Advertisement

Chow Sang Sang Holdings International And 2 Other Undiscovered Gems In Asia With Strong Potential

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a landscape of steady U.S. inflation and economic uncertainties, small-cap stocks have shown resilience, with the Russell 2000 Index outperforming larger counterparts. In this context, identifying promising opportunities in Asia's dynamic market can be rewarding, especially when focusing on companies with solid fundamentals and growth potential like Chow Sang Sang Holdings International and two other noteworthy contenders.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Nantong Guosheng Intelligence Technology Group | NA | 8.02% | 1.71% | ★★★★★★ |

| Suzhou Fushilai Pharmaceutical | NA | -12.24% | -31.94% | ★★★★★★ |

| Qingmu Tec | 0.74% | 13.00% | -19.41% | ★★★★★★ |

| Yibin City Commercial Bank | 82.57% | -1.19% | 15.94% | ★★★★★★ |

| DYPNFLtd | 26.11% | 13.24% | 0.06% | ★★★★★☆ |

| Daewon Cable | 23.95% | 7.90% | 48.33% | ★★★★★☆ |

| FCE | 7.36% | 11.78% | 26.35% | ★★★★★☆ |

| BIOBIJOULtd | 0.07% | 45.63% | 49.17% | ★★★★★☆ |

| Jinlihua Electric | 48.71% | 7.36% | 31.30% | ★★★★★☆ |

| Palasino Holdings | 9.75% | 10.88% | -14.54% | ★★★★★☆ |

We're going to check out a few of the best picks from our screener tool.

