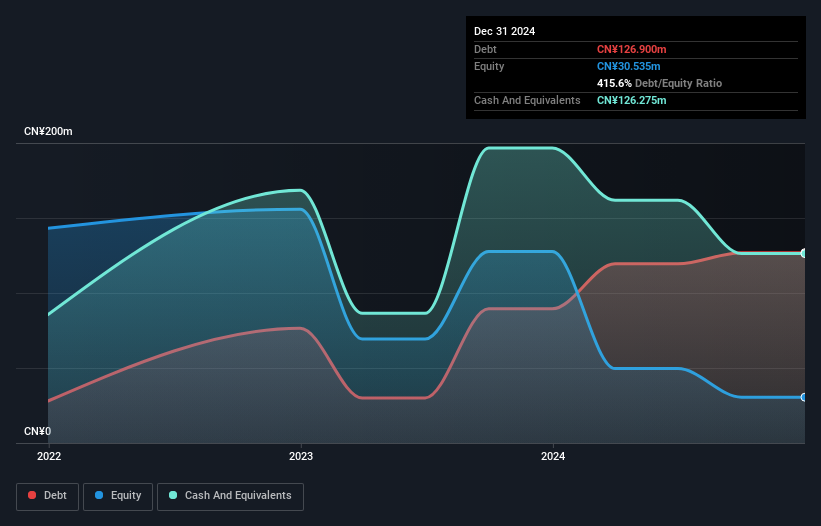

As you can see below, at the end of December 2024, Wuhan YZY Biopharma had CN¥126.9m of debt, up from CN¥89.5m a year ago. Click the image for more detail. However, it also had CN¥126.3m in cash, and so its net debt is CN¥625.0k.

How Healthy Is Wuhan YZY Biopharma's Balance Sheet?

The latest balance sheet data shows that Wuhan YZY Biopharma had liabilities of CN¥186.1m due within a year, and liabilities of CN¥51.2m falling due after that. Offsetting this, it had CN¥126.3m in cash and CN¥82.0k in receivables that were due within 12 months. So its liabilities total CN¥111.0m more than the combination of its cash and short-term receivables.

Given Wuhan YZY Biopharma has a market capitalization of CN¥1.11b, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Carrying virtually no net debt, Wuhan YZY Biopharma has a very light debt load indeed. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Wuhan YZY Biopharma will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Check out our latest analysis for Wuhan YZY Biopharma

While it hasn't made a profit, at least Wuhan YZY Biopharma booked its first revenue as a publicly listed company, in the last twelve months.

Caveat Emptor

Even though Wuhan YZY Biopharma managed to grow its top line quite deftly, the cold hard truth is that it is losing money on the EBIT line. Indeed, it lost CN¥95m at the EBIT level. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. We would feel better if it turned its trailing twelve month loss of CN¥98m into a profit. So to be blunt we do think it is risky. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 1 warning sign for Wuhan YZY Biopharma you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Wuhan YZY Biopharma might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2496

Wuhan YZY Biopharma

A biotechnology company, develops bispecific antibody-based therapies for the treatment of cancer, cancer-related complications, and age-related ophthalmologic diseases.

Slightly overvalued with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|41.9% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|14.1% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$613.59|1.3% undervalued

AN

Based on Analyst Price Targets