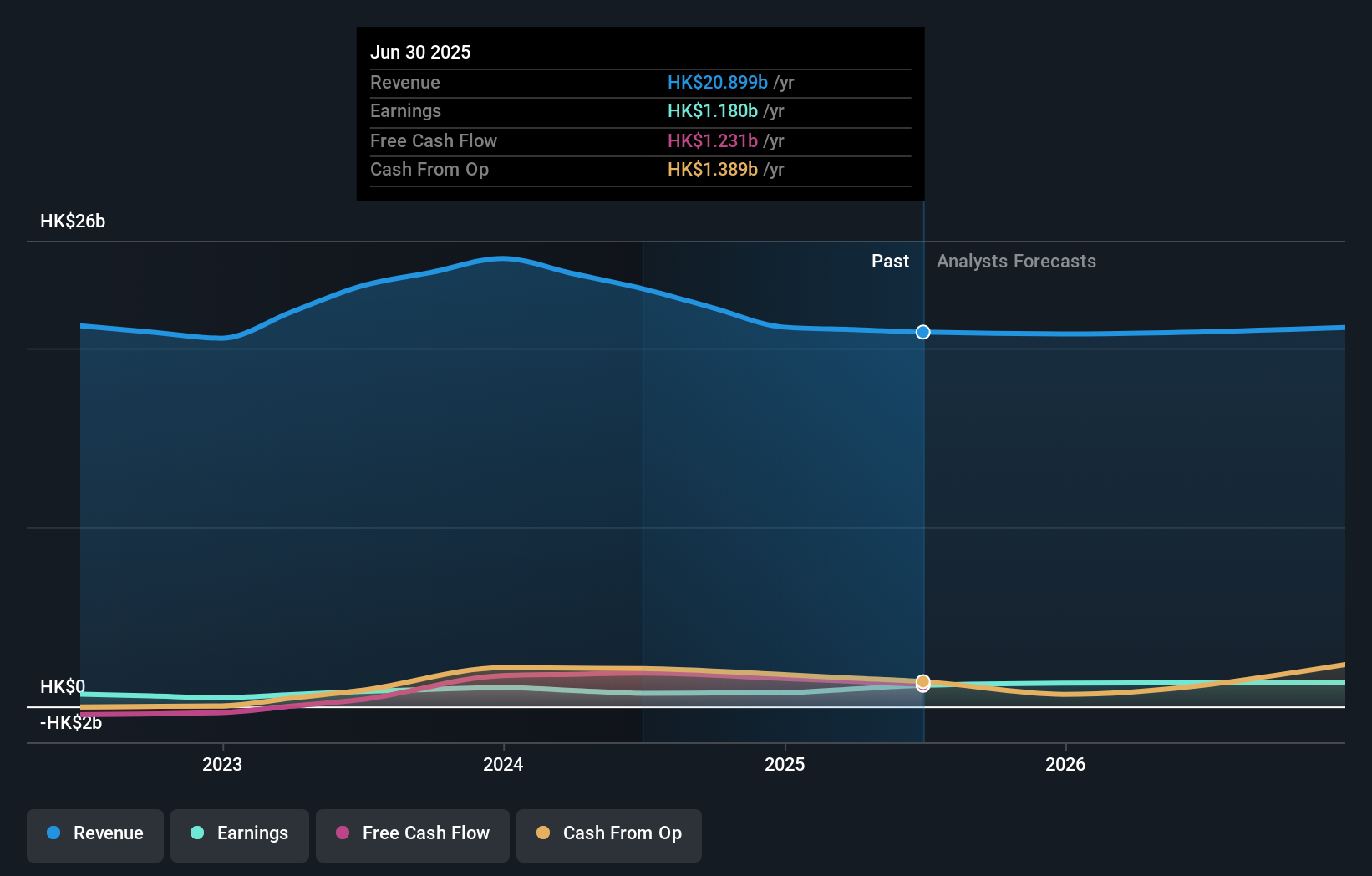

Chow Sang Sang Holdings International (SEHK:116)

Simply Wall St Value Rating: ★★★★★☆

Overview: Chow Sang Sang Holdings International Limited is an investment holding company that manufactures and retails jewellery across Mainland China, Hong Kong, Macau, and Taiwan with a market capitalization of approximately HK$9 billion.

Operations: The primary revenue stream for Chow Sang Sang Holdings International comes from the retail of jewellery and watches, generating HK$20.41 billion, followed by wholesale of precious metals at HK$466.89 million. Trading of LGD and other businesses contribute minimally to the overall revenue.

Chow Sang Sang Holdings International, a smaller player in the luxury sector, has shown impressive earnings growth of 61% over the past year, surpassing the industry's 5.8%. The company reported a net income of HK$901.74 million for the first half of 2025, up from HK$525.99 million a year prior. Despite an increase in its debt to equity ratio from 20.1% to 39% over five years, it remains satisfactory at 29.2%. With high-quality earnings and trading at nearly half its estimated fair value, Chow Sang Sang appears well-positioned despite forecasts suggesting potential future challenges with declining earnings expectations.

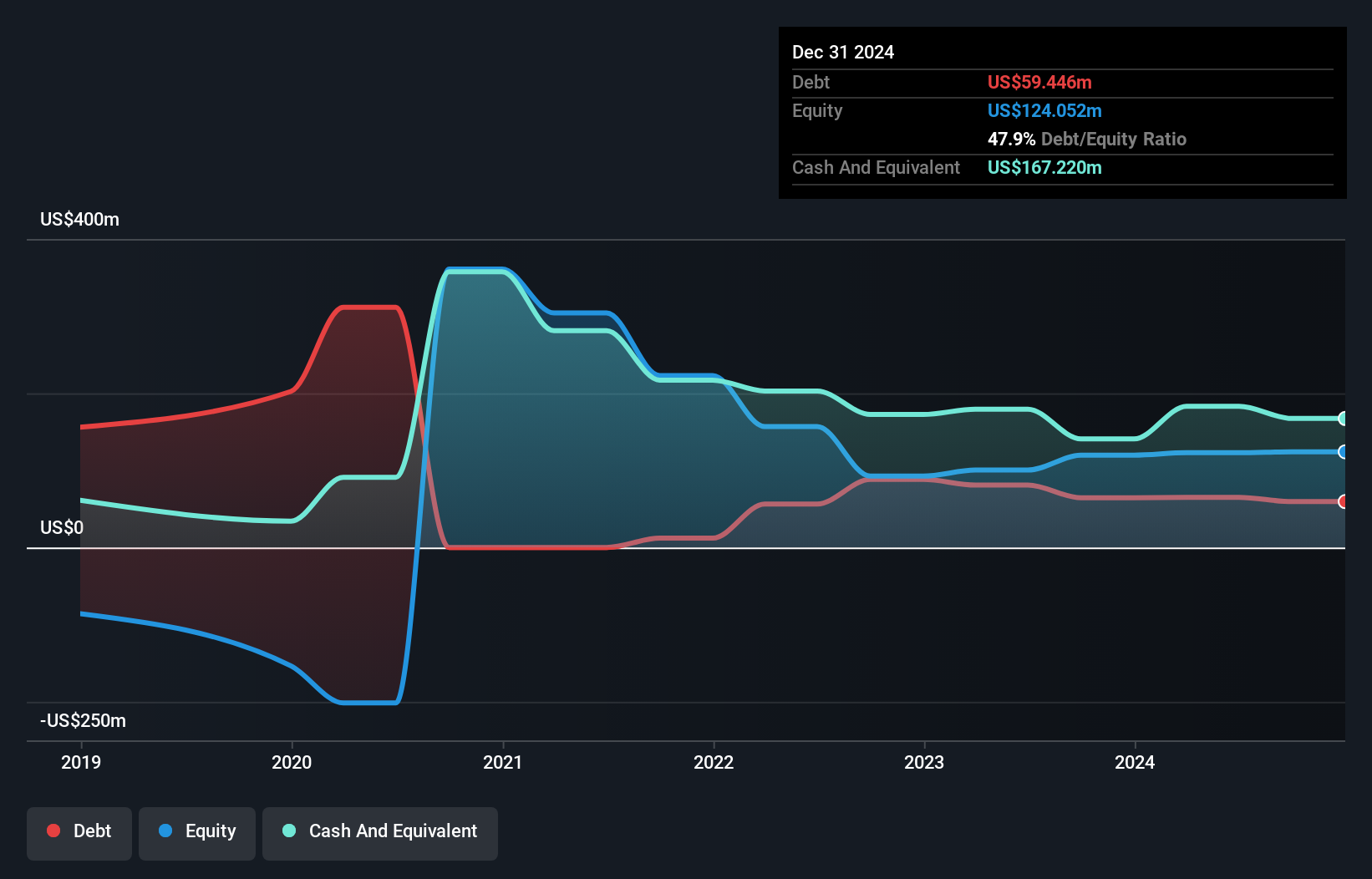

HBM Holdings (SEHK:2142)

Simply Wall St Value Rating: ★★★★★★

Overview: HBM Holdings Limited is a biopharmaceutical company that focuses on the discovery, development, and commercialization of antibody therapeutics in immunology and oncology across Mainland China, the United States, Europe, and internationally with a market cap of approximately HK$11.68 billion.

Operations: HBM Holdings generates revenue primarily from its biotechnology segment, amounting to $115.71 million. The company's market capitalization is approximately HK$11.68 billion.

HBM Holdings, a nimble player in the biopharma sector, has shown impressive financial growth with earnings surging by 243% over the past year, outpacing the industry average of 16.8%. The company is financially sound, boasting more cash than total debt and positive free cash flow. Recent developments include a substantial follow-on equity offering of HKD 517.75 million and strategic collaborations like their partnership with Otsuka Pharmaceutical for BCMAxCD3 bispecific T-cell engagers. Despite a volatile share price recently, HBM's Price-To-Earnings ratio of 20.5x remains below the industry average of 48.2x, indicating potential value for investors.

- Click here and access our complete health analysis report to understand the dynamics of HBM Holdings.

Explore historical data to track HBM Holdings' performance over time in our Past section.

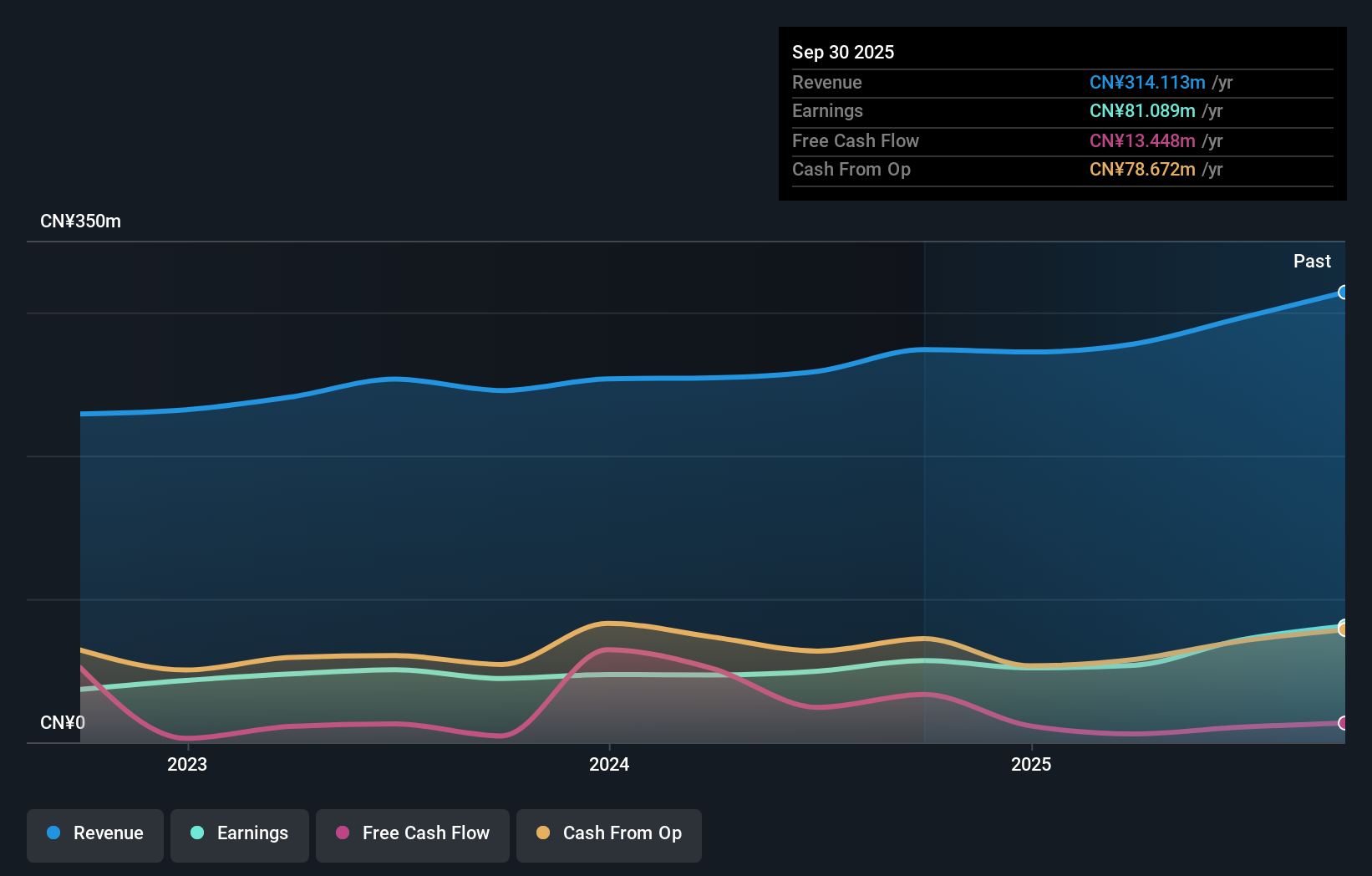

Touchstone International Medical Science (SHSE:688013)

Simply Wall St Value Rating: ★★★★★☆

Overview: Touchstone International Medical Science Co., Ltd. specializes in the development and production of surgical and medical equipment, with a market cap of CN¥4.47 billion.

Operations: Touchstone International generates revenue primarily from its surgical and medical equipment segment, totaling CN¥278 million.

Touchstone International Medical Science, a promising contender in the medical equipment sector, has shown robust earnings growth of 14% over the past year, outpacing the industry average of -2.6%. The company boasts a strong financial position with more cash than total debt and positive free cash flow. Its debt to equity ratio has risen slightly to 3.5% over five years, indicating manageable leverage. High levels of non-cash earnings highlight quality performance. With profitability ensuring a stable cash runway and interest coverage not being an issue, Touchstone seems well-positioned for continued success in its field.

Key Takeaways

- Unlock our comprehensive list of 2387 Asian Undiscovered Gems With Strong Fundamentals by clicking here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:116

Chow Sang Sang Holdings International

An investment holding company, manufactures and retails jewellery in the Mainland China, Hong Kong, Macau, and Taiwan.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor